Thursday Jul 30, 2026

Thursday Jul 30, 2026

Friday, 1 October 2021 00:00 - - {{hitsCtrl.values.hits}}

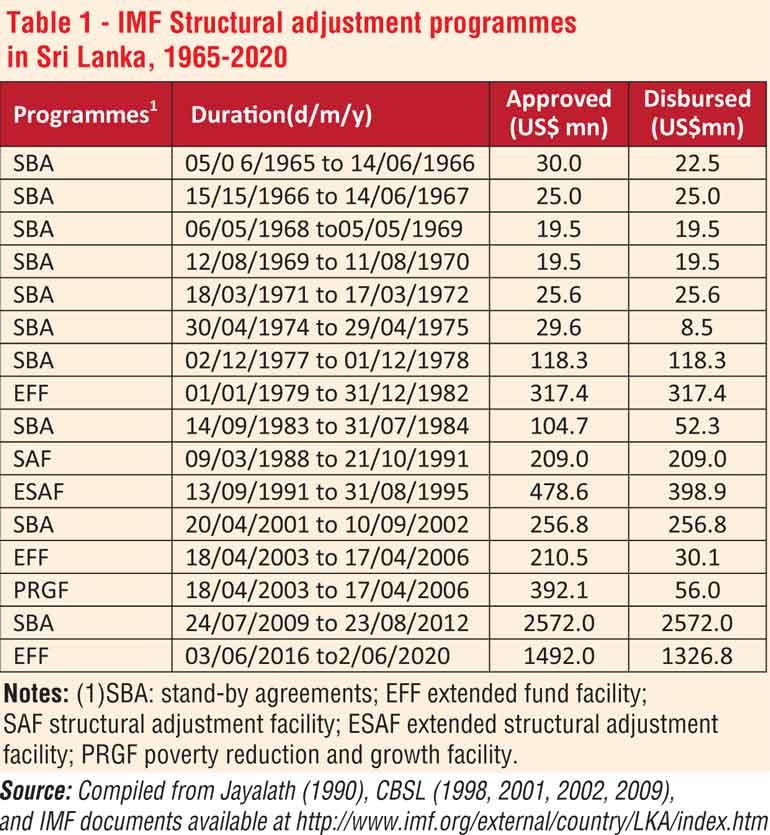

Since 1965 Sri Lanka has been a ‘repetitive client’ of the IMF. The country has entered into 16 economic stabilisation programmes during 1965-2000. Macroeconomic management of the country has been under IMF programmes for approximately 33 years of the 55-year period

1970-’75: Trotskyite Finance Minister seeking IMF support again

The United Front coalition (UF) came into power in 1970 promising to ‘to lay the foundation for an irrevocable transition to the economy to a socialist one’ (Perera 1970a, p. 4-5). The development strategy of the new Government envisaged combining ‘outward looking development ... with the right mixture of internal policies and approaches to domestic resource mobilisation which prove to be socially acceptable’ (Perera 1970b, p. 176)

Government envisaged combining ‘outward looking development ... with the right mixture of internal policies and approaches to domestic resource mobilisation which prove to be socially acceptable’ (Perera 1970b, p. 176)

By 1970, Sri Lanka’s repayment obligations to the IMF had become an important factor that contributed to high level of capital amortisation because of repetitive recourse to borrowing in the second half of the 1960s (Central Bank Annual Report 1971, p. 194). NM, the Finance Minister, started negotiation for a fifth SBA with IMF within months of the new Government coming into power. In his 1970 Budget Speech he argued that “we cannot brush aside and completely ignore these international institutions; we can repudiate their terms only if we are prepared to face the far-reaching distortions” (Perera 1970).

The initial discussions were held in June 1970 in Colombo with D.S. Savkar, Assistant Director, West Asia Division of the IMF. NM attended and addressed the IMF-World Bank annual conference in Copenhagen in September 1970 and persuaded the IMF Managing Directors Paul Schweitzer to visit Colombo on 20 October 1970. Final discussion were held in Washington DC in December 1970. In the negotiations, NM was assisted by a strong team of technocrats including W. Tennekoon (Central Bank Governor), M. Rajendra (Secretary to the Treasury) and H.A. de S. Gunasekera (Permanent Secretary, Ministry of Planning and Employment).

The IMF was firmly of the view that the imbalance of payments can only be set right by a further devaluation of the Rupee. The Finance Minister opposed to the idea because of the perceived inflationary impact it would have and managed to convince the IMF team that the Government had the capacity to reduce the budget deficit by taking firm actions to reduce the budget deficit, promoting domestic saving, relaxing credit controls, encouraging exports and pursuing a vigorous programme of import substitution. The IMF approved a SBA of $ 25.6 million on 17 May 1971. To facilitate the implementation of the SBA, the IMF enlisted assistance of the World Bank and some downer countries for an aid programme.

After signing the SBA, NM emphatically defended his decision to go to the IMF in the Parliament: ‘effort to put its own house in order was not the result of IMF advice but was the obvious thing to do in the national interest’ (Hansard, Vol 91, November 10, 1971, cc 2621-2633).

The worsening balance of payment situation in the wake of the oil price increase in 1973 compelled the Government to negotiate another SBA. In preparation for negotiations the Government came up with some ‘sweeteners’ for the IMF: the rupee was re-linked to the pound sterling from the US$ when the pound was floated on 23 June 1972 resulting in an indirect devaluation of the rupee by about 7%.; in November 1972 the FEECs rate was increased from 45% to 65% with an expansion of the import coverage of FEEC scheme to nearly 75%, and the food subsidy bill was cut substantially on its own initiative. The negotiations took two years and a personal visit by the Finance Minister to the IMF before signing the agreement to the tune of $ 29.6 m on 30 April 1974.

‘sweeteners’ for the IMF: the rupee was re-linked to the pound sterling from the US$ when the pound was floated on 23 June 1972 resulting in an indirect devaluation of the rupee by about 7%.; in November 1972 the FEECs rate was increased from 45% to 65% with an expansion of the import coverage of FEEC scheme to nearly 75%, and the food subsidy bill was cut substantially on its own initiative. The negotiations took two years and a personal visit by the Finance Minister to the IMF before signing the agreement to the tune of $ 29.6 m on 30 April 1974.

Sri Lanka obtained only the first instalment ($ 8.5 m) under this SBA. The IMF withheld the balance because the Government failed to adhere to the ceiling imposed on domestic credit. Perhaps the Government was not under pressure to stick to IMF conditionality in that year because of the availability of ‘easy’ IMF finance under the newly-introduced Oil Facility (SDR 34 million) and the Compensatory Finance Facility (SDR 7.0).

The Government approached the IMF for another SBA in 1975. However, the discussions floundered allegedly on account of the Government’s reluctance to cut further subsidies as required by the IMF (Kappagoda and Paine 1981, p74).

The UF Government made considerable progress towards macroeconomic adjustment with the help of the IMF programmes. Both the annual debt servicing burden and the term structure of external debt significantly improved. However, as Kappagoda and Paine (1981) have convincingly argued, ‘the payment adjustment [cut in domestic absorption] proceeded faster than was warranted’ (p. 100).

The adjustment burden primarily felt on imports with serious adverse effects on the economy’s medium term prospects and consumer wellbeing. The groundswell of unhappiness of the electorate paved the way for the UNP to return to power with a landslide majority in June 1977.

1977-’88: The first wave of liberalisation reforms

The widely-held view in the Sri Lankan policy circles is that the regime shift opened up the opportunity for the IMF to dictate ‘neo-liberal’ reform in Sri Lanka (Gunasinghe 1986, Lakshman 1985, Davis 2015). Lakshman (1985, p. 22), in particular, claims that ‘the determining hand of the IMF-WB group in shaping and implementing of the ‘open economy’ is abundantly clear’. This claim could not be further from reality.

Major reforms such as trade liberalisation and exchange rate depreciation and the opening up of the economy to foreign direct investment were, in fact, undertaken by the new Government in the ‘honeymoon’ period following the massive election victory, based on the recommendations of the Shenoy report. When the Government adopted pro-market policies for its own reasons, the IMF became an important partner of development policy, but, of course, subject to its standard conditionality.

As already noted, the balance of payments position was in relatively better shape at the time compared to the first half of the decade. There was also promising sign of massive concessionary capital inflows from the major donor nations in support of the economic opening by the new Government. Immediately after the new Government was formed, the Finance Minister, Ronnie de Mel made a one-month visit to a number of Western countries to seek aid and returned with promising pledges. In 1978, aid disbursements alone were sufficient to cover the current account deficit (Central Bank Annual Report 1978). There was no urgent need for approaching the IMF for balance of payments support alone. It seems that the Government choose to go to the IMF to gain credibility to the reform process.

The Government presented a proposal for a $ 427 m under a SBA. However, in the absence of a well-prepared medium-term stabilisation programme, and because the Government’s disagreement with the IMF to phase out subsidies, the IMF approved a SBA of only $ 122 plus $ 50.3 million as a supplement from the IMF Trust Fund in 1978. Immediately after approving the SBA, the IMF opened a representative office in Colombo to work closely with the Government in monitoring the reforms. In January 1979, the IMF approved $ 317.2 m EFF programme to support structural adjustment reforms during the three-year period of 1979-’81.

The relationship between the Government and the IMF, however, began to come under strain from 1981 because of a significant disagreement relating to the policy priorities of the Government (Rajapatirana 2017). The Government swiftly implemented the Shenoy recommendations for economic opening, but it overlooked Shenoy’s recommendations for macroeconomic stabilisation, which was an integral part of the proposed overall reform package. It decided to accelerate the implementation of the Mahaweli Development Project (collapsing the original implementation period of 30 years to eight years), side by side with the liberalisation reforms.

The IMF (and the World Bank) became concerned about the inconsistency between the objective of structural adjustment in the economy under liberalisation reforms and the inevitable macroeconomic instability resulting from the massive investment programme (Levy 1998, Athukorala and Jayasuriya 1991).

Apart from the macroeconomic instability, there were also genuine concerns regarding the viability of the $ 664 m project: A study of the project financed by the World Bank in 1981 recommended a slower rate of implementation than what the Government envisaged to avoid possible cost blow-up. The study also expressed concern that donors had made aid commitments for the project without properly evaluating the project’s costs.

In September 1983, the IMF approved another SBA of $ 105 m (as opposed to the Government’s request for $ 221 m). However, the IMF terminated the agreement after only half of the agreed amount was disbursed, over concerns about macroeconomic instability caused by the massive Mahaweli investment programme. The World Bank also withheld disbursement of allocations under a Structural Adjustment Loan (SAL) ($ 70 m) because of the Government’s dispute with the IMF. According to a confidential letter to the Ministry of Finance and Planning (leaked to Lanka Guardian), David Hopper, the Vice President of the South Asia Programme, emphatically stated that ‘the precondition for all Bank structural adjustment activities is an agreement with the IMF’ (Jayalath 1990).

Ronnie de Mel, the Finance Minister, described the nature of the Sri Lanka-IMF relationship during this period as follows: ‘We have had discussions, intricate discussions, debates, long negotiations and many quarrels. We have had suspensions. We have had estrangements. It has been, in short, love-hate type relationship. It has been something like the relationship between Elizabeth Taylor and Richard Burton’ (Hansard, Vol. 22, No. 12, March 18, 1983, C 1768).

1988-2005: The second-wave reforms

The economic boom following the 1977 reforms mainly concentrated in the first three years (1978-81) when the economy grew at an average annual rate of 6.6%. In the ensuing years of the decade, liberalisation reforms were overtaken by the commitment to major infrastructure projects. The process of structural adjustment in the economy was hampered by the failure to complete implementation of the reform agenda, in particular labour market reforms and State enterprise reforms, and the adverse impact of the investment boom on tradable goods production in the economy because of the appreciation of the real exchange rate (Moore 1990, Dunham and Kelegama 1997).

Added to this was the economic disruption caused by the escalation of the separatist war from 1983 and JVP uprising in the south during 1987-’89. By the end of the 1980s, the Sri Lankan economy had come close to a foreign exchange crisis, with low foreign exchange reserves, massive security related Government expenses, and a misaligned exchange rate that propelled significant capital flight and under repatriation of export proceeds (IMF 2001).

In this volatile economic climate, the UNP Government under the new leadership of President Premadasa embarked on the ‘second wave’ liberalisation reforms (Dunham and Kelegama 1995). The IMF supported the reforms under a Structural Adjustment Facility (SAF) of $ 209 m) and an Extended Structural Adjustment Facility (ESAF) of $ 478.6 m. Reforms included devaluation of the rupee against the US$ by 34% between mid-1989 and the end of 1993, further liberalisation of financial and commodity markets, revamping of the operations of the Board of Investment (BOI) with a one-stop-shop for investment approval process, privatisation of some State-Owned Enterprises (under an innovative politically-friendly label, ‘peopalisation’) and a poverty alleviation programme.

Dunham and Kelegama (1995, p. 187) have characterised the second-wave reforms as an illustration of how ‘strong leadership proved critical in ... reforms, in a country where the state is not strong, and is neither cohesive nor disciplined, in organisational rearms’.

The vigour of second-wave reforms was lost because of the tragic death of the President, but there was no back sliding from reform because economic outcomes had been impressive enough to make economic liberalisation by-partition policy (Kumaranatunge 2004).

The new SLFP-led Coalition Government continued with trade liberalisation and privatisation of State enterprises. During 2001-2002 the Government received financial support for reforms under a SBA of $ 256.8 m. In releasing funds under the SBA the IMF was sympathetic to the difficulties faced by the Government in meeting conditionality because of the exigencies of the accelerating civil war.

For instance, the IMF showed flexibility to extend the agreement to 19 September 2002 on a lapse-of-time basis to allow the completion of the final review and granted a waiver for the non-compliance of performance criteria and released the agreed amount, because non-compliance was largely due to factors beyond the control of the Sri Lankan authorities (escalating ethnic conflict and oil price hike).

1995-2009: The period of escalating civil war

During the period from collapse of peace talks between the LTTE and Government in 1995 until 2009, the reform process was hampered by the escalating civil war. In 2003, the IMF approved a three-year PRGF to the amount of $ 392.7 m and an additional EFF in tune of $ 210.8 m over the period 2003-’06. Both programmes lapsed after the withdrawal of the first instalments.

The post-civil war era

The post-civil war era

Following the ending of the civil war in July 2009, the IMF approved the largest ever programme loan (SBA of $ 2.6 b) for Sri Lanka. The quarterly performance criteria (QPCs) related to the standard macroeconomic stabilisation measures.

The Government’s poor record of revenue mobilisation, in particular continued decline in the tax revenue-to-GDP ratio, and the budgetary burden of supporting loss-making public enterprises, and the backsliding on trade liberalisation came up in the negotiations but did not become part of the conditionality. This was presumably because the IMF wanted to provide the Government with policy autonomy in restoring the economy after the three-decade civil war.

In June 2016 the Government entered into a three-year EFF ($ 1.5 b) with the IMF. The EFF aimed to harness an additional $ 650 m in other multilateral and bilateral loans of about $ 2.2 b (over and above the existing financing arrangements). The stated objective of the programme was to help the new Government restore macroeconomic stability and resilience of the economy to facilitate sustainable and equitable economic growth (IMF 2016).

The programme focussed on reforms to tax policy and tax administration with a focus on increasing direct tax collection, fiscal policy management, and State enterprise reforms to achieve fiscal consolidation while providing fiscal space for the Government’s key social and development spending programmes. Fiscal consideration reforms were to combine with flexible monetary targeting under a flexible exchange rate regime, reforms in the trade and investment regime, and rebuilding foreign exchange reserves.

The reforms undertaken by the Government under the programme during 2016-’19 included a major revision to the value added and income tax systems and introducing a new building tax and rationalising the customs duty structure (Coomaraswami 2017). On 13 May 2019 the IMF Executive Board approved an extension of the EFF until June 2020 with rephrasing of remaining disbursements to complete the reform agenda. However, the implementation of the programme abruptly ended with the change of government in early 2020.

To sum up, since 1965 Sri Lanka has been a ‘repetitive client’ of the IMF. The country has entered into 16 economic stabilisation programmes during 1965-2000. Macroeconomic management of the country has been under IMF programmes for approximately 33 years of the 55-year period. The IMF fully disturbed agreed funds under 12 (approximately covering 25 years) of these 17 agreements. The conditionality attached to the agreements has notably varied over time depending on shifts in the development thinking of the IMF and macroeconomic conditions and the underlying political developments of the country.

(To be continued tomorrow)

(The writer is a Fellow of the Academy of the Social Sciences of Australia, and Emeritus Professor of Economics at the Arndt-Corden Department of Economics, Crawford School of Public Policy, Australian National University and can be reached via [email protected])

[In writing the analytical native of Sri Lanka-IMF relations during 1960-1985, the author has drawn heavily on the PhD thesis of J.B.A.D Jayalath, ‘The Political Economy of Adjustment and Stabilization: Sri Lanka’s Relations with the International Monetary Fund and the World Bank, 1960-1985’ (The University of New England, Australia, 1990). He has also benefited from discussions with Sisira Jayasuriya. The full paper will be available soon at https://acde.crawford.anu.edu.au/acde-research/working-papers-trade-and-

development.]