Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 30 June 2026 06:44 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

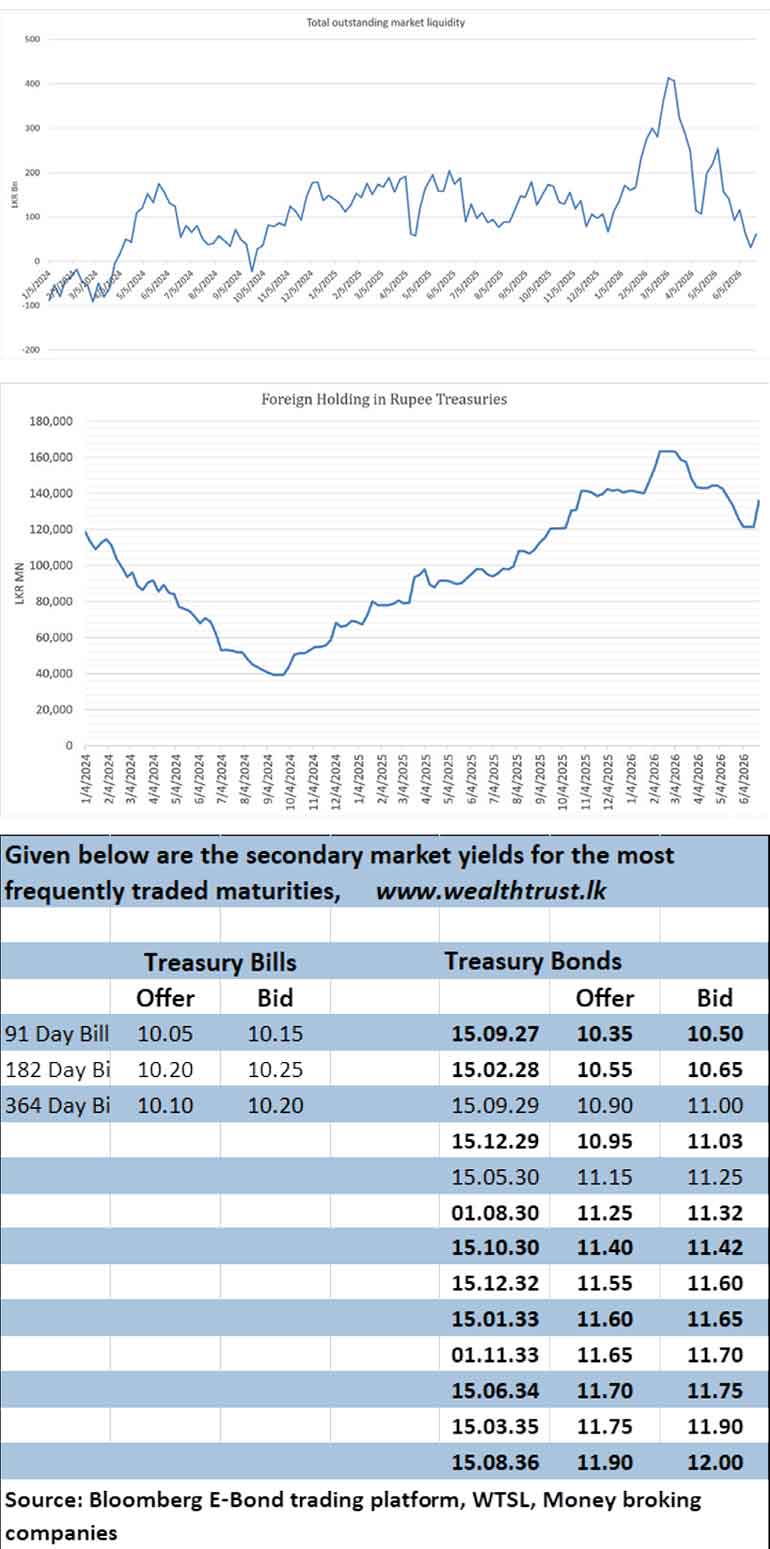

The foreign demand for rupee-denominated Government securities gathered significant momentum, with holdings rising for a third consecutive week.

The week ending 25 June recorded a substantial net inflow of Rs. 14.51 billion, the largest weekly foreign inflow in over three years, since 8 June 2023, driving total foreign holdings up to Rs. 135.86 billion.

The outcome at last Fridays Treasury Bond auction saw the yield curve flattening from the 4-year duration to the 10-year duration as the term premiums were seen narrowing.

The entire offered amount of Rs. 60 billion was raised at the first phase of the auction while the direct issuance window will be opened for an additional 10% of the offered amount on each duration at its weighted averages until 3.00pm today (30 June).

The bids received to accepted amount ratio stood at a staggering 3.17 times.

Maturity-wise the results were as follows:

The shorter tenor 15.10.30 maturity was issued at a weighted average yield of 11.44%, marginally above its pre-auction secondary market rate of 11.35%-11.40%.

The 15.03.35 maturity was issued at the weighted average yield of 11.88%, below its pre-auction secondary market rate of 11.85%-12.00% (see table for details of the auction).

The secondary Bond market remained largely range-bound during the week, with yields consolidating despite some volatility.

Strong buying interest, particularly in the 2030 maturities, briefly pushed yields lower midweek before profit taking prompted a partial reversal. Activity moderated ahead of the Treasury Bond auction as investors adopted a wait-and-see approach. Overall, market activity remained healthy while yields ended the week slightly higher on the short end, while the rest of the yield curve was broadly unchanged.

In the secondary Bond market, the 15.03.28 maturity changed hands within the range of 10.60%–10.6225%, while the 01.05.28 maturity traded within the range of 10.64% to 10.60%. The 15.10.28 maturity traded within the range of 10.6550% to 10.6350%.

Moving into the 2029 segment, the 15.06.29 maturity changed hands at the rate of 10.92%, while the 15.12.29 maturity touched a weekly low of 10.90%, before trading back up at 11.00%.

In the 2030 space, the 01.03.30 maturity changed hands at the rate of 11.05%. The 01.08.30 maturity touched an intraweek low of 11.14%, before trading back up to 11.30%. Similarly, the 15.10.30 maturity traded down to a low of 11.15% prior to the auction, before trading up to 11.40%.

Further along the curve, the 15.01.33 maturity changed hands within the range of 11.60%–11.55%. The 01.11.33 maturity traded within the range of 11.65% to 11.60%. The 15.06.34 maturity traded within the range of 11.70% to 11.65%.

At the longer end, the 15.03.35 maturity traded at the rates of 11.85%-11.80%, while the 15.06.35 maturity changed hands within the range of 11.95%–11.90%. The 15.08.36 maturity traded within the narrow range of 12.01% to 11.98%.

At the weekly Treasury Bill auction held last Wednesday, yields increased across all maturities, albeit by different extents, reversing part of the decline recorded at the previous auction.

The sharpest increase was witnessed on the 91-day bill by 12 basis points to 10.14% followed by the 182-day bill by 5 basis points to 10.21%. However, the 364-day bill edged up marginally by only 1 basis point to 10.17%

The auction successfully raised the full Rs. 70 billion offered at the first phase of competitive bidding, with accepted volumes across all maturities matching the amounts offered. Total bids received amounted to 1.86 times the offered volume.

In the money market, the total outstanding liquidity surplus was recorded at Rs. 61.62 billion improving notably against its previous week’s Rs. 31.25 billion. The weighted average interest rates on Call Money and Repo stood at 9.22% and 9.24% respectively at the close of the week unchanged against the previous week.

Forex market

In the forex market, the USD/LKR rate on spot contracts was seen closing the week lower at Rs. 336.40/336.70 as against its previous week’s closing of Rs. 333.85/334.25. This was subsequent to trading from at an intraweek high of Rs. 334.25 and a low of Rs.337.75.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 74.31 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)