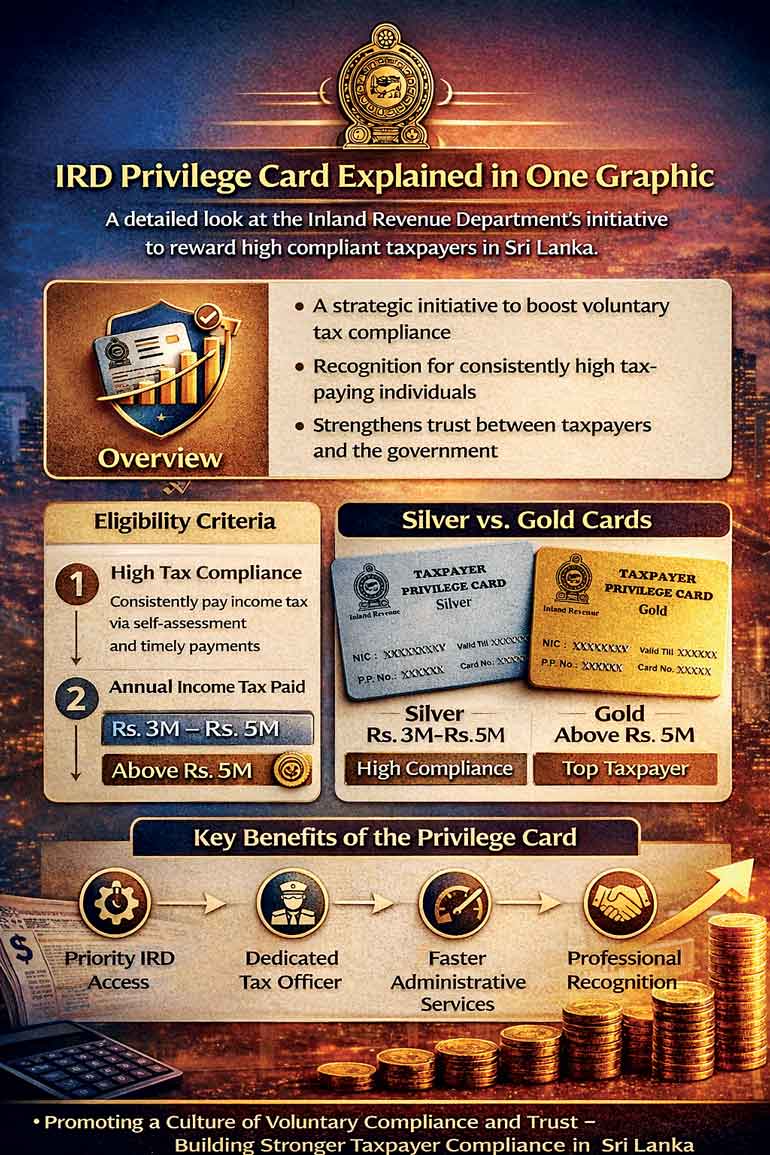

- Recognition for tax compliance: New dimension to the IRD Privilege Card

At a time when Sri Lanka is rebuilding fiscal stability and strengthening its revenue architecture, an important reform has emerged from the Inland Revenue Department (IRD). The newly introduced Privilege Card Scheme for compliant individual taxpayers signals a strategic shift in tax administration philosophy — from enforcement-centric compliance to recognition-based partnership.

This initiative represents more than a ceremonial gesture. It reflects a deliberate behavioural and governance strategy designed to reinforce voluntary compliance, reward fiscal discipline, and institutionalise trust between the State and high-value taxpayers.

For decades, tax compliance in Sri Lanka has been shaped largely by audits, penalties, and statutory enforcement. While these mechanisms remain essential, modern tax systems increasingly recognise that sustainable revenue growth depends on voluntary compliance and positive engagement.

The Privilege Card Scheme operates precisely within this framework. It acknowledges that individuals who consistently meet their tax obligations on time — and in full — contribute not only revenue, but also stability, predictability, and governance credibility to the national economy.

Eligibility under the scheme is grounded firmly in compliance performance in the immediately preceding Year of Assessment. To qualify, an individual must have paid income tax equal to or exceeding the eligible annual self-assessment payments for that year. Timely submission of the Return of Income is mandatory where applicable, and all declared taxes — including self-assessment instalments — must have been settled by their respective due dates.

Importantly, compliance extends beyond direct payments. Taxes deducted at source — including Advanced Income Tax (AIT), Withholding Tax (WHT), and Advanced Personal Income Tax (APIT) — must have been properly remitted within statutory timelines by withholding agents, together with the relevant returns. The scheme therefore emphasises procedural integrity and consistency, not merely quantum of payment.

In structuring the programme, the IRD has introduced a two-tier recognition model. A Silver Card is issued to individuals who have paid between Rs. 3 million and Rs. 5 million in income tax for the prior Year of Assessment. A Gold Card is granted to those whose income tax payments amount to Rs. 5 million or above.

This tiered structure introduces a subtle but powerful element of aspirational compliance. Recognition becomes both symbolic and reputationally valuable, particularly among senior professionals, corporate leaders, and entrepreneurs whose public credibility is closely intertwined with governance standards.

Applications are generally accepted between 15 November of the preceding calendar year and 31 January of the relevant year. For 2026, however, the IRD has extended the deadline until 28 February 2026 due to the extended return filing deadline for Y/A 2024/25. Applications may be submitted via email or delivered to the Revenue Monitoring Unit, and eligible applicants can expect issuance within three weeks, subject to verification.

What distinguishes the scheme is not merely the issuance of a card, but the administrative privileges that accompany it. Cardholders are granted priority access to meet senior IRD management, including the Commissioner General. They receive priority access to respective tax officers and are assigned a nominated officer from each Tax Services Unit. Additional benefits include a vehicle identification sticker, the possibility of tax consultancy services at the cardholder’s premises when necessary, and the presentation of a brooch bearing a special logo.

From a governance perspective, this effectively creates a relationship-managed taxpayer segment — a concept widely adopted in advanced jurisdictions. Institutions such as HM Revenue and Customs in the United Kingdom, the Inland Revenue Authority of Singapore, and the Australian Taxation Office have long implemented differentiated engagement frameworks for high-value compliant taxpayers. Sri Lanka’s move aligns with this global best practice model.

The broader economic implications are noteworthy. High-income individuals often represent a disproportionately significant share of direct tax collections. Ensuring their continued compliance improves revenue predictability, reduces administrative enforcement costs, and lowers the incidence of disputes and litigation. In an IMF-supported fiscal consolidation environment, such stability carries macroeconomic importance.

There is also a corporate governance spillover effect. Many eligible individuals are directors, senior executives, consultants, and business owners. When compliance becomes a recognised standard of professional stature, it reinforces ethical financial behaviour within companies and strengthens internal governance cultures.

That said, the success of the scheme will depend on careful implementation. The IRD must guard against perceptions of preferential treatment or unequal access. Transparency in eligibility verification, consistent service delivery, and integration with digital tax administration reforms will be essential to maintaining credibility. Recognition should never translate into regulatory compromise; rather, it should reward those who have already demonstrated consistent adherence to statutory obligations.

For Sri Lanka’s business community, the message is increasingly clear: tax compliance is no longer merely a defensive necessity. It is increasingly becoming a strategic asset. In an environment where reputational capital, ESG standards, and governance transparency increasingly influence investment flows and stakeholder confidence, formal recognition by the national tax authority carries tangible signalling value.

Ultimately, the Privilege Card Scheme reflects a maturing tax administration philosophy. It acknowledges that sustainable revenue systems are built not only on statutory authority, but also on mutual trust. By elevating compliant taxpayers from passive subjects of regulation to recognised partners in nation-building, the IRD has taken a meaningful step toward modernising Sri Lanka’s fiscal culture.

If consistently executed and expanded thoughtfully, this initiative could evolve into a foundational pillar of Sri Lanka’s long-term revenue governance framework — positioning tax compliance not simply as a legal duty, but as a mark of professional distinction, responsible leadership, and civic trust.

Why high-value taxpayers should embrace IRD Privilege Card

In the evolving landscape of Sri Lanka’s fiscal governance, the Inland Revenue Department (IRD) has introduced a Privilege Card Scheme to recognise compliant individual taxpayers. Yet among many high-income professionals and entrepreneurs who qualify, a practical question has surfaced: “Is it really worth applying?”

This skepticism is understandable. For individuals who already maintain disciplined tax compliance, the card may initially appear symbolic. However, when examined through the lens of governance efficiency, reputational capital, and strategic risk management, the Privilege Card represents far more than ceremonial recognition.

Compliance is no longer just an obligation — it is an asset

High-value taxpayers often contribute disproportionately to national revenue collections. They are corporate directors, consultants, investors, and senior executives whose financial affairs intersect with banks, regulators, investors, and international partners.

In such an environment, structured engagement with the tax authority is not a luxury — it is a governance advantage.

The Privilege Card Scheme provides several practical advantages, including:

- Priority access to senior IRD management

- Priority engagement with respective tax officers

- Assignment of a nominated officer from each Tax Services Unit

- On-premises consultancy support where necessary

For a high-income professional, the true value lies not in the physical card, brooch, or vehicle sticker, but in administrative speed and clarity. Time, in high-value transactions, has measurable financial consequences.

The economics of reduced administrative friction

Consider a scenario involving:

- Large property acquisitions

- Cross-border remittances

- Corporate restructuring

- Bank due diligence requirements

- Investment fund onboarding

A delay in tax confirmations or documentation can affect transaction timelines, financing costs, or investor confidence. If the Privilege Card reduces even one procedural delay during a major transaction, its practical value may exceed the perceived intangible benefits many times over. In this context, the card becomes a risk mitigation tool rather than a prestige instrument.

Tax compliance is no longer merely a statutory obligation; it is increasingly becoming a marker of professional integrity and responsible economic citizenship

Strengthening reputation in a governance-conscious era

Post-crisis Sri Lanka has entered a phase where transparency, fiscal discipline, and governance standards carry heightened importance. International lenders, development partners, and institutional investors closely monitor compliance culture.

Formal recognition from the national tax authority signals:

- Consistent statutory compliance

- Financial transparency

- Responsible fiscal citizenship

For board members and public-facing professionals, this enhances credibility in ways that may not be immediately quantifiable but are strategically meaningful. In modern business ecosystems, reputational capital is a competitive advantage.

Structured engagement reduces uncertainty

Historically, many compliant taxpayers have experienced procedural bottlenecks, documentation mismatches, or communication delays. Even when fully compliant, navigating administrative channels can consume time and create uncertainty. By providing structured access and a nominated officer framework, the Privilege Card introduces predictability into that relationship. Advanced tax administrations such as HM Revenue and Customs, Inland Revenue Authority of Singapore, and Australian Taxation Office have long adopted differentiated engagement models for high-value compliant taxpayers. These frameworks recognise that relationship management reduces disputes, enhances voluntary compliance, and improves administrative efficiency. Sri Lanka’s initiative reflects a similar strategic direction.

Addressing the common concerns

Some eligible taxpayers worry that applying may invite additional scrutiny. However, the scheme is eligibility-based and grounded in demonstrated compliance performance. It does not create new tax liabilities. Instead, it formalises recognition of compliance already achieved.

Others question whether it may create perceptions of preferential treatment. Yet the criteria are rule-based and transparent, with defined tax payment thresholds. The system is not discretionary; it is performance-driven. The more relevant question may therefore be: If one is already fully compliant, what is the strategic disadvantage in formal recognition? The downside appears minimal. The potential efficiency and reputational upside is tangible.

Beyond individual benefit: A civic signal

High-value taxpayers shape compliance culture. When leading professionals visibly align with structured, transparent tax engagement, it reinforces broader societal norms. Participation signals that compliance is not merely a defensive act to avoid penalties, but a marker of responsible leadership. In a country rebuilding fiscal credibility and strengthening revenue systems, this cultural shift matters.

A strategic choice, not a symbolic gesture

The IRD Privilege Card should not be evaluated emotionally or symbolically. It should be assessed strategically.

For high-income individuals who already meet the eligibility thresholds, the card offers:

- Administrative efficiency

- Risk reduction

- Reputational enhancement

- Structured institutional engagement

In governance terms, it transforms compliance from routine obligation into recognised leadership. For Sri Lanka’s high-value taxpayers, the decision ultimately becomes clear:

If compliance is already your standard, formalising it through structured engagement is not a concession — it is a strategic upgrade.

(The author is a Chartered Accountant, MBA (UK), FCA (SL), FCMA (UK), FCPA (Aust.), CIMA (Aust.), FCMA (SL), MCPM (SL) and CGMA (Global)