Wednesday Jul 08, 2026

Wednesday Jul 08, 2026

Wednesday, 8 July 2026 00:18 - - {{hitsCtrl.values.hits}}

Sri Lanka’s private sector is facing a structural labour shortage. This is no longer a temporary disruption caused by the pandemic or the economic crisis. It is a long-term constraint driven by declining labour force participation, large-scale outward migration, demographic shifts, and outdated labour market intelligence.

Sri Lanka’s private sector is facing a structural labour shortage. This is no longer a temporary disruption caused by the pandemic or the economic crisis. It is a long-term constraint driven by declining labour force participation, large-scale outward migration, demographic shifts, and outdated labour market intelligence.

Across agriculture, construction, manufacturing, logistics, and services, businesses are struggling to fill vacancies. Recruitment cycles are longer, wage pressures are intensifying, and expansion plans are being delayed. The evidence confirms what employers already know: the labour constraint is real and widening.

A shrinking labour force

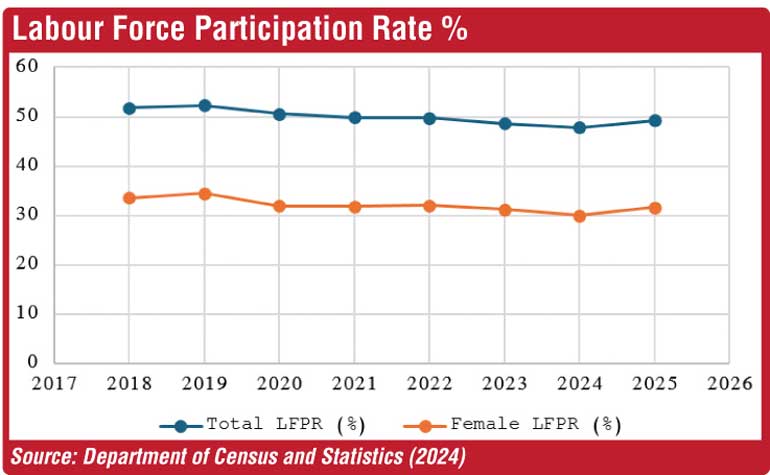

The Sri Lanka Labour Force Survey – Annual Report 2024, which defines the working-age population as persons aged 15 years and above, shows that the country’s Labour Force Participation Rate (LFPR) declined from 54.1% in 2017 to 47.4% in 2024. Female participation fell even more sharply — from 36.6% to 29.8% during the same period.

In absolute terms, Sri Lanka’s total labour force (15+ years) fell from 8.2 million in 2017 to 7.95 million in 2024. The most significant decline occurred among women, where the labour force contracted by approximately 338,000 workers.

In an economy with fewer than eight million active workers, this contraction is economically significant. It directly constrains production capacity, investment expansion, and long-term growth potential.

Sri Lanka’s challenge is not merely unemployment. It is declining participation.

Global comparison:

Sri Lanka is falling behind

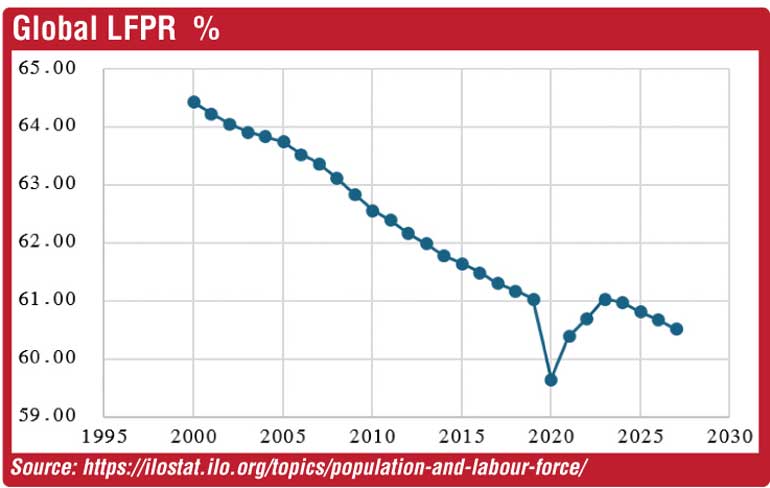

According to International Labour Organisation (ILO) global estimates, the world labour force participation rate currently stands at approximately 61%.

Sri Lanka’s LFPR at 47.4% is therefore significantly below the global average.

The gap is even more pronounced in female participation. Globally, female labour force participation averages around 48–50% depending on the region. Sri Lanka’s female LFPR at 29.8% is well below global norms.

This means Sri Lanka is not just experiencing a domestic participation problem — it is underperforming relative to global labour market standards.

Countries that sustain growth maintain high labour participation. Those that experience declining participation face long-term growth constraints.

Migration: A major supply shock

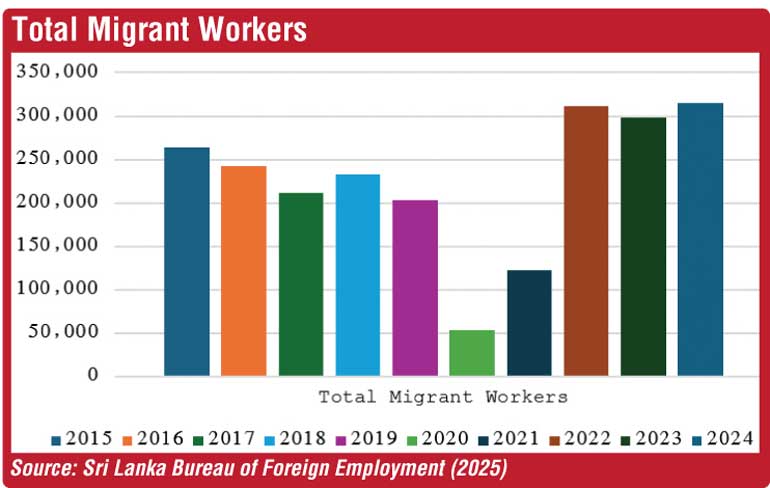

Outward migration has intensified the shortage. In 2024 alone, 314,786 Sri Lankans registered for foreign employment.

While remittances support macroeconomic stability, migration represents a significant domestic labour drain. More importantly, 77.66% of registered migrants fall into skilled categories. These are machine operators, technicians, construction workers, drivers, and skilled tradespeople — precisely the roles domestic industries struggle to replace.

Over 300,000 departures in a single year is substantial relative to the country’s labour base. The private sector is losing economically active workers at a time when production capacity must expand.

Structural imbalance in employment

Agriculture still accounts for 26% of total employment — approximately 2.07 million workers. Yet much of this employment remains informal and low productivity. Younger workers are exiting rural sectors, but there is no proportional rise in formal sector participation to offset the decline.

At the same time, Sri Lanka has not updated its comprehensive Labour Demand Survey since 2017. That survey estimated nearly 500,000 vacancies at the time, particularly in services and industry.

Seven years later — after a pandemic, debt crisis, currency depreciation, and migration surge — policymakers lack updated vacancy and skills-demand data. No serious labour reform can proceed without current labour demand intelligence.

Why importing labour is not the answer

Some argue that Sri Lanka can solve its labour shortage by importing workers from neighbouring countries. However, labour mobility depends on meaningful wage differentials and stable economic incentives.

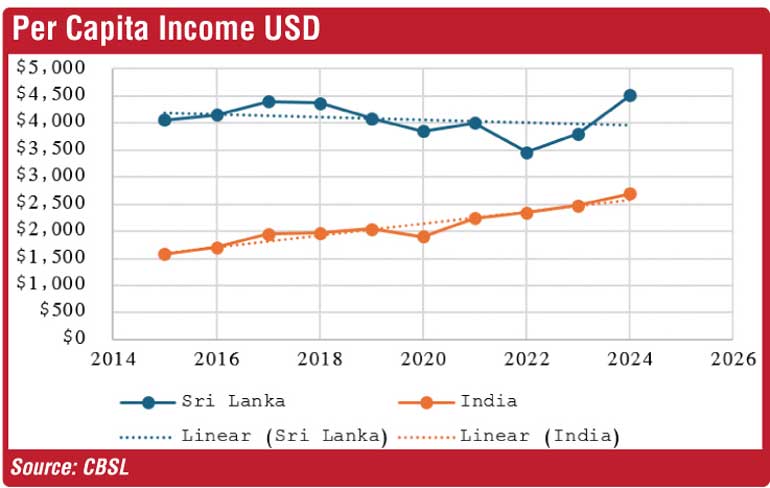

In 2024, Sri Lanka’s per capita GDP was approximately $ 4,516. India’s stood at about $ 2,695, Bangladesh’s at $ 2,769, and Pakistan’s at $ 1,812.

While Sri Lanka’s income appears higher, its volatility, limited industrial absorption capacity, and modest wage premium make it unlikely to attract sustained foreign labour inflows.

Importing labour is administratively complex and economically uncertain. It does not address the core issue — underutilised domestic labour potential.

Wage economics: Retaining local labour makes more sense

Average informal daily wages in India are roughly INR 1,000 per day. In Sri Lanka, comparable daily wages in manual sectors are around Rs. 3,000 per day.

When recruitment costs, visas, air tickets, accommodation, and compliance expenses are included, importing labour can cost as much as — or more than — improving domestic wages and retention strategies.

The labour shortage is therefore not purely a supply issue. It is also a matter of wage alignment and working conditions.

Untapped workforce: Women

The most immediate opportunity lies within Sri Lanka itself.

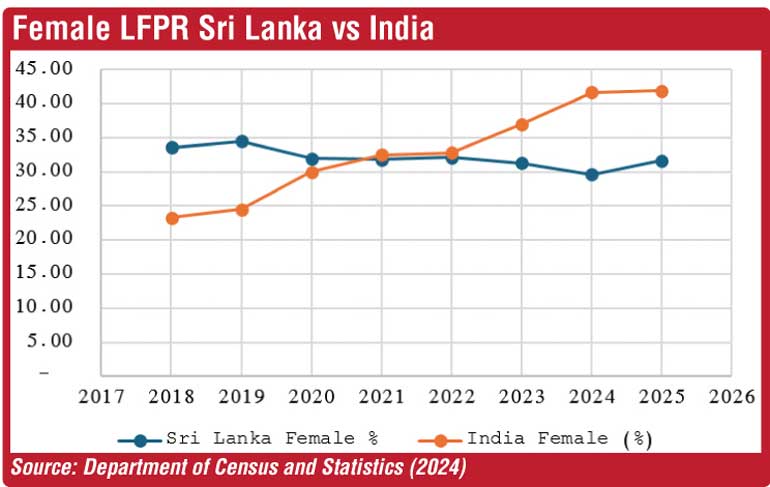

Female labour force participation stands at 29.8%. In India, it has risen to over 41%. Globally, it is close to 50%.

Raising female participation by even five to ten percentage points would significantly expand Sri Lanka’s labour force without importing workers or increasing migration.

This requires safe transport, flexible work arrangements, affordable childcare, and vocational alignment with industry demand.

Countries that mobilise female participation strengthen economic resilience. Those that fail to do so experience prolonged labour constraints.

Urgent need for new Labour Demand Survey

Sri Lanka cannot plan its growth strategy based on seven-year-old labour demand data.

A new National Labour Demand Survey in 2026 should measure:

Without predictive labour intelligence, education planning and industrial policy remain misaligned.

You cannot manage what you do not measure.

Conclusion

Sri Lanka’s labour shortage is structural. It is driven by declining participation, outward migration, and weak labour market intelligence — and it is compounded by participation rates well below global norms.

Importing labour is not the answer. The solution lies in expanding domestic participation, retaining skilled workers, aligning wages and incentives, and urgently updating labour demand data. If labour shortages are constraining growth today, addressing them must become a national priority.

(The author is CEO of Maxies Group and MPF (University of Kelaniya), ACA, ACMA, CGMA, CLSSBB)