Sunday Apr 19, 2026

Sunday Apr 19, 2026

Monday, 17 May 2021 00:30 - - {{hitsCtrl.values.hits}}

|

| Nishadi Tennakoon |

|

| Cover page

|

Resilience in financial systems

The financial system has been the livewire of any economy. That is because it provides a range of useful services to keep the economy alive. The most important of these services cover helping an economy to produce goods and services, exchanging them, expanding their production capacity, storing savings of those who consume less than their earnings, and making available such savings to those who spend more than they earn.

In the process, it mitigates the risks and cuts the costs of those who participate in the economy as consumers or producers. Hence, a well-functioning financial system is a blessing, while a defective one is a curse. But financial systems are subject to attack from within – called internal shocks – and from out – called external shocks. Once they are shocked, their ability to rise back and continue to provide their services – called resilience – is an important feature of a well-functioning financial system. It is like a physically fit person rises on his own after he has had a fall.

The job of the financial system regulator – in most countries the central bank and in some others, a financial services authority – has been to build this fitness in the system and consequentially its resilience. But resilience sometimes becomes an elusive goal and has to be pursued with carefully designed strategies, policies, and plans. Nishadi Tennakoon, a Deputy Director in the financial system stability cluster of the Central Bank, has helped us understand how we should pursue this goal through her latest publication, ‘Pursuit of Financial System Resilience’, released in April. It contains 16 essays that she has penned from time to time since 2016.

16 interconnected essays

Her essays do not stand alone despite the fact they have been written in different time periods. In fact, they are interconnected. She has started asking the common question which bothers many lay readers: why should a financial system be regulated? Then, she goes on to explaining why compliance of those regulations by individual financial firms – banks and other bodies that offer financial services – is important. Once a firm has fallen, the next question is whether it be resuscitated or simply weeded out. If it is weeded out, how should the depositors be protected?

Then she has focussed on the subtle issues relating to financial firm regulation. Should the corporate entity be punished for misbehaviour or should its human hands be taken to task for propelling such misbehaviour? After educating the reader of these basic issues, she has tackled multifarious aspects of the financial services industry that have a common impact on the community. The thread connecting all these essays is the need for building resilience and how it should be vigorously pursued.

Regulation of the financial services firms

Regulation of the financial services firms

Her first essay deals with the question of whether financial services firms be regulated or not. She has carefully weighed arguments for regulation and those against it. Those who are against regulation have been named ‘free bankers’ or ‘free marketers’, a term used interchangeably throughout the book to denote those economists advocating for the free-market economy system. How do they substantiate their claim? According to them, any control imposed on a firm – no matter whether it is a financial firm or not – is an impediment to its growth. Thus, the best governance for them is the self-governance. The best business environment is the least controlled environment. Tennakoon presents a number of arguments to repudiate these claims.

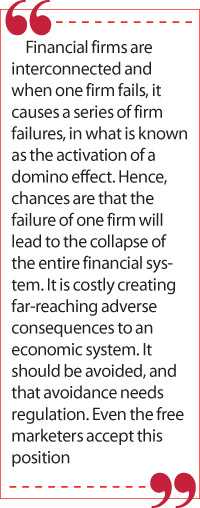

Financial firms are interconnected and when one firm fails, it causes a series of firm failures, in what is known as the activation of a domino effect. Hence, chances are that the failure of one firm will lead to the collapse of the entire financial system. It is costly creating far-reaching adverse consequences to an economic system. It should be avoided, and that avoidance needs regulation. Even the free marketers accept this position. They argue that governments have a case in regulating financial firms on the ground of producing a ‘public good’, a good needed by the public but not produced by the private sector.

Tennakoon has concluded her essay with a quotation of New York University’s don on financial regulations, Lawrence J White: “An efficient financial sector is important for economic growth and development, and an efficient financial regulation is crucial for an efficient financial sector. The beneficial results make the effort worthwhile”. This quotation summarises the main message which Tennakoon has conveyed in her essay.

Compliance from within a must

Regulations come from outside. But what is important is for a financial services firm is to adhere to such regulations on its own. This is called compliance and Tennakoon’s second essay is on the importance of compliance which she says stands at the heart of the financial services industry. It is necessary, according to her, to ensure “the safety and soundness of individual institutions as well as systemic resilience”. But it comes within the parameters of self-governance which those so-called free marketers have been advocating.

If compliance is not followed religiously, not even a ton of regulations can save a financial institution. Hence, it is in the interest of those within a financial services firm to adhere to compliance as a part of the organisational culture. In this respect, the example should be given by the people at the top of a firm. As the Silicon Valley inventor Robert Noyce has once said and quoted by Tennakoon in her essay, “If ethics are poor at the top, that behaviour is copied down through the organisation”. Once this organisational morality has been established, compliance with regulations should be made a part and parcel of the day-to-day behaviour of all those inside a financial services firm. Tennakoon says that it is the duty of the board of directors of a firm to ensure that compliance is being practiced as a passion and not as a fashion.

Resolution of problem financial services firms

Financial services firms may be stringently regulated, and they may have complied with such regulations fully. Yet some firms might fail because of the inherent weaknesses in them. Should these firms be weeded out? If they do not pose a threat to the financial system as a whole, in the interest of the system, there is a case for allowing them to die out. Tennakoon analyses this issue in her third essay titled ‘Should Weak Financial Institutions Be Allowed to Exit?’ Her answer is that, while zero failure is not a realistic goal, there should be a mechanism to resolve problem financial services firms.

According to her, resolution is a restructuring of a problem financial services firm by a special authority specifically set up for this purpose. She has presented to her readers diverse methods of resolution being carried out by different resolution authorities in the world. One such method is to establish a resolution fund to finance the resolution process.

Another is to get all financial services firms to file a ‘living will’ with the authorities providing their own resolution plan in the event of a major failure of the firm. This amounts to getting prepared for the eventual closure in advance. Tennakoon says that it is important to maintain a tight connection between the living will and the firm’s overall strategy for profitable growth.

Bring errant directors and managers to book

All financial services firms are corporate bodies and therefore they assume a legal personality. But behind these legal persons are natural persons, made-up of shareholders, directors, and managers. A salient feature of this system is that the legal person is responsible for its action and not the natural persons behind it. But it is these natural persons who make decisions that might lead to failure of the legal persons. In terms this legal structure, the natural persons go scotch-free though they may have been responsible for the failure of the firm. This is known as corporate veil.

Tennakoon says in her fifth essay that in modern regulatory systems, this corporate veil is pierced to make those natural persons responsible for the ill-fate of the financial services firms. In terms of this, while the corporate entity has a civil liability, the natural persons have a criminal liability for their wilful actions leading to scandals, frauds, and other misappropriations in a financial services firm. It will help, according to Tennakoon, a financial services firm to establish appropriate crime control policies. This should be a part of the corporate governance system being adopted by the firm.

Consumer protection, a journey

Consumer protection, a journey

Tennakoon has addressed the issue of protecting the depositors and other consumers of a financial services firm in several essays. Essay four has focused on deposit insurance, while essay nine has elaborated on consumer protection as a journey or a process. While deposit insurance helps establish trust among customers, Tennakoon says that it is not a ‘quick-fix’ for ensuring financial system stability. It is also marred with basic issues in any insurance scheme like the moral hazard problem and the adverse selection problem.

Moral hazard problem refers to the situation where managers of the firm knowing that the deposit insurance system would take care of depositors in the event of the failure of the firm would make risky choices triggering and accelerating its failure. Adverse selection occurs when financial services firms select businesses covered by deposit insurance with the intention of defaulting eventually.

Hence, if allowed to be present, both moral hazard and adverse selection problems will contribute to the failure of financial services firms which the regulators want to prevent at all costs. Tennakoon has suggested, going by global best practices, numerous ways of organising and implementing a deposit insurance system to minimise these problems.

Both buyers and sellers beware

With regard to the broad issue of consumer protection, her suggestion has been to empower the consumers by improving their financial literacy, on one side, and getting them to be careful when selecting financial products by adhering to a long-established principle in commerce, on the other. That principle known as Caveat Emptor warns customers to be careful when choosing any product. If the product is found to be defective later, it is the customer who is responsible and not the seller.

Tennakoon has referred only to Caveat Emptor but there is a new principle now established known as Caveat Venditor or Let the seller beware after the ill-fated Orange County Bankruptcy Case in California, USA. What this means is that managers in financial services firms are responsible if they have not properly advised the customers of the risks involved in selecting a particular product offered by them.

In Essay Ten, she has elaborated on the right to information as a part of the consumer protection and maintaining transparency in all business matters undertaken by a financial services firm. In this regard, she has argued for having a proactive disclosure system instead of having a reactive disclosure system. In Essay Eleven, Tennakoon has advised banking customers how they should avoid falling into financial scams and frauds. They include donations for fake charities, tempting proposals for quick-rich opportunities, unsolicited winnings, pyramid, and Ponzi schemes, etc.

Covering multifarious issues faced by financial services firms

The other essays in her volume deals with goals like inclusive banking, preventing money laundering and terrorist financing, going for green banking, adhering to appropriate fitness and propriety tests for directors and senior officers of these firms. Tackling these issues properly makes the financial landscape a proper place to operate by all the stakeholders of the industry.

A good read for all

Tennakoon has substantiated her claims by citing relevant references. It facilitates any reader to make further inquiry into these issues. Every essay has been ended with a pertinent quotation of an authority in the field. Since it summarises exactly what she has said in the essay, it would have been more relevant had those quotations been presented at the beginning of the essays. That would have served as a warning to readers what they should expect to find in the following pages.

Her writing style is lucid, clear and to the point. It makes the reading of her Pursuit a pleasant experience. I have noted two shortcomings in the formatting of the book. Both relate to the absence of a detailed reference list and an index at the end of the book. These two deficiencies could be rectified easily in a future reprinting of the book.

Nishadi Tennakoon’s Pursuit of Financial System Resilience is a good read for laymen, students and practicing bankers.

(The writer, a former Deputy Governor of the Central Bank of Sri Lanka, can be reached at [email protected].)