Thursday Jun 25, 2026

Thursday Jun 25, 2026

Thursday, 25 June 2026 00:48 - - {{hitsCtrl.values.hits}}

The CBSL’s monitoring and regulation on the captioned matter is twofold. i.e firstly the export proceeds repatriation into Sri Lanka and secondly the conversion of foreign currency proceeds to LKR, as part of the effort to build adequate foreign currency reserves, through means that does not impose debt obligations on the country and which will support the functioning of the economy during uncertain times. On the other hand, the Inland Revenue Department (IRD) considers only the former, i,e. the repatriation of export proceeds into Sri Lanka for the purposes of direct and indirect tax concessions

The CBSL’s monitoring and regulation on the captioned matter is twofold. i.e firstly the export proceeds repatriation into Sri Lanka and secondly the conversion of foreign currency proceeds to LKR, as part of the effort to build adequate foreign currency reserves, through means that does not impose debt obligations on the country and which will support the functioning of the economy during uncertain times. On the other hand, the Inland Revenue Department (IRD) considers only the former, i,e. the repatriation of export proceeds into Sri Lanka for the purposes of direct and indirect tax concessions

The policies on repatriation of export proceeds into Sri Lanka are in place as one of the Central Bank of Sri Lanka’s (CBSL) measures to ensure adequate foreign currency inflow to build the foreign currency reserve position of the country.

The policies on repatriation of export proceeds into Sri Lanka are in place as one of the Central Bank of Sri Lanka’s (CBSL) measures to ensure adequate foreign currency inflow to build the foreign currency reserve position of the country.

The foreign currency reserves play an important role in building CBSL’s international reserves. International reserves provide a shield during times of economic instability through supporting currency stabilisation, country’s foreign debt repayment obligations and ensuring trade and import stability.

The further requirement for the mandatory conversion of the export proceeds into Sri Lankan Rupees (LKR) post the repatriation, is with the aim of maintaining the foreign currency liquidity in the domestic foreign exchange market.

Evolvement of the relevant foreign regulations in Sri Lanka

The regulations on repatriation of export proceeds were introduced under the repealed Exchange Control Act No. 24 of 1953 (ECA) in 1973. However, it was discontinued after Sri Lanka accepted Article VIII under the Articles of Agreement of the International Monetary Fund (IMF) in 1994, which placed a focus on liberalisation of current payments.

This permitted exporters to repatriate export proceeds into Sri Lanka and retain such proceeds in local or foreign currency accounts in Sri Lanka or retain them in foreign currency accounts in a bank abroad, until the regulations were re-introduced in 2016 under the ECA.

Since then, these regulations have been amended from time to time post the enactment of the Foreign Exchange Act No.12 of 2017 (FEA) which replaced the ECA, having regard to the foreign exchange policies of the CBSL.

Initially the mandatory timeline requirement for repatriation of export proceeds applied only to an exporter of goods. This requirement was extended to exporters of services as well under Extraordinary Gazette No. 2251/42 dated 28 October 2021. The repatriation timeline was within 180 days from the date of shipment or provisioning of services.

The mandatory conversion requirement of the export proceeds has also evolved over time. Though Extraordinary Gazette No.2215/39 dated 18 February 2021 mandated the immediate conversion of 25% of export proceeds on receipt, subsequent regulations amended the conversion percentage (to 10% and back to 25%) and timeline for such conversion (from 14 days to 30 days).

However, under Extraordinary gazette No. 2251/42 dated 28 October 2021 (supra), the exporters of goods and services were granted an extended timeline being on or before the seventh day of the following month of receipt, for conversion of the residual export proceeds after deduction of authorised payments. Nevertheless, there was a condition that this conversion timeframe also should not exceed the 180 day timeline from the date of shipment or provisioning of services.

Subsequently, the mandatory conversion requirement of the foreign currency to LKR was removed for service exporters under Extraordinary Gazette No. 2292/50 dated 12 August 2022.

For exporters of goods, the mandatory conversion timeline of residual export proceeds were liberalised under Extraordinary Gazette No. 2391/02 dated 01 July 2024 (subsequently amended), effective from 04 September 2024, where conversion was required on or before the tenth day following 03 calendar months from the month of receipt.

However, given the negative repercussions of the present global economic conditions on Sri Lanka’s economy and the need to ensure adequate foreign currency reserves, this liberalised timeline has been curtailed drastically under Extraordinary Gazette No. 2492/10 dated 09 June 2026. Now exporters of goods are required to convert the export proceeds after deducting authorised payments, on or before the tenth day of the following month of receipt.

The authorised payments permitted for deduction prior to conversion are:

The 180 day timeline for repatriation of export proceeds into Sri Lanka continues to apply for both exporters of goods and exporters of services, calculated from the date of shipment or provision of services. Where this condition is not satisfied, immediate conversion of the export proceeds on receipt is mandated and the exporters maybe subject to regulatory action.

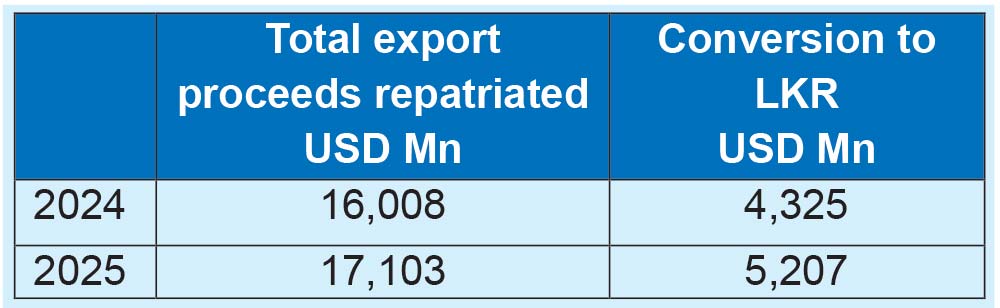

As per the CBSL data, there is an increase in 2025 compared with 2024, in both total export proceeds repatriated to Sri Lanka and the foreign currency conversion to LKR.

Income tax perspective

Income tax perspective

With the enactment of the Inland Revenue Act No.24 of 2017 as amended (IRA) effective from 01 April 2018, a concessionary corporate tax rate was provided to a company “predominantly” conducting a business of exporting goods and services. i.e. where more than 80% of the revenue of the company was from exports.

Subsequently, an amendment was brought under the IRA to afford this concession for income from export of goods irrespective of the proportion of export income to the total income and in the case of export of services, an exemption (for both an individual and a company), requiring the payment be received in foreign currency and remitted through a bank to Sri Lanka, in parallel to the requirement for repatriation of export proceeds under the foreign exchange regulations (FER):

a) Export of Goods – a concessionary rate of 14% during the period from 01 January 2020 to 30 September 2022, where the payment was received in foreign currency and remitted through a bank to Sri Lanka.

b) Export of Service - An exemption during the period from 01 January 2020 to 31 March 2025, where the payment in respect of any service that was provided in or outside Sri Lanka, to any person to be utilised outside Sri Lanka, has been received in foreign currency and remitted through a bank to Sri Lanka.

The concessionary rate for export of goods was removed and the standard corporate income tax rate (of 30%) applied from 01 October 2022.

It is interesting to note that in the case of export of services, the IRA exemption which is conditional upon meeting stipulated criteria was brought in prior to the FER requirement for repatriation of export proceeds from services (which was only introduced in October 2021). Nevertheless, the IRA exemption on export of services was removed, and a 15% rate applied from 01 April 2025, under the same conditions that were applicable for availing the exemption.

Value Added Tax (VAT) perspective

Exporters of goods and services can avail the zero VAT rate under the Value Added Tax Act No.14 of 2002 as amended (VAT Act) on meeting the specified requirements.

An amendment was brought under the VAT Act effective from 13 May 2021, mirroring the 06 month mandatory export repatriation timeline under the FER.

Under this amendment, exporters of goods and exporters of services (detailed below), are required to ensure that the payment for the exports made by them are received in foreign currency, through a bank in Sri Lanka licensed under the Banking Act, No. 30 of 1988, within a period of 06 months, from the end of the taxable period of the export of goods or supply of services. Apart from this, a requirement was introduced to upload schedules (schedule 6 and 7) to RAMIS providing all payment details.

The export of services to which the repatriation timeline applies under the VAT Act includes services directly connected with:

The impact of non-compliance with this timeline did not result in the standard VAT rate application, in the case of exporters who could prove to the satisfaction of the Commissioner General of Inland Revenue that the goods were in fact exported or the services were performed. In this instance, the VAT input of the exporter was considered as disallowed and barred a claim against the zero-rated output VAT.

However, effective from 11 April 2025, the restriction of disallowing the VAT input in such instance was removed as well.

Therefore, at present, the 06-month repatriation timeline does not carry adverse repercussions to an exporter under the VAT Act if it could be proved to the satisfaction of the Commissioner General of Inland Revenue that the goods were in fact exported or the services were performed.

Social Security Contribution Levy (SSCL) perspective

The Social Security Contribution Levy Act No. 25 of 2022 as amended (SSCL Act) which came into effect from 01 October 2022 also aligns with the FER requirement for repatriation of proceeds in respect of export of services where, an exemption can be availed in respect of any service rendered in or outside Sri Lanka, to any person or partnership outside Sri Lanka, for the utilisation out of Sri Lanka and the payment is made in foreign currency and is remitted to Sri Lanka through a bank. A timeframe within which the funds should be remitted is not stipulated as a condition for applying the exemption.

For exporters of goods, the exemption applies on any article exported by the manufacturer, and is not conditional upon the requirement to repatriate the export proceeds to Sri Lanka.

Conclusion

The CBSL’s monitoring and regulation on the captioned matter is twofold. i.e firstly the export proceeds repatriation into Sri Lanka and secondly the conversion of foreign currency proceeds to LKR, as part of the effort to build adequate foreign currency reserves, through means that does not impose debt obligations on the country and which will support the functioning of the economy during uncertain times.

On the other hand, the Inland Revenue Department (IRD) considers only the former, i,e. the repatriation of export proceeds into Sri Lanka for the purposes of direct and indirect tax concessions.

Unlike CBSL, IRD does not receive direct source information as to whether the company or individual received the payment in foreign currency for the export through a bank or within 06 months as the case maybe. However, when an audit is carried out by the IRD, a report issued as per the CBSL guideline by the respective bank where the foreign currency account is handled, is accepted.

Sri Lankan Transfer Pricing guidelines require that goods and services being provided to/received from associated enterprises be compensated in line with the arm’s length principle. Generally, captive service providers invoice the foreign counterparts of the multinational group a service fee which comprises of cost plus profit margin. However, in certain cases, the inward foreign currency remittance is made only to the extent of the captive service provider’s cost excluding profit margin.

Therefore where the export proceeds have been routed to Sri Lanka only in part, it raises concerns on the entitlement of exporters who have claimed or are claiming the tax benefit, of the concessionary rate, VAT input or the exemption, on the premise of routing the entire proceeds.

Non-compliance with the relevant provisions of the IRA, VAT Act or SSCL Act will get flagged to the IRD only in the case of an audit being conducted and it comes within their scrutiny for the purposes of granting the benefit under the relevant tax statute.

The burden of proof will be on the exporter to demonstrate their bona fide compliance through related documentary evidence pertaining to receipt of export proceeds. This would include related invoices, transfer confirmation from foreign customer, relevant bank statements of the exporter etc.

In any event this would not constitute an additional requirement since the foreign exchange regulations require exporters to present documentary evidence on each and every receipt of export proceeds to the respective license commercial bank.

(The author is Senior Manager, Tax and Business Advisory at Deloitte Sri Lanka)

References:

CBSL Annual Report 2022: Chapter 5 - External Sector Developments and Policies

CBSL Financial Statements and Operations 2024

CBSL Financial Statements and Operations 2025

CBSL opinion: International Reserves - A Buffer against the External Shocks (April 2025)

Department of Foreign Exchange – Directions on repatriation of export proceeds