Friday Jul 31, 2026

Friday Jul 31, 2026

Friday, 24 April 2026 03:40 - - {{hitsCtrl.values.hits}}

Sri Lanka’s location and potential still matter. But potential isn’t enough. With opportunities opening up and some traditional destinations losing appeal, this is exactly the moment for Sri Lanka to become easier, clearer and more investable. Sri Lanka cannot go on selling the promise of investment while tolerating a system that too often frustrates it. If we are serious about competing for capital, we must become serious about fixing what is broken

Sri Lanka’s location and potential still matter. But potential isn’t enough. With opportunities opening up and some traditional destinations losing appeal, this is exactly the moment for Sri Lanka to become easier, clearer and more investable. Sri Lanka cannot go on selling the promise of investment while tolerating a system that too often frustrates it. If we are serious about competing for capital, we must become serious about fixing what is broken

The problem

The problem

Over the years, I have heard the same frustration from investors. They arrive with genuine interest, spend time exploring opportunities, hold meetings, visit sites, discuss structures, and then somewhere along the way their enthusiasm begins to drain away. The opportunity may still be there, but the process starts to exhaust them.

Facilitating foreign investment into Sri Lanka is one of the things I do, and I have seen from close quarters how often serious investor interest gets slowed down or discouraged by the way the system works. I have also dealt with the same bureaucracy myself as a local businessman.

At the same time, I have been involved in successfully implementing greenfield hotel projects in Sri Lanka after the war ended. Those projects did get done. But they did not get done because the system was clear, efficient or welcoming. They got done largely because of local knowledge, persistence, and the ability of local partners to keep pushing until things moved.

That, in many ways, is the heart of the problem. Investment can happen in Sri Lanka. It does happen. But too often it happens despite the system rather than because of it.

The promise and the delivery

Sri Lanka has spent years telling the world that it wants investment. Governments have held roadshows, promoted opportunities, spoken about investor confidence, and highlighted the country’s location and potential. The US State Department’s 2025 Investment Climate Statement says foreign investors in Sri Lanka report high transaction costs, unpredictable policies, and opaque procurement procedures.

But wanting investment in theory and making it happen in practice are not the same thing.

We need to move away from the assumption that investors will come here, find their own way through the maze, and sort it all out for themselves. That is not how serious competition for capital works. Capital has options. Investors can go to many other countries in the region and beyond where the path is clearer, the interfaces are simpler, and the State makes a visible effort to help projects move.

I say that not in theory, but from experience. In other jurisdictions where I have invested or worked with investment processes, including Malaysia, Australia and Vanuatu in the South Pacific, I have found the experience clearer, more welcoming and more straightforward. Sri Lanka is competing for that capital. It is not entitled to it. We still behave too often as though investors will tolerate whatever the system gives them. They will not.

The difficulty is that while Sri Lanka promotes itself actively, too many investors discover that the delivery does not match the promise. We market opportunity, but too often fail to match that with clarity, speed, coordination and follow-through.

From pillar to post

Too often, the experience is one of being sent from pillar to post. One agency asks for one thing, another asks for something else, and a third gives a different interpretation. One adviser says one thing, another says something different. What should be a structured process becomes uncertain, repetitive and unnecessarily slow.

Even basic matters become more cumbersome than they should be. Tax registration, approvals, company matters, utility connections, permits and compliance often involve repeated visits, repeated document requests, and repeated uncertainty over who is actually responsible for moving the matter forward.

Most striking is not only the bureaucracy itself, but the instinct behind it. Too often, officials are ready with reasons why something cannot be done, but much less ready to explain how it can be done. There is too little ownership and too little urgency.

And if this is frustrating for local business people who know the system, the language and the terrain, then it is easy to see how foreign investors become discouraged.

At the outset

In some cases, the frustration begins even before a project has properly started.

Visa handling is a good example. Business visitors, potential investors and technical personnel often find extensions, renewals and re-entry arrangements bureaucratic and time-consuming. A friend of mine currently dealing with the process described it in simple terms: half a day can disappear just to sort out an extension, and if you leave the country within that period, the arrangement can become invalid and need to be done all over again.

That may sound like a small operational irritation, but it is not. It is part of the investor’s first impression of the country. If a serious investor or key technical person finds it difficult even to enter, stay and renew in a predictable way, that already tells them something about the wider system they are dealing with. Public business groups have made the same point, warning that Sri Lanka’s business-visa difficulties were hurting economic activity and investor confidence.

When projects start to unravel

This is not just a matter of private complaints. We have seen it in public, high-profile cases.

United Petroleum entered Sri Lanka’s liberalised fuel market and then exited within months, reportedly after frustration over deviations from commitments and an operating environment it found unsustainable. The Ambuluwawa cable car project became another example. The investor involved said money had already been spent and approvals obtained, yet progress still ran into obstruction and uncertainty. Sinopec’s proposed refinery in Hambantota is not a failed investment, but it remains a useful example of how even one of the largest proposed FDI investments in the country can stay bogged down for a very long time while key terms, expectations and conditions remain unresolved.

Adani’s wind project is more complicated. One can reasonably argue that the project may not necessarily have been in Sri Lanka’s best interests in the form in which it was proposed. But even so, when a large, highly publicised foreign investment becomes entangled, delayed, renegotiated and then falls away, it still sends a message internationally and causes reputational damage.

Different sectors, different investors, different facts, but the same broad signal: in Sri Lanka, moving from announcement to execution remains far less certain than it should be.

When the State forgets its own promises

The problem does not end with getting investors in. It also extends to whether the State can be trusted to stand by the terms on which investment was made.

That is why the recent debate around RANSI — the Rupee Account for Non-Resident Sri Lankan Investment — matters. In reality, it raises a much larger question: if Sri Lanka made specific commitments to attract certain investors, can those investors still rely on those commitments years later? The recent Daily FT article on the subject set out the legal and policy history behind that concern in considerable detail. (See https://www.ft.lk/columns/The-Ghost-in-the-Gazette/4-790493)

I know of several investors who have been caught up in this issue, and it has left a bad taste. That matters, because serious investors do not think only about entry. They think about the full life of an investment — entry, operation, taxation, repatriation and exit. Confidence has to survive the entire journey.

When governments change, commitments should not

One of the most damaging signals any country can send is that major understandings may not survive a change in administration.

Sri Lanka has examples of this too. The Japanese-funded light rail project and the East Container Terminal arrangement both became casualties of political change and altered policy direction. One may debate the merits of the projects themselves, but the wider signal was unmistakable. If commitments reached under one Government can be reopened, reversed or abandoned under another, investors and partner countries will naturally question how durable any commitment really is.

This is not only a policy issue. It is a credibility issue.

The corruption question

Then there is the issue many people speak about privately and only some speak about openly: corruption.

Japanese diplomats have been unusually candid on this subject. Sri Lanka’s own anti-corruption authorities, CIABOC, have also acknowledged that investors face corruption-related difficulties in projects. That alone should tell us that this is not idle gossip.

The reality is that while some embassies speak openly, others say similar things behind closed doors. I have heard such concerns myself over the years, from diplomatic circles and from investors. In different forms, I have also encountered the broader culture that allows such suspicions to thrive: opacity, delay, discretion, and too little accountability for who is holding up what and why.

Corruption does not always arrive in dramatic form. Sometimes it appears as unexplained delay, repeated obstacles, and the lingering feeling that files do not move on merit alone. Whether explicit or implied, the effect is the same. Trust erodes.

The mindset issue

Beyond forms, files and delays, there is also a deeper problem of official culture.

More than once, the impression left on investors has been that the system does not really want them there. The hurdles keep coming, and instead of being told how to proceed, they are mostly told what cannot be done.

That may sound harsh, but it reflects what many investors privately say. In different ways, I have felt the same thing myself. There is too often a lack of ownership, a reluctance to facilitate, and an instinct to pass the problem along rather than resolve it. Public commentary in Sri Lanka has also described bureaucratic “negative thinking”, fear-based paralysis in the public sector, and a failure of working attitudes to align with what enterprise and investment require.

This matters because no amount of policy language will fully solve the issue if the mindset remains the same. A portal can be built, a circular can be issued, a new slogan can be coined — but if the person at the desk is still acting as a gatekeeper rather than a facilitator, the obstacle remains.

It was not always like this

I remember a different approach.

During the Premadasa period, I was involved in a project that benefited from a very different official culture. What I remember was not perfection, but urgency. There was a can-do attitude. There was a willingness to solve problems rather than explain them away. At one point, we had the unusual experience of a Government agency calling to ask when they could come and install the transformer. In other words, they were pushing the project forward even before we were ready.

That may sound like a small anecdote, but it says a great deal. It reflected a system in which investment was treated as something to be helped along, not slowly suffocated by process.

This is worth remembering because it means Sri Lanka’s present condition is not inevitable. We have seen before that when there is political will, ownership and expectation, things can move. Retrospective commentary on that period has described investors as being served from one centre rather than pushed from pillar to post.

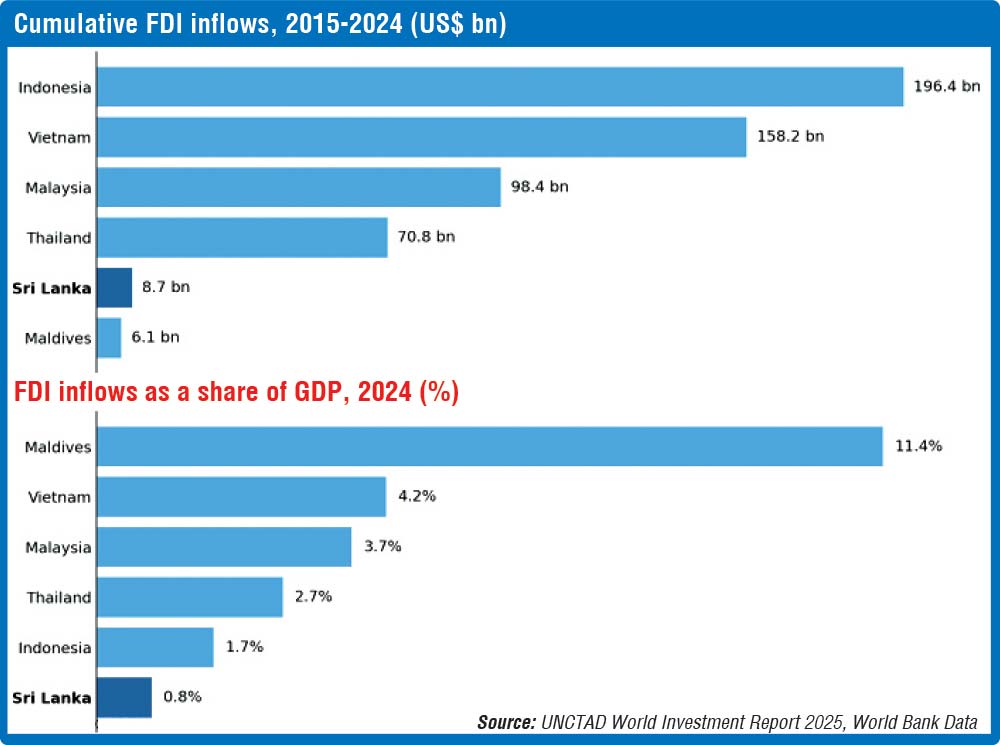

How Sri Lanka compares

Sri Lanka has underperformed on foreign direct investment over the last decade, both in absolute terms and as a share of GDP. Countries such as Vietnam, Malaysia, Thailand and Indonesia have attracted far larger volumes of foreign capital, while the Maldives has outperformed Sri Lanka even on a small-state basis in relation to the size of its economy. UNCTAD and World Bank data support that comparison.

The comparison becomes even clearer in the numbers.

The point is not simply that Sri Lanka is smaller. Even on an apples-to-apples basis, it attracts less foreign investment than the regional peers it competes with.

That is important because it removes one easy excuse.

And the contrast is not only visible in the data. I have seen it personally elsewhere. In Malaysia, in Australia, and in Vanuatu in the South Pacific, the process I encountered was clearer, more structured, more welcoming and easier to follow. There were clearer contact points, clearer checklists, and more practical effort to help the investor understand the pathway.

None of those places is perfect. But the difference in usability and attitude is noticeable.

The business case

Sri Lanka’s own apex private-sector body, the Ceylon Chamber of Commerce, has repeatedly called for many of the same reforms: a modernised BOI, a legally empowered one-stop shop, fixed timelines, digital integration, stronger accountability, and more effective commercial diplomacy. Its Vision 2030 work and Budget recommendations make that very clear.

That matters. It means the wider business community has already diagnosed the problem in broad terms.

The issue, then, is not lack of understanding. It is lack of execution.

Where the fix must begin

The first step in fixing anything is to admit that it is broken.

Sri Lanka’s investment process is broken in important ways. Not beyond repair — but broken enough that it now needs a serious, organised reform effort. The answer is not another roadshow or another speech.

We know broadly what needs to improve: a real one-stop shop with authority; timelines with accountability; integrated handling of investor and key-staff visas; more digital and risk-based approvals; sector-specific pathways, especially for large projects; and a deliberate effort to train the public service to see facilitation as part of its role.

I recall that in 2007 Malaysia took a practical step through PEMUDAH, a public-private initiative aimed at cutting bureaucracy and improving the way Government dealt with business. It is a useful example because it was practical, time-bound, and backed at a high level. Sri Lanka should consider something similar now: a high-level public-private investment facilitation reform initiative driven from the President’s Office, bringing together the BOI, Treasury, Immigration, Inland Revenue, Customs, key approval agencies, and representatives of the private sector and practitioners with direct experience.

Give such a body six months to map the investor journey, identify bottlenecks, benchmark regional peers, and produce a reform blueprint. Then give it a fixed period to oversee implementation, with public reporting.

That would at least show seriousness.

Sri Lanka’s location and potential still matter. But potential isn’t enough. With opportunities opening up and some traditional destinations losing appeal, this is exactly the moment for Sri Lanka to become easier, clearer and more investable. Sri Lanka cannot go on selling the promise of investment while tolerating a system that too often frustrates it. If we are serious about competing for capital, we must become serious about fixing what is broken.

(The author is a business leader specialising in hospitality, tourism, and investment. As Chairman and CEO of private companies and a board member of three publicly listed companies, he is actively engaged in hotel development and asset management in Sri Lanka. He can be contacted at: [email protected])