Saturday Jun 06, 2026

Saturday Jun 06, 2026

Thursday, 26 February 2026 00:00 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The net liquidity surplus in money market was recorded at Rs. 322.93 billion yesterday crossing the Rs. 300 billion mark and hitting the highest level in 22 years, up from Rs. 297.94 billion the day before.

The Domestic Operations Department (DOD) of the Central Bank of Sri Lanka was seen draining out an amount of Rs. 75 billion by way of overnight Repo auction at a weighted average rate of 7.64% and an amount of Rs. 25 billion by way of seven-day Repo auction at a weighted average rate of 7.74%.

Further an amount of Rs. 223.33 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25% as against an amount of Rs. 0.40 billion withdrawn from the Central Bank’s SDFR (Standing Deposit Facility Rate) of 8.25%. The weighted average rates on overnight call money and Repo yesterday stood at 7.69% and 7.71% respectively.

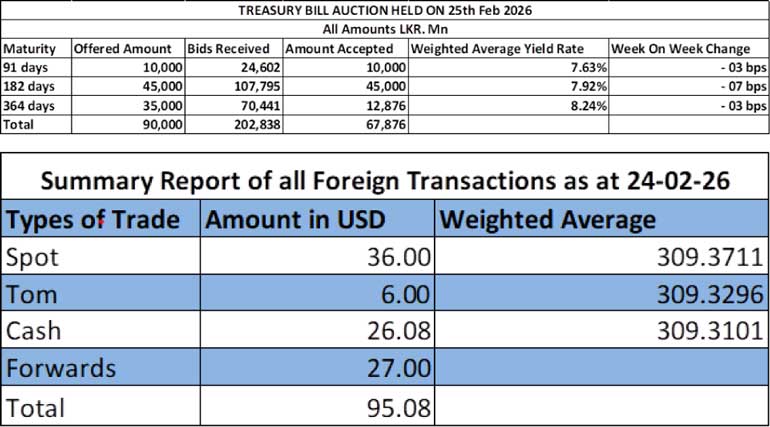

Meanwhile, the weekly Treasury Bill auction conducted yesterday saw yields continue their downward trajectory, with weighted average rates declining across all maturities for the sixth consecutive week.

Accordingly, the rate on the 91-day Bill declined by three basis points to 7.63%, the rate on the 182-day Bill dropping by seven basis points to 7.92% and the 364-day Bill saw its yield ease more by three basis points to 8.24%.

However, the auction was undersubscribed, raising only Rs. 67.88 billion, or 75.42% of the total offered amount of Rs. 90 billion. The bid-to-cover ratio stood at 2.25 times.

The Phase II subscription across all three maturities is now open until 3.00 pm of business day prior to settlement date (i.e., 26.02.2026) at the WAYRs determined for the said ISINs at the auction.

The secondary Bond market saw a constructive tone as yields recovered slightly and consolidated yesterday. This was supported by renewed buying interest following the recent uptick in yields. However, market activity was largely at a standstill for most of the day, with only intermittent and sporadic trading.

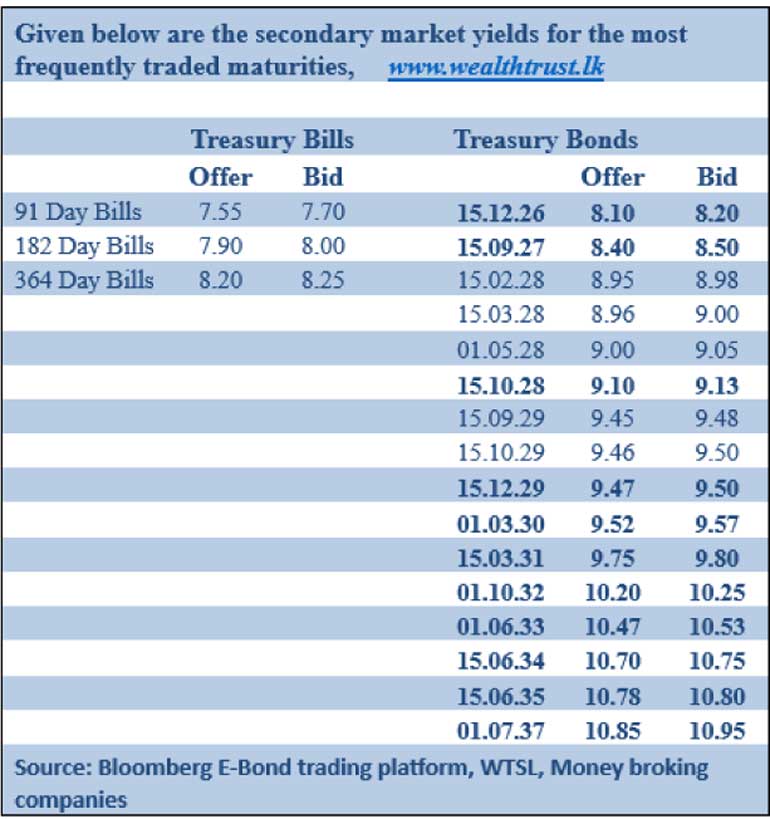

In terms of the Secondary Bond market trade summary, the 01.08.26 maturity traded at the rate of 8.00%-8.10% and the 15.01.27 maturity traded at the rate of 8.23% to 8.25%. The 15.02.28 and 01.05.28 maturity traded at the rate of 8.98% and 9.05% respectively. The 15.10.28 maturity traded at the rate of 10.12%. The 15.09.29, 15.10.29 and 15.12.29 maturities were seen trading at the rates of 9.45%, 9.47% and 9.48% respectively. The 01.03.30 maturity traded at the rate of 9.55%. The 15.06.34 and 15.06.35 maturities traded at the rates of 10.72% and 10.80% respectively.

This comes ahead of the Treasury Bond auction scheduled to be conducted today (26) as follows. The round of auction will have a total offered amount of Rs. 140 billion across three available maturities.

The auction will be comprised of: Rs. 40 billion from a 1 March 2030 maturity bearing a coupon rate of 9.50%; Rs. 60 billion from a 15 June 2034 maturity bearing a coupon rate of 10.75%; Rs. 40 billion from a 1 July 2037 maturity bearing a coupon rate of 10.75%. The settlement for which will be held on 3 March 2026.

For reference the immediately previous Treasury Bond auction held last on 12 February, delivered a bullish outcome. The Public Debt Management Office successfully raised the entire Rs. 51 b on offer across two available maturities. Weighted average yields were in line with or below prevailing market levels, while demand was robust, reflected by a bid-to-acceptance ratio of 4.86 times.

Maturity wise: The 01.03.30 maturity was fully taken up at the first phase at a weighted average yield (WAYR) of 9.52%, in line with pre-auction levels; the 15.08.36 maturity was also fully subscribed at the first phase at a WAYR of 10.73%, coming in well below comparable market benchmarks pre-auction.

The total secondary market Treasury Bond/Bill transacted volume for 24 February was Rs. 10.90 billion.

Forex market

In the Forex market, the USD/LKR rate on spot contracts closed the day at 309.33/309.36, as against its previous day’s closing level of Rs. 309.35/309.40.

The total USD/LKR traded volume for 24 February was Rs. 95.08 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)