Tuesday Jun 09, 2026

Tuesday Jun 09, 2026

Monday, 8 June 2026 04:57 - - {{hitsCtrl.values.hits}}

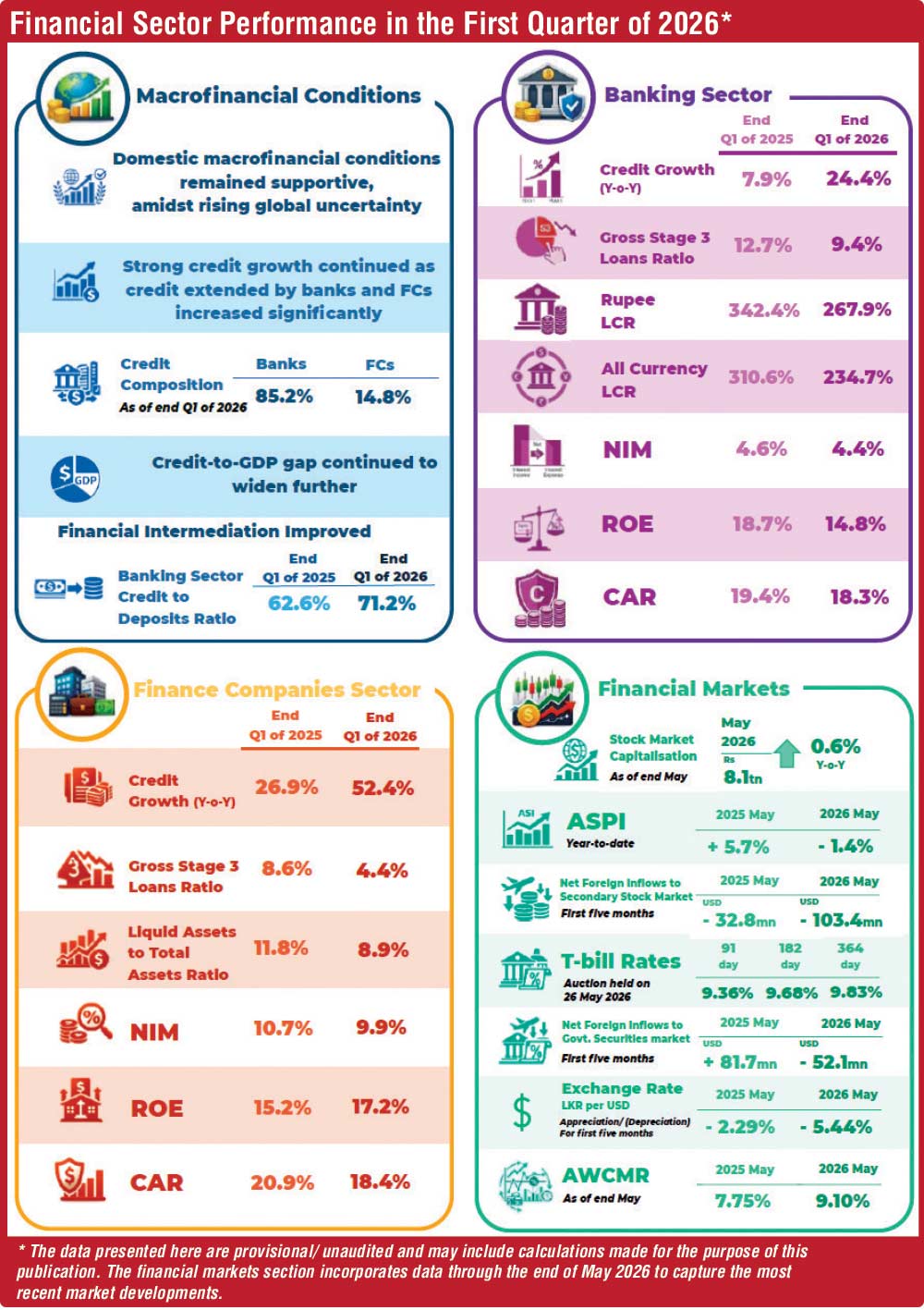

The financial system remained resilient during the first quarter of 2026 despite heightened geopolitical tensions, external sector pressures and growing global uncertainty, according to the Central Bank of Sri Lanka’s (CBSL) latest Financial Sector Performance Report.

The Central Bank said domestic macrofinancial conditions remained broadly supportive during the quarter, supported by strong private sector credit growth and improving financial intermediation, although emerging risks linked to inflation, exchange rate volatility, commodity prices and adverse weather conditions continued to warrant close monitoring.

Macrofinancial conditions

The CBSL noted that total credit extended by licensed banks and finance companies expanded further during the quarter, driven mainly by private sector lending, while exposures to the Government and public corporations moderated marginally.

Financial intermediation improved with the banking sector’s credit-to-deposit ratio exceeding 70% for the first time in three years, reflecting the continued recovery in lending activity.

However, the Central Bank cautioned that the credit-to-GDP gap widened further into positive territory, indicating the potential build-up of systemic risks within the financial sector.

The report said sustained fiscal consolidation, stronger external buffers and vigilant monitoring of emerging macrofinancial risks would remain critical to preserving financial stability amid rising energy prices, commodity market volatility, exchange rate fluctuations and inflationary pressures.

Banking sector performance

Credit granted by the banking sector grew by 24.4% year-on-year (YoY)

at end-March 2026, sharply higher than the 7.9% growth recorded a year earlier.

Asset quality continued to improve, with the Stage 3 loans ratio declining to 9.4% from 12.7%, supported by both credit expansion and a slight reduction in impaired loans. The impairment coverage ratio for Stage 3 loans improved to 59.5% from 54.1%.

The acceleration in lending was reflected in a moderation of liquidity buffers. The rupee liquidity coverage ratio declined to 267.9% from 342.4%, while the all-currency liquidity coverage ratio fell to 234.7% from 310.6%. Nevertheless, both remained well above the minimum regulatory requirement of 100%.

Profitability weakened modestly during the quarter, with profit after tax (PAT)

declining by 7.1% YoY due mainly to higher operating expenses. Return on (ROE)

fell to 14.8% from 18.7%, while return on assets declined to 2.2% from 2.6%.

The banking sector’s total capital adequacy (CAR) moderated to 18.3% from 19.4% a year earlier as risk-weighted assets increased alongside stronger lending growth.

The CBSL also warned that the recent depreciation of the rupee and higher secondary market yields could exert further pressure on capital buffers through asset revaluation effects. In addition, cyber-related incidents and financial scams remain emerging risks requiring greater vigilance.

Finance companies sector performance

The finance companies sector maintained strong growth momentum during the quarter, with total credit expanding by 52.4% YoY compared to 26.9% growth recorded a year earlier.

The expansion was largely driven by vehicle financing and gold-backed lending. Vehicle-backed lending increased by 52.8%, while gold-backed lending recorded a robust 69.2% increase.

Asset quality improved significantly, with the Stage 3 loans ratio declining to 4.4% from 8.6%. However, the impairment coverage ratio eased slightly to 45.1% from 47.4%.

Liquidity remained comfortable, with total liquid assets increasing

by 9.7% YoY and remaining well above regulatory requirements.

Profitability strengthened considerably, with PAT rising by 28.8% during the 2025/26 financial year. ROE increased to 17.2% from 15.2%, although return on (ROA) moderated slightly to 6.2% from 6.6%.

The sector’s total CAR declined to 18.4% from 20.9% due to rapid credit expansion.

The Central Bank noted that future lending growth may moderate due to higher vehicle prices arising from increased import duties and exchange rate depreciation, as well as tighter monetary and macroprudential policies.

Financial market performance

Domestic financial markets experienced increased pressure during the first five months of 2026 amid escalating tensions in the Middle East, growing external sector vulnerabilities and speculative market activity.

The Colombo Stock Exchange recorded mixed performance. The All Share Price Index declined by 1.4%, while the S&P SL20 Index remained broadly unchanged, posting a marginal gain of 0.03% as at end-May.

Foreign investors continued to exit the market, with net foreign outflows amounting to $ 103.4 million during the period, adding to cumulative divestments recorded over the previous two years.

The Government securities market also came under pressure, with yields trending upwards from March and rising further following the 100-basis-point policy rate increase announced by the CBSL in late May.

Secondary market activity moderated somewhat, while foreign participation remained volatile due to evolving global uncertainties.

The domestic foreign exchange market experienced continued volatility amid external sector pressures, while surplus liquidity persisted in the money market, requiring the Central Bank to absorb excess funds through open market operations.

Recent macroprudential measures

In response to rapid growth in collateral-based lending and heightened asset price volatility, the CBSL introduced several macroprudential measures to strengthen financial stability.

With effect from 25 May 2026, a maximum loan-to-value (LTV) ratio of 70% was imposed on credit facilities secured by gold.

The Central Bank also tightened existing maximum LTV ratios applicable to vehicle financing facilities by 10 percentage points.

According to the CBSL, the measures were introduced in response to significant expansion in collateral-backed lending, exchange rate volatility and geopolitical uncertainties that could amplify financial system risks.

The report concluded that while Sri Lanka’s financial sector remained resilient during the first quarter, continued vigilance would be necessary as external shocks, inflationary pressures, commodity price volatility and exchange rate movements continue to pose challenges to macrofinancial stability.