Thursday Jul 09, 2026

Thursday Jul 09, 2026

Wednesday, 8 July 2026 00:06 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

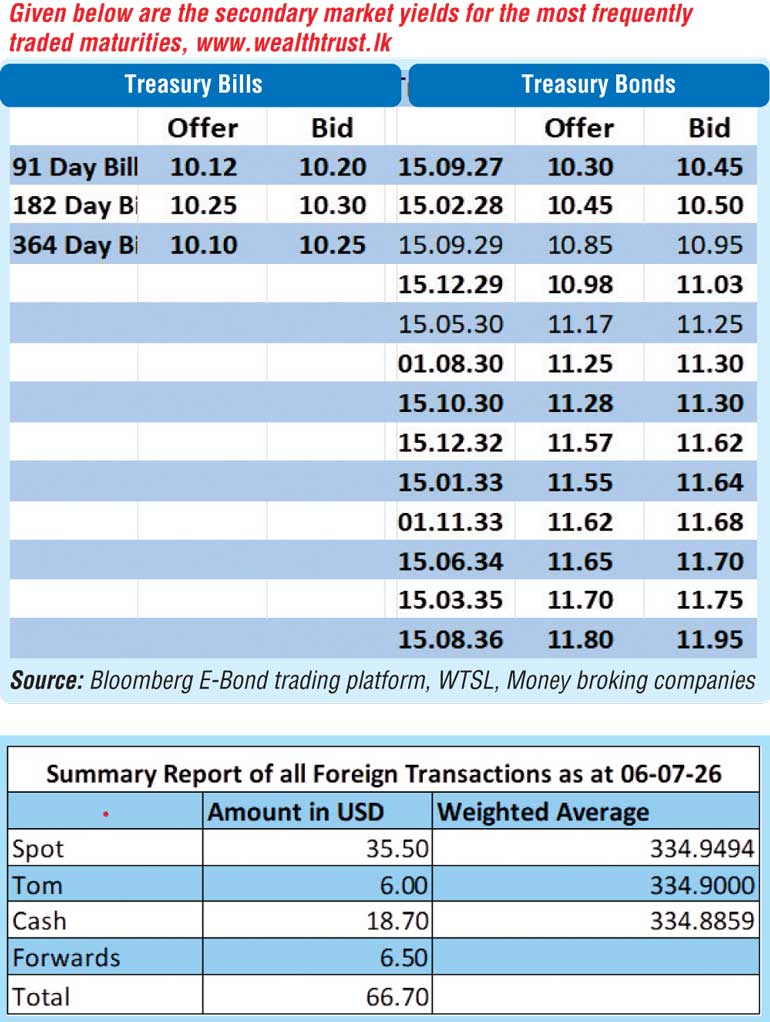

The secondary Bond market yesterday saw activity pick up against its previous day’s dormant mood, with activity concentrated mainly on the short end of the yield curve.

At the very short end of the curve, the 15.02.28, 15.03.28, 01.05.28 and 01.07.28 maturities traded at the rates of 10.50%, 10.55%, 10.60% and 10.65% respectively.

The 15.12.29 maturity traded at the rate of 11%. On the 4-year 2030 segment, the 01.03.30 maturity traded at the rate of 11.10%, the 01.07.30 at the rate of 11.25%, the 01.08.30 at the rates of 11.25%-11.28% and the 15.10.30 at the rates of 11.30%-11.33%.

On the belly end of the curve, the 15.12.32 maturity traded at the rate of 11.60%.

The Treasury Bill auction scheduled for today, will have a total amount of Rs. 100 billion on offer. This will comprise of Rs. 50 billion offered on the 91-day maturity, Rs. 35 billion on the 182-day maturity and Rs. 15 billion on the 364-day maturity. This is broadly in line with the maturity corresponding to the scheduled auction, which is estimated to be approximately Rs. 103.54 billion.

To recap: At the weekly Treasury Bill auction held last Wednesday, weighted average yields increased across all three maturities for a second consecutive week. The sharpest upward adjustment was recorded at the shorter end, with the 91-day and 182-day Bills rising by 9 basis points each to 10.23% and 10.30%, respectively. In comparison, the 364-day Bill edged up by just 3 basis points to 10.20%, reinforcing the recent front-end bias in the re-pricing of the Treasury Bill yield curve.

The auction successfully raised the entire Rs. 100 billion offered at the first phase of competitive bidding. However, the bulk of the accepted amount was raised from the 91-day tenor, which saw acceptance exceed its offered amount, while the 182-day and 364-day maturities raised less than their respective offered amounts. An additional amount of Rs. 7.73 billion was raised at phase two of the auction on the 182 day.

In the money market, the net liquidity surplus was recorded at Rs. 134.77 billion yesterday. An amount of Rs. 120.97 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 8.25%. In addition, the Domestic Operations Department (DOD) of the Central Bank of Sri Lanka drained out an amount of Rs. 13.80 billion by way of overnight repo auction at a weighted average rate of 8.75% as against an offered amount of Rs. 40 billion.

The weighted average rates on overnight call money and Repos were recorded at 9.17% and 9.19% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing at the day at Rs. 334.85/335, holding steady against its previous day’s close of Rs. 334.90/335.00.

The total USD/LKR traded volume for 6 July was $ 66.70 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)