Thursday Jul 16, 2026

Thursday Jul 16, 2026

Monday, 25 May 2026 03:42 - - {{hitsCtrl.values.hits}}

Leading up to the Asian Financial crisis, the Thai Central Bank sold dollars from its international reserves to keep the baht-to-dollar rate at 25 baht. This came to a culmination in 1997 when it lost $ 25 billion in its abortive attempt to protect the baht. After the Bank of Thailand had lost all its dollars and could no longer support the baht, it had to allow the currency to go into free fall in the market. Its Governor was later tried in court for the losses caused through his excessive use of international reserves to protect the baht

Leading up to the Asian Financial crisis, the Thai Central Bank sold dollars from its international reserves to keep the baht-to-dollar rate at 25 baht. This came to a culmination in 1997 when it lost $ 25 billion in its abortive attempt to protect the baht. After the Bank of Thailand had lost all its dollars and could no longer support the baht, it had to allow the currency to go into free fall in the market. Its Governor was later tried in court for the losses caused through his excessive use of international reserves to protect the baht

Free fall of rupee in international transactions

Free fall of rupee in international transactions

The Sri Lankan rupee against the US dollar, the currency to which the rupee has been pegged, is falling and, given the global and local circumstances, it has been unavoidable.

As at the end of business on 22 May 2026, the Central Bank’s indicative rates for telegraphic transfers, or TTs, stood at Rs. 343 for the buying of dollars and Rs. 353 for the selling of dollars, with a mid-rate of Rs. 348 as the official exchange rate. This rate is applicable to the previous day, calculated by taking the average weighted by both volume and rate, and applies only to telegraphic transfers.

If a retail customer wants to buy or sell dollars over the counter, he should pay more for purchases, at about a premium of Rs. 2, and receive less for sales, at about a discount of Rs. 2, over the announced TT rate. As it is a weighted average, the TT rate offered by individual banks may vary from this announced rate.

Since it is the middle rate between the buying and selling of dollars that is used as the official rate, the current levels indicate a year-to-date (YTD) depreciation of the rupee of about 12%. Indicating the shortage of dollars, it is reported that they are available in the curb market at a premium of Rs. 4-6 for small amounts.

IMF’s stern warning for a flexible exchange rate

Sri Lanka has been under an IMF-supported balance of payments financing facility called the Extended Fund Facility, or EFF, since March 2023. Under the loan covenants applicable to the EFF, as highlighted by the IMF every time a progress review mission visits the country, Sri Lanka should ensure “greater exchange rate flexibility and gradual phasing out of administratively imposed import restrictions” for rebuilding external buffers and economic resilience’ [1].

This stern counsel from the IMF means that Sri Lanka cannot have its own exchange rate. It should buy dollars from the market when there is pressure for the rate to appreciate due to short-term surpluses, while any sale to avoid depreciation is contingent on achieving the targeted foreign reserve positions.

It should also remove, as soon as possible, all the import restrictions that were imposed to support the rupee before it entered into the EFF with the IMF. Economic resilience, as advocated by the IMF, means that the exchange rate should neither encourage imports nor discourage exports excessively when understood in the context of the external sector.

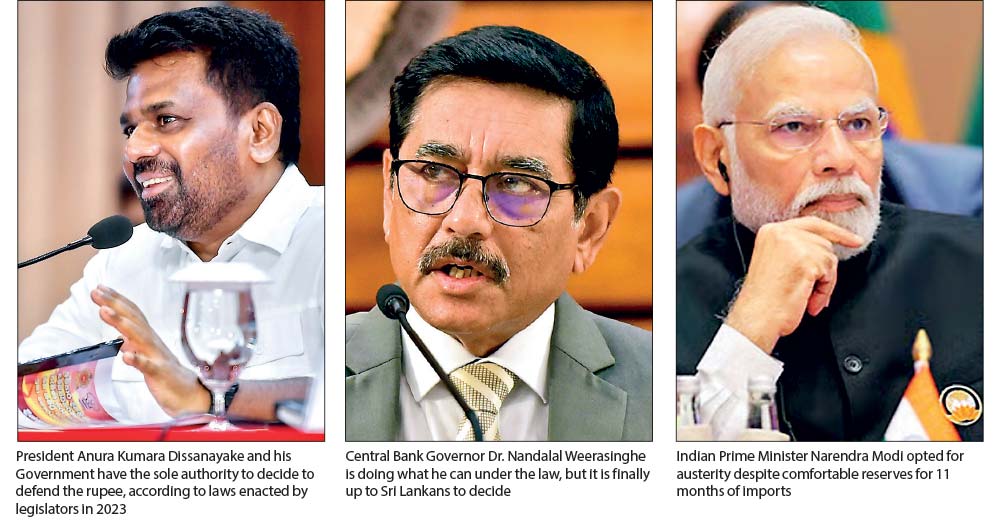

The Indian rupee has so far depreciated by about 8% year-to-date, and India has a comfortable foreign exchange reserve of about $ 696 billion, which is sufficient to finance about 11 months of future imports. Despite this advantageous position, India is pursuing a massive austerity program. It is timely for the Sri Lankan Government to follow suit as well

New Central Bank Act mandates domestic price stability

Maintaining exchange rate stability is not a function of the Central Bank under the new Central Bank Act (CBA) enacted in 2023. In terms of Section 6(1) of the CBA, the primary object of the Central Bank shall be to attain and maintain “domestic price stability”. Domestic price stability means keeping the inflation rate at the level agreed with the Minister of Finance under the bank’s new inflation-targeting monetary policy framework.

The agreed rate with the Minister of Finance in October 2023 was 5% for the headline inflation rate measured by the Colombo Consumers’ Price Index, with a leeway of two percentage points in either direction. Thus, the maintenance of external price stability, meaning a stable exchange rate, is an indirect offshoot of the bank’s primary object.

ER stability, an offshoot of domestic price stability

If the inflation rate is kept at the target level, which the Central Bank and the Finance Minister have fixed at 5% because that is the inflation rate considered to be neutral for economic growth, employment, and savings and investment decisions, the exchange rate is automatically stabilised, avoiding either appreciation or depreciation.

As I explained in my previous article in this series, under John Exter’s Monetary Law Act (MLA), one of the objectives of the Central Bank was to maintain a stable external value of the rupee [2].Under an amendment made to the MLA in 2002, spearheaded by Governor A.S. Jayawardena, and hence termed ASJ’s MLA, this explicit goal was removed but indirectly included in the objective function of the Bank by calling it “attaining economic and price stability”.

As I have explained elsewhere, economic and price stability meant attaining broad macroeconomic stability covering the external, fiscal, and monetary sectors, in which the Central Bank should set the aggregate demand, which is under its control, equal to the aggregate supply, which is outside its control [3].

If a gap persists between these two macroeconomic variables, in terms of the “economic” part of price stability, the Central Bank should continue with its monetary policy actions until the gap is fully eliminated. However, according to the new CBA, which has omitted the stabilisation of the external value of the rupee as an objective of the bank, direct intervention to preserve the exchange rate is not the Central Bank’s job. It therefore follows that the Government should do so in collaboration with the Central Bank.

CBSL does not have tools to intervene in the market, except moral suasion through polite but firm dialogue with banks, to prevent a fall in the external value of the rupee. Therefore, any action that should be taken must come from the Government

CBSL’s job: report to Finance Minister with recommendations

This is a serious policy vacuum in Sri Lanka.

In terms of Section 40(1) of the CBA, the Central Bank shall “manage the official international reserves consistent with international best practices and the rules made by the Governing Board, having regard to safety, liquidity and return, in that order of priority”.

According to the CBA, there is no provision for the Central Bank to use the country’s official reserves to protect the rupee if it comes under pressure to depreciate. What it can do in this regard has been highlighted in subsection (3) of Section 40.

It states that “in the event the Central Bank is satisfied that there is a decline or a likelihood of decline in the international reserves, or such reserves may reach a level that could jeopardise the objects of the Central Bank, and that the Central Bank is unable to remedy such decline by its own measures, the Central Bank shall report to the Minister (of Finance) in writing of such decline, including the reasons for and recommendations to remedy such decline”.

In terms of this provision, the Central Bank has no freedom to conduct its own exchange rate policy in the same way it enjoys freedom in conducting monetary policy. All it can do is bring the reasons for the fall of the rupee to the notice of the Minister of Finance and make recommendations for the Minister and the Government to adopt.

In this scenario, the Central Bank does not have tools to intervene in the market, except moral suasion through polite but firm dialogue with banks, to prevent a fall in the external value of the rupee.

Therefore, any action that should be taken must come from the Government, since it is the Government that can decide whether to use the foreign exchange reserves to appease the high demand for dollars in the market. This is the exchange rate management framework that the country’s legislators intended when they approved the new CBA in September 2023. Hence, they cannot blame the Central Bank for the current unmanageable state of the foreign exchange market.

Speculators, had bet against the short-sighted policy of the Bank of Thailand. Since Thailand had a recurring balance of payments gap year after year, it was logical for speculators to assume that the Bank of Thailand would not be able to continue defending the baht for long. Thus, speculators borrowed heavily in baht and converted the same into dollars using the country’s open capital account

CBSL fettered from all sides

Thus, in exchange rate management, the Central Bank is restrained by two forces.

On one side, there is IMF advice, which compels Sri Lanka to adopt a flexible exchange rate policy, having regard to the need for building external reserve buffers and economic resilience.

On the other, the Bank is toothless since it cannot use the official international reserves on its own to protect the rupee. Any action in that regard should come from the Government after the Bank has made the appropriate recommendations to it.

It also cannot manage the widening trade gap by imposing restrictions on non-essential imports, as many in the country argue, since the advice from the IMF asks it to remove those restrictions imposed prior to obtaining the EFF as soon as possible.

It can increase tariffs, but the increase in import costs through tariff hikes will not reduce the import bill immediately. Quantitative restrictions are more effective in this case since they serve as a shock treatment. However, to introduce quantitative restrictions, Sri Lanka is required to renegotiate the EFF loan covenants with the IMF. Therefore, Sri Lanka today is in a classic Catch-22 situation. Whatever it does will lead to a no-win situation.

It is the Government that can decide whether to use the foreign exchange reserves to appease the high demand for dollars in the market. This is the exchange rate management framework that the country’s legislators intended when they approved the new CBA in September 2023

The Bank of Thailand case

Given the frustrating experience of Bank of Thailand Governor Rerngchai Marakanond in handling the baht-to-US dollar exchange rate prior to the East Asian Financial Crisis of 1997-98, it is unlikely that Central Bank officials would act in violation of the CBA in protecting the rupee today.

The Central Bank is simply an agent responsible for maintaining the country’s official international reserves, and the agent should act according to the instructions of the principal, the Government of Sri Lanka. The case of the Bank of Thailand is illustrative in this scenario, as I have explained elsewhere [4].

Thailand’s insane attempt to protect the Baht

In this case, the Bank of Thailand had maintained the value of the Baht at 25 Baht to the US dollar for a significant period prior to the East Asian Financial Crisis, despite rising inflation within the country requiring it to allow the Baht to depreciate against the dollar.

To keep the baht-to-dollar rate at 25 Baht, it had sold dollars from its international reserves. This came to a culmination in 1997 when it lost $ 25 billion in its abortive attempt to protect the Baht.

However, speculators, chiefly the US-based entrepreneur George Soros, had speculated against this short-sighted policy of the Bank of Thailand. Since Thailand had a recurring balance of payments gap year after year, it was logical for speculators to assume that the Bank of Thailand would not be able to continue defending the baht for long. Thus, speculators borrowed heavily in baht and converted the same into dollars using the country’s open capital account.

After the Bank of Thailand had lost all its dollars and could no longer support the baht, it had to allow the currency to go into free fall in the market. Since all East Asian economies had been connected to each other through trade and investment, a phenomenon known in economics as the contagion effect, the collapse of the Thai economy and its currency triggered the onset of the East Asian Financial Crisis, which spread across all countries in the region during 1997-98.

When the Thai Baht fell to a level of 50 Baht to the dollar, speculators converted part of their dollar holdings into baht and repaid all their debt while keeping the balance as profit. It was reported that they were immensely enriched through this strategic action.

The Central Bank has done what it can under the existing laws. It is toothless in handling this extraordinary situation. Hence, instead of blaming the Central Bank, all Sri Lankans should come together today to face the challenges posed by the Middle East war as a united force

Making BOT Governor guilty

After the fall of the Thai baht and the consequential collapse of the Thai economy, a high-level investigative committee was appointed by the Thai Government to identify the people responsible for the destruction of the Thai economy.

The report was released in 2000, and it identified key officials of the Bank of Thailand who could be subject to criminal prosecution. One such official identified was Bank of Thailand Governor Rerngchai Marakanond. Subsequently, Rerngchai was tried in court for the losses caused to the Bank of Thailand through his excessive use of international reserves to protect the Baht.

He was found guilty and fined Baht 186 billion, equivalent to $ 4.6 billion, in 2005 for his leading role in the country’s financial crisis. Later, on appeal, this order was reversed in 2011 but, as he confessed, his mental and emotional wellbeing had been completely shattered because of the severe criticism and charges levelled against him.

Thus, it is necessary for the Central Bank to obtain the approval of the Government if it wants to use the international reserves to protect the external value of the rupee.

India’s smart move: Austerity despite comfortable reserve levels

This is a national crisis, and all citizens should unite to face the challenges as a single force. In this connection, the appeal made by Indian Prime Minister Narendra Modi to all Indians, both citizens and businesses [5], to adopt an austerity program is a useful guide for Sri Lanka.

He urged Indian citizens to conserve fuel, cut down on foreign currency-draining activities, and avoid non-essential gold purchases in view of the Middle East war and its disastrous impact on the global economy. He also asked businesses to revive work-from-home arrangements, reduce foreign travel, and prioritise the use of local products, which he termed under the slogan “Vocal for Local”.

The Indian rupee has so far depreciated by about 8% YTD, and India has a comfortable foreign exchange reserve of about $ 696 billion, which is sufficient to finance about 11 months of future imports. Despite this advantageous position, India is pursuing a massive austerity program. It is timely for the Sri Lankan Government to follow suit as well.

Blaming CBSL unwarranted

The Central Bank has done what it can under the existing laws. It is toothless in handling this extraordinary situation. Hence, instead of blaming the Central Bank, all Sri Lankans should come together today to face the challenges posed by the Middle East war as a united force.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected] )

Endnotes

(Endnotes)

1 See the IMF Executive Board recommendation to Sri Lanka while approving the Fourth instalment under EFF in July 2025: https://www.imf.org/en/news/articles/2025/07/02/pr24235-sri-lanka-imf-executive-board-completes-the-fourth-review-under-the-eff

2 https://www.ft.lk/columns/Revisiting-Central-Bank-s-growth-role-With-its-nominal-policy-powers-it-cannot-promote-growth-even-if-it-wants-to-do-so/4-792043

3 Wijewardena, W.A. 2017, Central Banking: challenges and Prospects, BMS Publications, Colombo, Chapter 17, pp 193-204.

4 Ibid, pp 191-2.

5 See: https://www.instagram.com/p/DYLl28vkwRJ/