Tuesday Jul 14, 2026

Tuesday Jul 14, 2026

Tuesday, 14 July 2026 05:10 - - {{hitsCtrl.values.hits}}

Inflation is driven largely by exchange rate movements, global prices, and supply conditions

The debate over Sri Lanka’s inflation target is ultimately one of timing and economic readiness rather than theoretical desirability. While the long-term benefits of lower inflation are well recognised, the near-term costs of enforcing a 2% target in the current context are significant

The debate over Sri Lanka’s inflation target is ultimately one of timing and economic readiness rather than theoretical desirability. While the long-term benefits of lower inflation are well recognised, the near-term costs of enforcing a 2% target in the current context are significant

Abstract

Abstract

As Sri Lanka approaches the scheduled review of its inflation target, and with public consultations underway, the debate over the appropriate level of the medium-term inflation target has intensified. Some policy commentators argue that reducing the current 5% target to 2% would strengthen macroeconomic stability, enhance policy credibility, and align Sri Lanka with global best practices. At first glance, this appears compelling - many advanced economies operate successfully with low inflation targets.

However, the appropriateness of any inflation target depends not on international norms, but on domestic economic realities. Sri Lanka operates under a flexible inflation targeting (FIT) regime, with a 5% target (and a ±2%age-point margin for assessing deviations from the target for accountability purposes), as set out in the Monetary Policy Framework Agreement (MPFA) signed in October 2023 between the Central Bank of Sri Lanka (CBSL) and the Minister of Finance under the Central Bank of Sri Lanka Act No. 16 of 2023.

This article argues that reducing the inflation target to 2% at this stage would be premature and potentially counterproductive. While the long-run benefits of low inflation are well established, the short- to medium-term economic impacts of enforcing a 2% target in Sri Lanka on growth, employment, debt dynamics, and financial stability etc., are likely to be significant. The current inflation objective remains better aligned with prevailing macroeconomic conditions, with any future recalibration best pursued gradually and in line with sustained structural improvements.

Introduction: Choosing the right target for the right economy

The determination of an inflation target is fundamentally about economic fit rather than imitation. It requires aligning the target with the structural characteristics of the economy, including the sources of inflation, the nature of shocks, and the strength of institutions. In Sri Lanka, these factors point to an economy where inflation is neither smooth nor fully controllable through monetary policy alone.

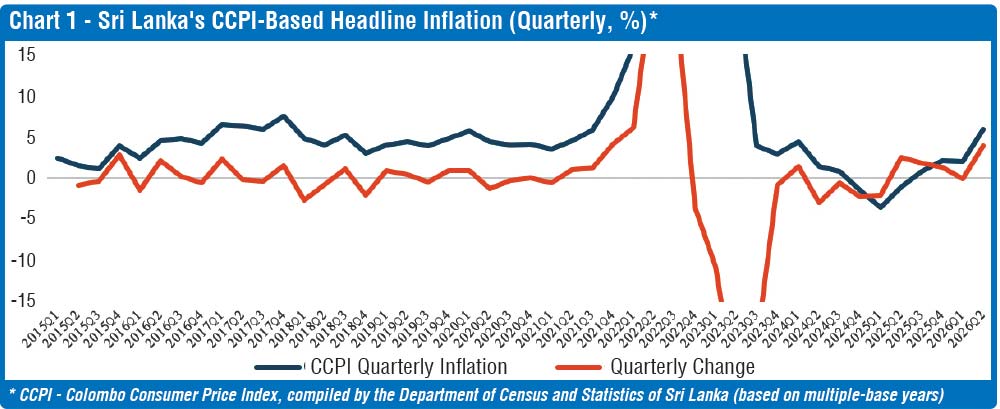

Chart 1 shows that inflation dynamics have been highly volatile and subject to large, abrupt shifts, rather than evolving stably and predictably. (The chart axis has been truncated to improve the visibility of periodic volatility, as the peak value of around 70% compresses the scale and obscures variations in the data.) Headline inflation rises from around 4–5% in the pre-2021 period to a peak close to 70% in 2022, before declining sharply to nearly 3% in 2023, turning negative around 2025, and subsequently rebounding toward 6% by mid-2026. This wide dispersion is accompanied by exceptionally large quarterly changes, pointing to significant underlying shocks.

The combination of sharp inflation surges followed by a descent into deflation underscores the sensitivity of inflation to both supply- and demand-side disturbances. In particular, the surge in 2022, followed by rapid disinflation and continued volatility, reflects an environment in which inflation is heavily influenced by exchange rate movements, energy price adjustments, and supply disruptions. Such dynamics are not characteristic of a conventional demand-driven inflation process that can be smoothly anchored around a very low target.

Although macroeconomic stability has improved since the crisis, underlying vulnerabilities remain. Public debt is still elevated, fiscal consolidation is ongoing, and the external sector continues to rebuild buffers, while inflation remains sensitive to external developments. These considerations underscore why Sri Lanka’s framework is explicitly flexible, allowing policymakers to balance inflation control with broader macroeconomic stability.

In this context, lowering the inflation target is not merely a technical recalibration, but a shift in the overall policy stance with far-reaching implications for the economy. Moving toward a very low target at this stage would risk undermining credibility and could necessitate disproportionately tight policy, increasing the likelihood of output losses and recurrent deflation episodes. Maintaining the target at around current levels, therefore, provides an important buffer against volatility and remains more consistent with observed inflation dynamics until greater stability and predictability are firmly established.

The case for lowering the target to 2%

The argument for reducing the inflation target to 2% is grounded in the long-standing view that lower and more stable inflation supports stronger economic outcomes over time. One of the central benefits is improved expectations anchoring. A lower target can serve as a clear and credible signal of the authorities’ commitment to price stability, helping to shape wage-setting and price-setting behaviour. Over time, this can reduce inflation persistence, enhance policy credibility, and improve the overall effectiveness of monetary policy.

There are also potential financial advantages associated with a lower inflation environment. Greater price stability is typically linked to lower inflation risk premia, which can translate into reduced borrowing costs for both the public and private sectors. In turn, this can support higher levels of investment and foster more sustainable economic growth, particularly when accompanied by strengthened macroeconomic credibility and institutional frameworks.

From an external perspective, a lower inflation target may help reduce inflation differentials with trading partners, thereby supporting external competitiveness, enhancing exchange rate stability, and improving the predictability of external balances. This consideration is especially relevant for a small open economy such as Sri Lanka, where external sector dynamics play a significant role in shaping macroeconomic outcomes.

In addition, there are incremental welfare gains associated with moving closer to price stability. Even moderate levels of inflation can distort relative prices, erode purchasing power, and introduce inefficiencies in resource allocation. A lower and more stable inflation environment can therefore enhance economic efficiency and improve welfare over the long run.

However, these benefits are neither immediate nor automatic. They tend to materialise gradually and are contingent on supportive preconditions, including strong policy credibility, well-anchored inflation expectations, and a stable macroeconomic environment. In the absence of these conditions, the transition to a significantly lower target may entail substantial adjustment costs, particularly in economies where structural vulnerabilities are still being addressed, as is the case in Sri Lanka.

Potential economic impacts of moving to 2% inflation target

While the benefits of low inflation are clear in theory, the economic impacts of enforcing a 2% target in the near term must be carefully considered.

Achieving a 2% inflation target would likely require maintaining higher real interest rates over a prolonged period, resulting in a sustained tightening of financial conditions. Elevated borrowing costs would reduce access to credit for both firms and households, while dampening private investment by raising hurdle rates and increasing uncertainty around returns, particularly in sectors that depend heavily on bank financing. In a recovering economy such as Sri Lanka’s, these effects could be especially pronounced. Private sector balance sheets are still adjusting, and confidence, although improving, remains sensitive to policy conditions. Prolonged tight monetary policy could therefore discourage capital formation, delay business expansion, and weaken the momentum of recovery, with adverse implications for productivity and medium-term growth. More broadly, persistently tight financial conditions risk delaying the transition from macroeconomic stabilisation to sustained expansion. While stabilisation focuses on restoring price and external balance, a durable growth phase depends on reviving investment, strengthening credit flows, and rebuilding economic dynamism. An extended period of restrictive policy aimed at achieving a very low inflation target could slow this transition, resulting in a more prolonged and uneven recovery path.

Tighter monetary policy would likely translate into weaker job creation and slower income growth, as higher borrowing costs dampen investment and consumption. Sectors that are particularly sensitive to credit conditions, such as construction, small and medium-sized enterprises, and consumer-facing services, would be disproportionately affected, given their reliance on bank financing and exposure to cyclical demand. A slowdown in these sectors can generate broader spillover effects, as they play a significant role in employment generation and income formation. In the Sri Lankan context, where the labour market is still recovering from the effects of the recent crisis, these dynamics carry important social implications. Employment gains remain uneven, informality is still widespread, and many households continue to face fragile income conditions. Slower job creation and subdued wage growth could therefore weigh on household consumption, increase vulnerability among lower-income groups, and risk reversing some of the recent improvements in economic stability. Moreover, weaker labour market conditions may interact with existing pressures such as elevated household debt and constrained access to credit, amplifying stress at the household level and potentially hindering a more inclusive and durable recovery.

Lower inflation, while beneficial in many respects, also has important implications for debt dynamics, particularly in the Sri Lankan context. A reduction in inflation typically translates into lower nominal GDP growth, which is a critical factor in stabilising and reducing public debt ratios. With public debt still elevated, slower nominal income growth weakens the denominator effect, thereby slowing the pace at which debt ratios can decline. At the same time, achieving and maintaining lower inflation often requires tighter monetary conditions, which can lead to higher real interest rates and increase the cost of servicing both existing and newly issued debt. This combination, slower nominal growth and higher real debt-servicing costs, can complicate fiscal consolidation efforts, requiring either larger primary surpluses or a more prolonged adjustment path. Moreover, tighter financial conditions may dampen economic activity, weakening revenue performance and further constraining fiscal space. These dynamics create difficult policy trade-offs, where efforts to enforce a very low inflation target risk undermining growth and, in turn, the sustainability of public finances.

Higher interest rates and slower growth can place significant strain on borrower balance sheets, elevating the risk of non-performing loans across both households and firms. As financing costs rise, debt-servicing burdens increase, while weaker income growth and reduced profitability constrain repayment capacity—particularly for highly leveraged sectors and small and medium-sized enterprises that are more sensitive to shifts in economic conditions. These risks are especially pronounced in a post-crisis context, where financial sector strengthening and balance sheet adjustment are still underway, and where legacy vulnerabilities and uneven recovery across sectors leave parts of the system exposed to renewed stress. A prolonged period of tight financial conditions could therefore not only slow the pace of recovery but also contribute to a deterioration in asset quality. In response, financial institutions may adopt more cautious lending practices, further tightening credit conditions. This, in turn, can delay balance sheet normalisation across the economy, constrain the flow of credit to productive sectors, and weaken monetary policy transmission. The result is a reinforcing feedback loop, where tighter policy dampens growth, heightens financial sector risks, and ultimately amplifies the overall macroeconomic adjustment.

A stricter inflation target may also have important implications for exchange rate dynamics in the Sri Lankan context. While tighter monetary policy could provide some short-term support to the currency, it may simultaneously reduce the exchange rate’s role as a key shock absorber in an economy that remains highly exposed to external disturbances. In recent years, exchange rate flexibility has played a critical role in absorbing pressures arising from external imbalances, terms-of-trade shocks, and capital flow volatility. Constraining this adjustment mechanism through a more aggressive inflation objective could shift a greater share of the adjustment burden onto domestic output and employment, potentially amplifying macroeconomic volatility during periods of stress.

Perhaps most importantly, a 2% target would significantly reduce policy flexibility. In a shock-prone economy such as Sri Lanka, where inflation is frequently driven by supply-side factors, including exchange rate movements, energy price adjustments, and external disruptions, the ability to accommodate temporary deviations is essential. A very low target leaves limited room to absorb such shocks without prompting a policy response, increasing the likelihood of tightening even when inflationary pressures are transitory. This, in turn, raises the risk of policy overreaction, where monetary policy responds to short-term or supply-driven movements that it is not well-positioned to offset. Such responses can impose unnecessary costs on output and employment, and may contribute to greater macroeconomic volatility over time. Frequent deviations from a very low target could also complicate policy communication and weaken credibility if the target proves difficult to achieve consistently.

By contrast, a more moderate inflation objective provides greater room to look through temporary shocks, smooth the policy response, and maintain a focus on medium-term price stability while supporting broader macroeconomic objectives. Preserving this degree of flexibility is particularly important in a structurally evolving and externally exposed economy like Sri Lanka, where overly rigid targets could ultimately undermine both stability and policy effectiveness.

Why a rapid shift to 2% is risky for Sri Lanka at this juncture

As discussed above, the potential economic costs of moving too quickly to a lower inflation target are substantial and well-documented in the literature. However, several important considerations appear to be underemphasised in the ongoing academic debate in Sri Lanka and warrant closer attention.

First, the cost of disinflation can be significant. Reducing inflation from moderate levels to around 2% is not a marginal adjustment; it typically requires a sustained period of tight monetary policy, which can suppress economic activity. These costs tend to be particularly pronounced when inflation is driven by supply-side factors rather than excess demand, limiting the effectiveness of policy tightening.

Second, Sri Lanka’s inflation dynamics are heavily influenced by external factors, including exchange rate movements and global price developments. As a result, monetary policy has only partial control over inflation outcomes. A very low target could therefore compel the Central Bank to respond to temporary or externally driven shocks, increasing macroeconomic volatility.

Third, there are important credibility considerations. If the target is set at a level that proves difficult to achieve consistently, repeated deviations could weaken confidence in the policy framework. Credibility is built through sustained and predictable outcomes, rather than through the adoption of more ambitious targets.

Fourth, financial and fiscal constraints amplify these risks. Higher real interest rates raise the cost of servicing both public and private debt, while lower inflation reduces nominal GDP growth, slowing the pace of debt reduction. This combination effectively tightens monetary and fiscal conditions simultaneously, complicating the overall macroeconomic adjustment.

Finally, the loss of policy space is a critical concern. Sri Lanka’s monetary policy framework places emphasis on the ability to absorb shocks and manage trade-offs in a flexible manner. Moving to a 2% inflation target would constrain this flexibility, reducing the capacity to accommodate temporary disturbances and potentially increasing the economy’s vulnerability to external shocks.

Lessons from international experience

International experience consistently demonstrates that successful disinflation is a gradual, institution-led process rather than an abrupt policy shift. Countries that have achieved and sustained low inflation, particularly at levels close to 2%, have typically done so over extended periods, underpinned by strong institutional credibility, disciplined fiscal frameworks, deep financial markets, and stable macroeconomic conditions. These economies did not simply adopt a lower target: they grew into it through sustained improvements in policy frameworks and structural resilience.

For emerging market economies, the experience is even more instructive. Such economies tend to operate with higher inflation targets precisely because they face structural constraints, such as higher exposure to external shocks, larger weights of food and energy in consumption baskets, and more volatile capital flows, that make inflation inherently less stable. In these contexts, attempts to reduce inflation too quickly or to adopt overly ambitious targets have often resulted in significant output losses, macroeconomic instability, or even policy reversals, as the central banks are forced to recalibrate in the face of persistent target misses or excessive economic costs.

The overarching lesson is clear: sustainable disinflation requires more than a numerical adjustment to the target. It requires time to anchor expectations, credibility built through consistent policy delivery, and structural alignment that reduces the economy’s exposure to volatility, particularly through stronger fiscal discipline, lower pass-through, and improved monetary transmission. Without these foundations, lowering the target prematurely risks undermining both economic stability and the credibility of the policy framework itself.

Conclusion: Timing matters more than the target

The debate over Sri Lanka’s inflation target is ultimately one of timing and economic readiness rather than theoretical desirability. While the long-term benefits of lower inflation are well recognised, the near-term costs of enforcing a 2% target in the current context are significant. Sri Lanka remains a shock-prone, externally exposed, and structurally evolving economy, where inflation is driven largely by exchange rate movements, global prices, and supply conditions. A premature shift to a very low target would likely require tighter monetary conditions, with adverse implications for growth, employment, credit expansion, and debt dynamics, while also placing additional strain on the financial sector and reducing policy flexibility.

Taken together, these trade-offs suggest that the near-term gains from moving to 2% are limited relative to the risks. A more prudent approach would be to consolidate stability under the existing framework, strengthen macroeconomic buffers, and improve policy transmission before considering a gradual transition. Ultimately, the effectiveness of inflation targeting depends less on how low the target is set than on how consistently it can be achieved.

(Note: This article has benefitted from a range of sources; however, for brevity, not all references have been explicitly cited.)

(The author currently serves as an Assistant Governor of the Central Bank of Sri Lanka (CBSL). The views expressed in this article are his own and do not necessarily reflect those of the CBSL. The author may be contacted at [email protected] for further information.)