Friday Jul 17, 2026

Friday Jul 17, 2026

Wednesday, 22 April 2026 00:05 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market continued to see yields holding broadly steady for a second consecutive session, reinforcing the ongoing consolidation phase.

External conditions remained the key influence on market sentiment. Middle Eastern geopolitical tensions continued to weigh on investor outlook. Meanwhile, crude oil prices, although slightly moderated, stayed elevated.

Market activity remained subdued, as participants stayed cautious amid mixed geopolitical signals and uncertainty over global macro direction. Investor behaviour continued to reflect a defensive stance, with most players adopting a wait-and-see approach in the absence of clear directional triggers.

Despite the muted tone, transaction volumes were supported by selective block trades, providing intermittent liquidity to the market.

Overall, the market maintained a sideways bias, with limited catalysts to drive yields decisively in either direction in the near term.

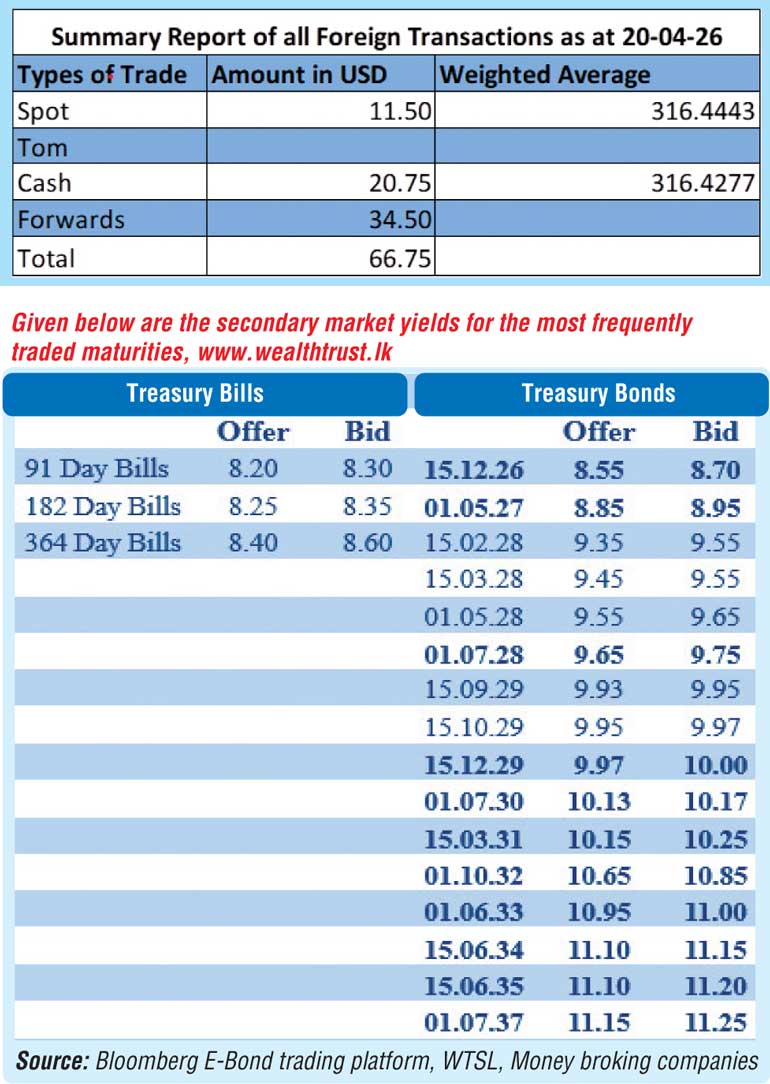

In secondary Bonds market, the 01.08.26 maturity traded at the rate of 8.40%. The 15.09.27 maturity traded at the rate of 9.00%. The 2029 tenors saw rates drop on robust concentrated demand. The 15.09.29 and 15.10.29 maturities traded lower at the rates and down the ranges of 9.95% and 10%-9.95% respectively. The 01.03.30 maturity traded at the rate of 10.07%. The 01.11.33 traded at the rate of 11%.

This comes ahead of the Treasury Bill auction due today, which will have a total amount of Rs. 110 billion on offer. This will comprise of Rs. 45 billion offered on the 91-day maturity, Rs 35 billion on the 182-day maturity and Rs. 30 billion on the 364-day maturity.

For reference, the Treasury Bill auction conducted last Wednesday extended the upward trajectory and saw weighted average yields increase across the board for the fourth consecutive week. Accordingly, the yield on the 91-day Bill rose by 20 basis points to 8.15%, the 182-day Bill increased by eight basis points to 8.22%, while the 364-day Bill saw an uptick of seven basis points to 8.52%.

The auction was undersubscribed at the first phase in competitive bidding, raising only Rs. 58.52 billion or 65.02% out of the Rs. 90 billion total offered amount. The bid-to-cover ratio stood at 1.51 times. Notably, further to the T-Bill auction, Rs. 25.52 billion was raised at the phase II of the auction boosting the aggregate accepted amount of the issuance was Rs. 84.04 billion.

The total secondary market Treasury Bond/Bill transacted volume for 20 April was Rs. 9.71 billion.

The net liquidity surplus stood at Rs. 123.32 billion yesterday. As an amount of Rs. 151.52 billion was deposited at Central Bank’s SDFR (Standing Deposit Facility Rate) of 7.25% while an amount of Rs. 28.20 billion was withdrawn from the Central Bank’s SLFR (Standing Lending Facility Rate) of 8.25%.

In the money markets, the weighted average rates on overnight call money and Repos remained mostly unchanged at 7.68% and 7.70% respectively.

Forex market

The USD/LKR rate on spot contracts was seen closing the day depreciating to Rs. 316.50/316.75 against its previous day’s closing level of Rs. 316.40/316.90.

The total USD/LKR traded volume for 20 April was $ 66.75 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)