Wednesday Aug 05, 2026

Wednesday Aug 05, 2026

Wednesday, 11 March 2026 01:11 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

A sharp correction in global oil prices triggered a relief rally in Sri Lanka’s Secondary Government Bond market yesterday. Brent crude, which had surged to nearly $ 120 per barrel amid fears of supply disruptions in the Middle East, fell below $ 95 after signals emerged that geopolitical tensions may ease. This was spurred by news that the US President indicated that the conflict with Iran could be nearing its end. He also noted plans to waive oil-related sanctions and deploy the US Navy to escort tankers through the Strait of Hormuz, aiming to stabilise oil flows and prevent further price spikes.

The decline in oil prices eased fears of prolonged energy inflation and external sector pressures for oil-importing economies such as Sri Lanka. As a result, risk premiums embedded in Government securities began to compress, attracting renewed buying interest from banks and institutional investors. The rally was observed across the yield curve. Activity and transaction volumes were initially very strong during the rally but eventually tapered off as market participants settled back into a wait and see mode as the day progressed.

This rally was compounded by the robust and stable macroeconomic situation domestically. It was reported that Sri Lanka’s gross official reserves rose to $ 7.28 billion in February, marking a six-year high, while external sector data released by the Central Bank of Sri Lanka showed the current account recording a surplus of $ 369.7 million in January 2026, significantly higher than both recent months and January 2025 ($ 99.8 million). This follows a provisional surplus of $ 1.7 billion for 2025, highlighting improving external sector dynamics.

Meanwhile, liquidity conditions in the domestic banking system remain ample, keeping money market rates compressed and supportive of demand for government securities. Against this backdrop, easing global geopolitical risks and stable domestic macro conditions saw yields normalise lower across the secondary bond market.

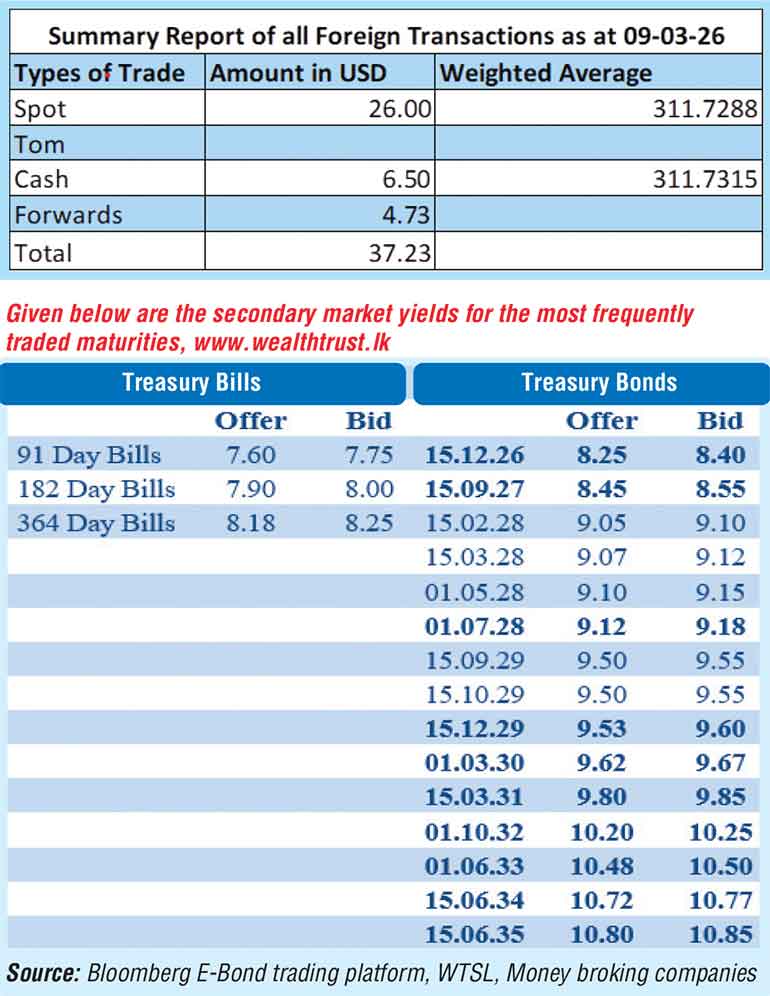

Accordingly, the 01.08.26 maturity traded at the rate of 8.30%. The 15.02.28 maturity traded lower at the rate of 9.10%. The 15.09.29 maturity traded at the rate of 9.55%. The 01.10.32 maturity traded within the range of 10.25% to 10.23%. The 01.06.33 maturity experienced a steep drop in rates of 10 basis points intraday from a high of 10.60% to a low of 10.50%. The 15.06.34 maturity traded within the range of 10.75%-10.72% and the 15.06.35 maturity saw its rate drop from an intraday high of 10.85% to a low of 10.80%.

These developments come ahead of the weekly Treasury Bill auction scheduled for today which will have on offer a total amount of Rs. 130 billion. The auction will be comprising of Rs. 40 billion in 91-day bills, Rs. 60 billion in 182-day bills, and Rs. 30 billion in 364-day bills. The offered amount is below the maturing volume, which is estimated at around Rs. 149.39 billion.

For context, the weekly Treasury bill auction conducted last Wednesday (4) saw yields hold broadly steady, breaking a six-week consecutive streak of decreases prior. Accordingly, the rate on the 91-day bill remained at 7.63% and the rate on the 182-day bill stayed static at 7.92%. However, the 364-day bill saw its yield ease very marginally by 1 basis points to 8.23%. The auction was heavily undersubscribed at the 1st phase in competitive bidding. The auction raised only

Rs. 47.83 billion, or 39.86% of the total offered amount of Rs. 120.00 billion. An additional amount of Rs. 7.50 billion was raised from the second phase. Accordingly, the aggregate accepted amount of the issuance was Rs. 55.33 billion.

The total secondary market Treasury bond/bill transacted volume for 9 March was Rs. 13.57 billion.

In money markets, the net liquidity surplus was recorded at Rs. 335.36 billion yesterday. The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka was seen draining out an amount of Rs. 150.00 billion by way of overnight repo auction at a weighted average rate of 7.46% while an amount of Rs 185.36 billion was deposited at Central Banks SDFR (Standing Deposit Facility Rate) of 7.25%. No funds were withdrawn from the Central Banks SLFR (Standing Lending Facility Rate) of 8.25%.

The weighted average rates on overnight call money and Repo stood at 7.63% and 7.65% respectively.

Forex market

The USD/LKR rate on spot contracts was seen appreciating, to close the day at

Rs. 310.90/311.00 as against the previous day’s closing level of Rs. 311.60/311.90. The total USD/LKR traded volume for 9 March was $ 37.23 million.

(References: Central Bank of Sri Lanka, Bloomberg E-Bond trading platform, Money broking companies)