Tuesday Jun 23, 2026

Tuesday Jun 23, 2026

Monday, 22 June 2026 00:08 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary Bond market recorded a strong rally last week, supported by improving global and domestic fundamentals. Investor sentiment turned bullish following reports of the signing of an interim US-Iran peace agreement, which in turn contributed to a sharp decline in Brent crude oil prices, easing inflationary and external sector pressures.

Domestically, confidence was further boosted by continued fiscal consolidation, with the Government recording a budget surplus of Rs. 105 billion during January–April 2026 compared to a deficit of Rs. 261.6 billion in the corresponding period of 2025.

Against this backdrop, aggressive buying interest emerged across the yield curve, driving yields sharply lower amid elevated activity and transaction volumes. The positive momentum was reflected at the weekly Treasury Bill auction, where rates declined for the first time in five weeks, reflecting the broader downward adjustment in market yields.

As a result, last week saw yields decline and two-way quotes closing lower despite some minor profit taking pressure towards the very latter part of the week and as the news of postponed US-Iran talks slightly tempered optimism over ceasefire progress.

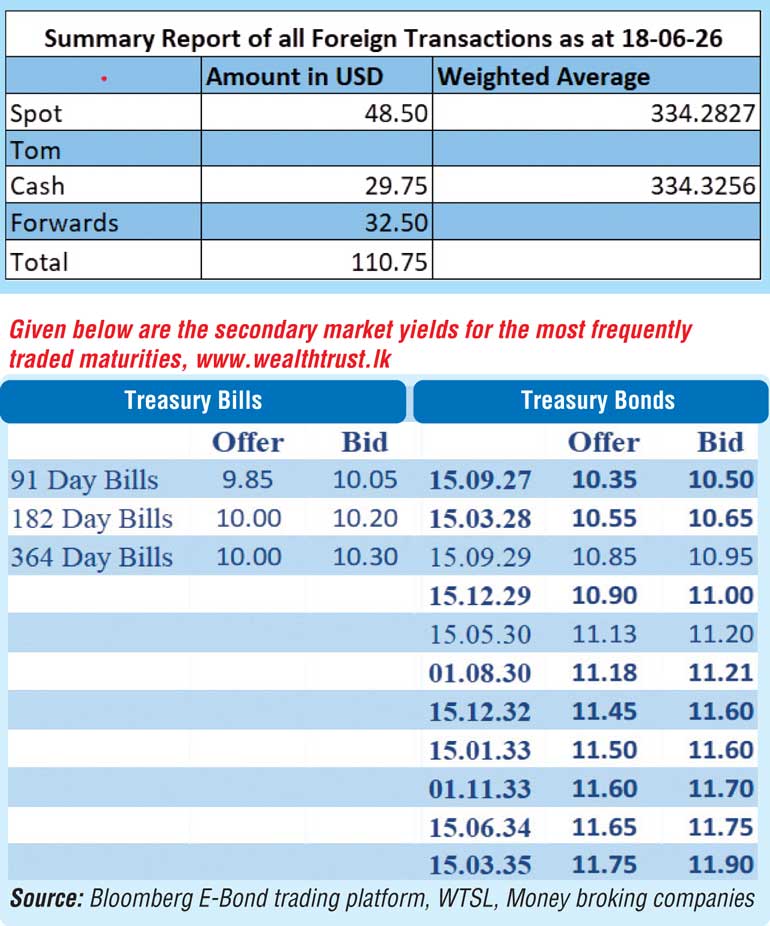

In the secondary Bond market, the 15.12.26 maturity traded down from an intraweek high of 10.25% to a low of 10.05%. In the 2028 space, the 15.02.28 maturity traded down from an intraweek high of 10.95% to a low of 10.60%. The 01.05.28 maturity traded down from an intraweek high of 10.95% to a low of 10.65%, while the 01.07.28 maturity traded down from an intraweek high of 11.00% to a low of 10.65%. The 15.10.28 maturity traded down from an intraweek high of 11.00% to a low of 10.70%.

Moving into the 2029 segment, the 15.12.29 maturity traded down from an intraweek high of 11.30% to a low of 10.85%. In the 2030 space, the 01.03.30 maturity traded down from an intraweek high of 11.35% to a low of 10.95%, while the 15.05.30 maturity traded down from an intraweek high of 11.65% to a low of 11.05%. Similarly, the 01.08.30 maturity traded down from an intraweek high of 11.75% to a low of 11.15%.

Further along the curve, the 15.12.32 maturity traded down from an intraweek high of 11.83% to a low of 11.45%. The 15.01.33 maturity traded down from an intraweek high of 12.00% to a low of 11.50%, while the 01.06.33 and 01.11.33 maturities traded down from an intraweek high of 11.70% each to a low of 11.60% and 11.55% respectively.

The 15.06.34 maturity traded down from an intraweek high of 11.90% to a low of 11.60%. At the longer end, the 15.03.35 maturity traded down from an intraweek high of 12.25% to a low of 11.75%, while the 15.08.36 maturity changed hands at the rate of 11.90%.

At the weekly Treasury Bill auction conducted last Wednesday, rates dropped for the first time in five weeks. This reflected the downward adjustment in secondary Bond market yields.

The weighted average yield on the 91-day Treasury Bill decreased by 7 basis points to 10.02%, the 182-day bill saw its rate drop by 11 basis points to 10.16%. However, the 364-day tenor remained unchanged at 10.16%. As such the inversion in the T-Bill yield curve was corrected.

The auction raised the entire Rs. 70 billion offered at the first phase in competitive bidding. Total bids received amounted to 1.85 times the offered volume. Notably, the bulk of the accepted amount was raised from the shorter tenor three months which raised more than its respective offered amount. The other two tenors saw acceptance sharply below their respective offered amounts.

Meanwhile, the foreign holdings of rupee-denominated Government securities increased marginally for the second consecutive week. Accordingly, the total foreign holdings increased by Rs. 2 million to Rs. 121.35 billion during the week ended 18 June.

In the money Market, the total outstanding liquidity surplus in the money market was recorded at Rs. 31.25 billion against its previous weeks of Rs. 62.57 billion. The weighted average interest rates on Call Money and Repo stood at 9.22% and 9.24% respectively at the close of the week as compared to 9.19% and 9.23% respectively the previous week.

In the Forex market, the USD/LKR rate on spot contracts was seen closing at Rs. 333.85/334.25 as against its previous weeks closing of Rs. 335.50/336 trading from an intraweek high of Rs. 327.50 to a low of Rs.335.50.

The daily USD/LKR average traded volume for the first four trading days of the week stood at $ 86.00 million.

(References: Public Debt Management Office - Ministry of Finance, Central Bank of Sri Lanka, Bloomberg E-Bond Trading Platform, Money Broking Companies)