Tuesday Jun 23, 2026

Tuesday Jun 23, 2026

Tuesday, 23 June 2026 06:55 - - {{hitsCtrl.values.hits}}

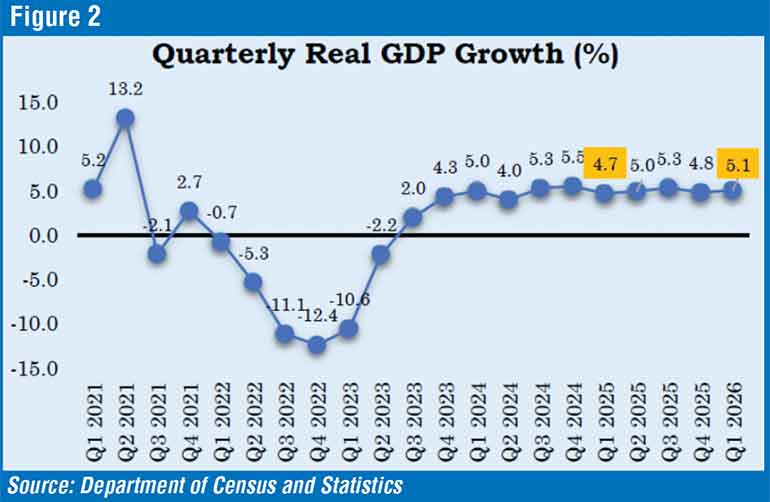

Sri Lanka achieved a year-on-year GDP growth of 5.1% in the first quarter of 2026, compared with 4.7% growth rate in 1Q 2025. It was the highest first-quarter growth recorded since 2021, reflecting economic recovery.

Sri Lanka achieved a year-on-year GDP growth of 5.1% in the first quarter of 2026, compared with 4.7% growth rate in 1Q 2025. It was the highest first-quarter growth recorded since 2021, reflecting economic recovery.

Such growth rates predicted by authorities are certainly welcome for improving people’s quality of life. But certain caveats behind such aggregate numbers need to be understood to meet the policy challenges ahead, without being carried away by occasional growth hikesThe country has failed to move to high-tech industries in contrast to fast-growing Asian countries. Sri Lanka’s high-tech exports account for only 1.4% of total manufactured exports, as against 58% in Malaysia, 56% in Singapore, 43% in Vietnam, and 28% in Thailand. Handicaps in science, technology, innovation, and knowledge-based products are major constraints to Sri Lanka’s growth dynamics.Cost escalation effectsThe rising production costs triggered by surging energy, transport, and borrowing expenses following the recent forex market volatility have dampening effects on economic activities. The recent rupee depreciation makes imported investment and intermediate goods costlier, although it has a positive impact on the export sector. A rise in borrowing costs can also be expected due to the recent increase in the Overnight Policy Rate (OPR) by the Central Bank, which was essential to deal with forex market volatility.Service sector is inward-orientedThe service sector is the largest contributor to the economy, accounting for 57% of GDP and providing employment for 50% of the country’s workforce. This sector is largely concentrated in domestic activities such as local wholesale and retail trade, transportation, financial services, and public administration. Approximately 88% of the output of the services sector is domestically consumed, and such products can be considered as non-tradables. Thus, Sri Lanka’s services sector is predominantly inward-oriented.Export-oriented services, known as tradables, account for only 12% of the total services output. A positive development observed in recent years is the significant growth of tourism and service exports related to information technology, communication, and business process outsourcing. These service exports earn foreign exchange amounting to $ 7 billion, equivalent to 35% of total foreign exchange earnings from goods and services.Way forwardTransforming the country’s production structure towards export orientation is essential not only to elevate the economy to a higher growth trajectory but also to ease the balance of payments difficulties. To this end, a coherent policy framework is required targeting the agriculture, industry, and service activities. Policy strategies are necessary for high-tech-based education and skills development, infrastructure development, regulatory reforms, and fiscal incentives. Efforts should also be made to attract FDI for high-tech, high-value-added service activities, instead of continuously relying on low-tech exports such as apparel products.The necessity to adopt such outward-looking policy strategies in the backdrop of the competitive, knowledge-based global economy should not be masked by complacency about temporary and unsustainable spikes in GDP growth.(The author, Emeritus Professor in Economics at the Open University of Sri Lanka, is the President of the Sri Lanka Economic Association and the Honorary Deputy Chairman of the Gamani Corea Foundation)

Recent columns

COMMENTS