Tuesday Mar 31, 2026

Tuesday Mar 31, 2026

Tuesday, 31 March 2026 04:01 - - {{hitsCtrl.values.hits}}

Preamble

Preamble

Despite having a regasified LNG power generation capacity of 600 MW in Kerawalapitiya, Sri Lanka has chosen not to include LNG in its future energy mix because of the associated risks.

This is the Government's most prudent decision, and they deserve praise. Sri Lanka had planned to secure LNG by leasing a FSRU (Floating Storage Regassification Unit). If Sri Lanka had needed LNG during the Hormuz Strait closure by Iran, the penalties could have exhausted our limited USD savings.

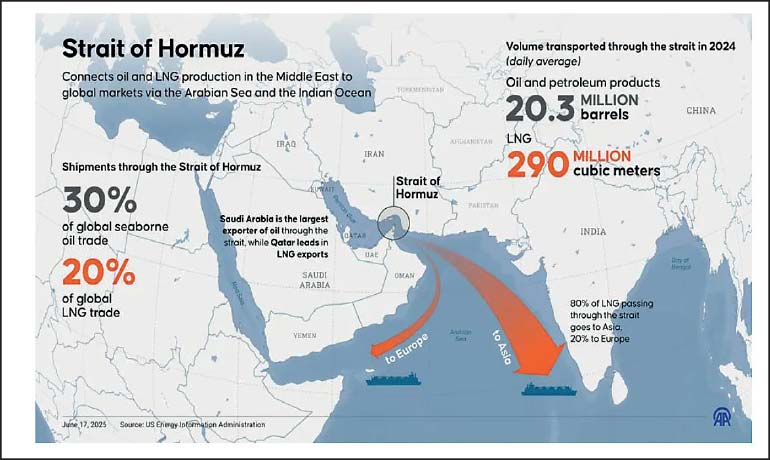

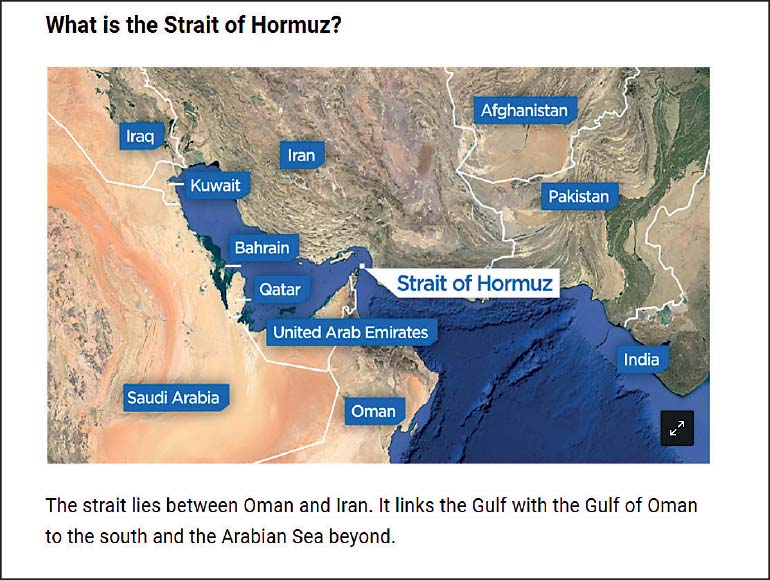

All LNG shipments from Qatar (the largest global supplier) via the Hormuz Strait have been terminated indefinitely. Given the risks to vessels and personnel during transit via Hormuz, the increased charter rates and often unavailable insurance cover is unaffordable as the risks cannot be mitigated. The global price of LNG has risen 300- 400%, making any power generation at this price uneconomical.

Sri Lanka lacks the political clout to obtain this scarce resource which is currently sought by major European countries and other powerful nations.

LNG became the alternative European energy supply after Nord Stream 1 and 2 stopped supplying natural gas from Russia to Europe through Germany due to the war in Ukraine.

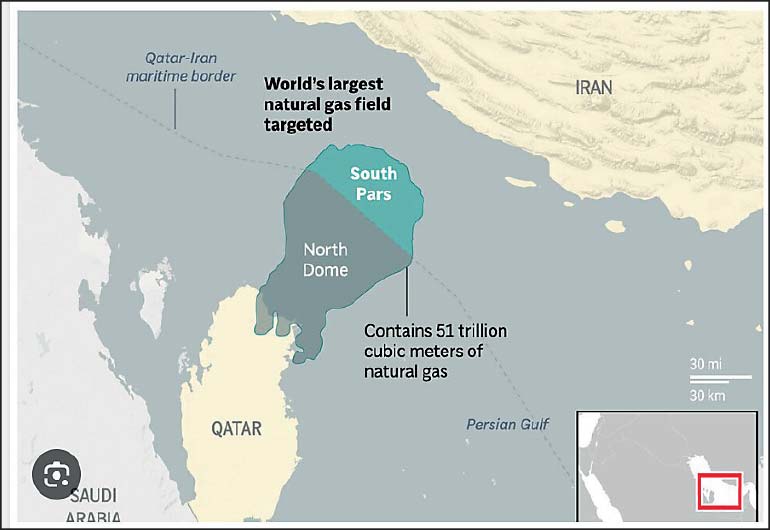

The recent Israeli strike on Iranian facilities linked to the South Pars gas field marks a significant escalation in the war, prompting a further lack of LNG in the market.

South Pars is part of the world’s largest natural gas offshore reserves. It is shared between Iran and Qatar, who calls their part of it the North Dome. The entire gas field contains an estimated 51 trillion cubic metres of utilisable gas, enough to supply the world’s needs for 13 years, according to Reuters. There are many reservoirs elsewhere being drained by more than one country under a ‘Zone of Cooperation’.

'Take-or-Pay' procurement risks and penalties payable

Long term LNG procurements are usually on ‘take-or-pay’ terms where the price of LNG is hedged.

Hedging is a risk management strategy used by oil companies and investors to protect themselves against unfavourable oil and gas price movements in the market. It essentially involves taking an opposite position in a related security: a financial instrument to offset potential losses in another.

A take-or-pay provision obligates the buyer to either purchase and receive a specified quantity of LNG within a contract year or to pay a predetermined amount for any LNG that is not taken. India faced such penalties of $ 1 billion in 2015 when RasGas (now Qatar Energy) imposed the penalty for India breaking a long-term contract for having bought 68% of the 7.5 mtpa of the contract.

At present, the LNG price has skyrocketed with an extreme shortage. Global demand is increasing as ongoing supply shortages persist without a foreseeable resolution. While these prices skyrocket during shortages, vested interests make the price decline slowly like a floating feather when supply returns.

The global premier supplier Qatar’s LNG supply is indefinitely shut down declaring Force Majeure . A price premium of 300 to 400% is expected, rendering the power generation tariff economically unfeasible and unaffordable.

LNG contracts are notoriously complex and cannot be compared to oil hedging contracts.Despite having procured oil over many decades, the simpler oil hedging contracts signed by Sri Lanka were flawed. In the 2008 oil hedging contract between GOSL and Standard Chartered Bank, a British Court imposed a $ 200 million settlement resulting from a flawed deal that cost the GOSL billions of rupees. This is a typical deal that went sour, and displayed GOSL’s inadequacies in these highly complex commercial matters. The writer notes that these deals were carried out by GOSL’s best technocrats who engaged highly paid consultants. The GOSL’s credentials in navigating these complex transactions or their technology is questionable. Even engaging consultants, SL is placed in a highly vulnerable position well into the future. Some cutting edge technology with FSRU is proprietary making such technology inaccessible even via consultants.

Plans to expand LNG power generation in SL remain ambitious, but risks must be carefully assessed based on past performance and current lessons with LNG in the volatile political landscape today.

Vessel leasing risks and penalties payable

Vessel leasing agreements are associated with significantly elevated levels of risk and penalties.

A comparable ‘look alike’ project for SL is the Bangladesh Moheshkhali FSRU project. Sri Lanka experiences monsoon-driven oceanographic conditions which increases in wave heights, like those observed in Bangladesh which mandates a disconnectable mooring system for the vessel.

A disconnectable mooring system is adapted where the floating installation has a propulsion system and a means of disengaging the installation from its mooring and riser systems during rising waves. This allows the installation to ride out severe weather or seek refuge under its own power for a specified design environmental condition. This is cutting edge technology even for India, where the writer was engaged for ONGC’s KG-98-2 floating production installation.

The commercial details of Bangladesh’s FSRU ought to be noted. Sri Lanka’s leased FSRU could reflect a similar commercial payment structure. This is the global industry practice in payment structure based elsewhere across Asia, Middle East, Africa and South America given the writer’s explicit experience.

In the comparable FSRU, Excelerate built the FSRU in Bangladesh under a Build-Own-Operate and Transfer (BOOT) basis and charged $0.49 per Mcf (1,000 cubic feet) against its service. Petrobangla paid an additional $0.10 per Mcf to cover other related costs, including fuel, tugboat operation, port facility usage etc.

In Bangladesh, regasified LNG from the terminal was sold on a take-or-pay basis to Petrobangla, which had back-to-back gas sales agreements with power plant owners, operators or other end-user consumers. The FSRU would have berthing and mooring facilities for LNG tankers with a capacity of 138,000 cubic metres. It had the capacity to supply around 500,000 Mcf per day of natural gas to Bangladesh's national gas grid. The capacity could be increased to around 700,000 Mcf per day. The Excelerate turret loading buoy vessel will process up to 3.5 mta LNG.

The fixed component capex day rate to be paid to Excelerate was $159,000 and an operating component of $46,000 per day. The capex day rate is payable for the fixed term of the lease for 15 years, irrespective whether LNG is procured and available or not for regassification. Usually, a significant portion of the operating day rate is also payable, even if the vessel is not utilised. However, a minor amount is deductible based on the amount of regasification.

Thus, the exposure (even if LNG is unavailable) is about $200,000/day for the 15 year fixed term duration. These conditions are per the usual Force Majeure terms as dictated by banks financing the project, such as today when LNG is unavailable for regassification. Long periods when LNG is unavailable could be considered a severe penalty when day rate of about $200,000 is payable with no power being generated. This could be of the same order in Sri Lanka. The Force Majeure terms are the most difficult terms to negotiate.

Reducing the lease duration from 15 years leads to a higher prorated capex day rate for the vessel.

The writer has negotiated complex commercial lease contracts for clients and received a Technical Excellence Award from Shell in recognition. Shell has been the global leader since 1976 in this complex technology with SBM. This cutting-edge technology is based in Ocean Engineering and Naval Architecture which subjects are not taught in Sri Lanka in any recognised form.

Early termination during the fixed term of the lease and penalties payable

An early termination usually results in a costly penalty to the client based on the remaining period of the fixed term of the lease. Even in the case of ‘Force Majeure’ under most conditions, the day rate is payable to the FSRU contractor for the remainder of the contract period.

These vessels usually have a negative value on completion of contract and become a liability, having a much higher cost of operating them in their poor condition. The vessel is also on occasion uninsurable for further operation, with too many ‘conditions of class’, namely flaws. These vessels have to face the ‘end of life’ burden as well upon termination. In Australia for instance, the vessel Northern Endeavour’s removal cost the tax payer $ 1 billion, upon termination of the lease.

GOSL should be mindful of the risks with engaging LNG today and into the future, where any such misguided adventures may bankrupt Sri Lanka again.

(The author brings over 50 years of experience in upstream oil and gas exploration, specialising in LNG contracting and infrastructure. He received the Technical Excellence Award from Royal Dutch/Shell and has worked with major global energy firms. He trained as an engineer at University of Ceylon, Peradeniya later at University College London as a post graduate Government scholar. He is contactable on nalin.gunas