Saturday Jul 04, 2026

Saturday Jul 04, 2026

Monday, 3 October 2016 00:01 - - {{hitsCtrl.values.hits}}

As reported by Lloyd’s Loading List, the impromptu boost to the Asia-Europe spot market in the immediate aftermath of the Hanjin collapse was always unlikely to be sustained, given market fundamentals and the latest Shanghai Containerised Freight Index (SCFI) shows rates on the Asia-North Europe and Asia-Mediterranean trades falling by more than 20% to $ 764 per TEU and $ 667 per TEU respectively.

But on the transpacific trade, where Hanjin had a bigger market share, carriers have taken full advantage of the sudden premium for slot space on the back of Hanjin’s vessels being pulled from service. Spot rates on routes from Asia to either coast of the US have rocketed since the start of the month and even a slight drop off on the SCFI last week, where rates on the Asia-US East Coast and Asia-US West Coast trades fell 0.6% to $ 2,433 per FEU and 0.9% to $ 1,726 per FEU respectively, will do little to dampen the mood of carriers. At the start of the month, freight rates to the US West Coast from Asia were as low as $ 1,153 per FEU, while those to the US East Coast stood at $ 1,684 per FEU.

Avoiding another bankruptcy, not easy

With 33 Hanjin Shipping vessels and all their containers still unable to be unloaded three weeks after the bankruptcy of the world’s seventh largest container line, profound questions regarding the risks of ocean container transportation are being raised in corporate  boardrooms throughout the world. The questions boil down to these: Could the collapse have been anticipated and avoided? What can be done to protect the company from another potential carrier failure? While these are the right questions of course, the answers unfortunately aren’t simple or straight forward.

boardrooms throughout the world. The questions boil down to these: Could the collapse have been anticipated and avoided? What can be done to protect the company from another potential carrier failure? While these are the right questions of course, the answers unfortunately aren’t simple or straight forward.

There is no question that risk, or at least perception of risk, by shippers regarding container lines is significantly heightened following the Hanjin collapse. The bankruptcy shatters the complacency that major carriers are immune to failure and can stomach prolonged years of low rates and financial losses, Drewry stated. Shippers furthermore had every reason this year to be concerned about Hanjin’s finances. The company had in recent years experienced bloated losses and staggeringly high debt levels, all of which was out in the open.

Since 2013, Drewry Financial Research Services has warned that Hanjin was dangerously leveraged and living on borrowed time, Drewry said. But then again shippers earlier this year could have been just as concerned about Hyundai Merchant Marine, which is now a much safer bet. At different points in recent years they could have been justifiably concerned about deteriorating finances at other carriers as will. But none of those other carriers went belly up. What was different about Hanjin.

The answer is that within the closeted, internecine world of the South Korean business elite a high stakes drama was unfolding almost entirely behind closed doors, that suddenly the government would sever the financial lifeline for its two major container lines, which thousands of its exporters rely on, was an unprecedented act that only the most informed business risk analysis could have anticipated. A true insider might have seen this act coming, but it was invisible as far as the wider world was concerned, reports JOC.

Automated trucks, closer to reality

The vision of autonomous trucks and other vehicles sharing US highways is closer to reality with the release of federal guidelines for the regulation of autonomous vehicles (AV). The Department of Transportation released an autonomous vehicle policy that includes guidelines for vehicle manufacturers, a model policy for states and a discussion of current regulatory tools and new tools that could accelerate the development and use of AVs. The new policy is an attempt by regulators to catch up with technology that is rapidly evolving and moving off the drawing board and onto the streets of cities such as Pittsburgh.

Uber last week launched an autonomous taxi service in the Iron City, drawing criticism from safety advocates who claimed Pennsylvania hasn’t yet developed laws or regulations on how and where highly automated vehicles or ‘HAVs’ could or should be deployed. The federal policy on HAVs isn’t a regulation, but at 116 pages it’s more than a suggestion. It clearly demonstrates federal regulators see safety benefits in more autonomous vehicles. 94% of crashes on US roadways are caused by a human choice or error.

National Highway Traffic Safety Administrator Mark Rosekind said in a statement ‘We are moving forward on the safe deployment of automated technologies because of the enormous promise they hold to address the overwhelming majority of crashes and safe lines’. (JOC)

Overcapacity will continue for years

To fully appreciate the enormous overcapacity predicament container lines find themselves in, consider these numbers a record 500,000 twenty-foot equivalent units will be scrapped by the end of the year and the idle capacity is more than 1.5 million TEUs. Yet even with 2 million TEUs out of service, around 10% of the global fleet container shipping supply will remain above demand for containerised transport for at least the next two years, according to maritime analysts.

Alphaliner’s Tan Hua Joo said demand growth will not be more than 2% in the next two years. He said even if the scrapping rate were to continue at the current level, next year’s growth in supply will only be brought down from 6% to 5%. The scrapping is not sufficient to address the demand-supply gap, he told the Global Liner Shipping Asia Conference in Singapore. Ona year-to-year basis, 2016 will have the lowest ever annual growth recorded in container ship supply at 2.9%. That is an all-time low, but will unfortunately bring no recovery in the container markets.

Camille Egloff, Partner and Managing Director at Boston Consulting Group, said BCG had run a projection looking at where demand would go in the next five years. It arrived at an annual growth rate of under 4% at best if everything goes right and slightly more than 2% if everything goes wrong. Supply growth would be around 3.7%, which wouldn’t help narrow gap between supply and demand. If you were to rebalance the supply and demand gap, you would have to remove another 100 supper large vessels form the global fleet, she said.

Hanjin Shipping’s collapse immediately removed around 600,000 TEUs form service, but much of that capacity will eventually find its way back to work.

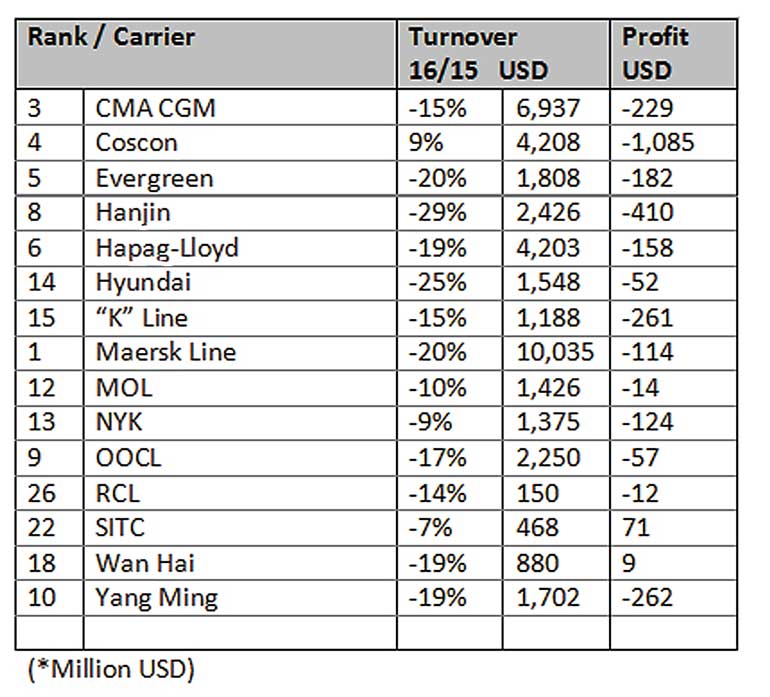

Top shipping lines continue to bleed

Altogether, fifteen top carriers posted their financial results for the first half of 2016, or first three months in case of the Japanese. Thirteen of them were loss making, with only SITC and Wan Hai making small gains. Their combined minus was $ 2.9 billion, excluding the approximately combined $ 1.5 billion lost by APL (before becoming part of CMA CGM) and China Shipping (Before being integrated into Coscon). Turnover went down for all of them, by up to 29%, except for Coscon.

Need to withdraw state support from liner shipping

Speaking to Lloyd’s Loading List, the impact on global supply chains became clear of Hanjin Shipping’s entry into receivership, Peter Sand, Bimco’s Chief Shipping Analyst said the container shipping sector had consistently been in the red in recent years and some lines had become reliant on state hand-outs to survive, as overcapacity and poor demand drove down freight rates. Bimco only comments on the market, not individual companies acting in it, but what I can say is that the global supply chain has seen its normal business routines disrupted and much extra work is needed and not only by lawyers but also competing liner companies to resolve it.

What it proves, if anything, is that the die-hard government support of companies in shipping and shipbuilding may not be all conquering any more. This is good news; the industry is struggling to make money every single day, but right now is losing money every single day. A resetting of cost levels is what is needed for most companies. Sand said that while this would be hard to achieve for many liner companies, or impossible for those that purchased vessels at peak prices, it was necessary if the industry was to return to profitability sooner rather than later.

The fundamental balance between supply and demand is not going to change permanently due to any bankruptcy, added Sand. The capacity/ships will simply be owned by someone else, not sold for outright demolition.

(The writer a Maritime Economist is a Chartered Fellow (Logistics Transport), Chartered Shipbroker (UK), Chartered Marketer (UK) and a University of Oxford Business Alumni. He is also a Fellow of NORAD/JICA and Harvard Business School (EEP).)