Saturday Jul 04, 2026

Saturday Jul 04, 2026

Wednesday, 27 May 2026 00:21 - - {{hitsCtrl.values.hits}}

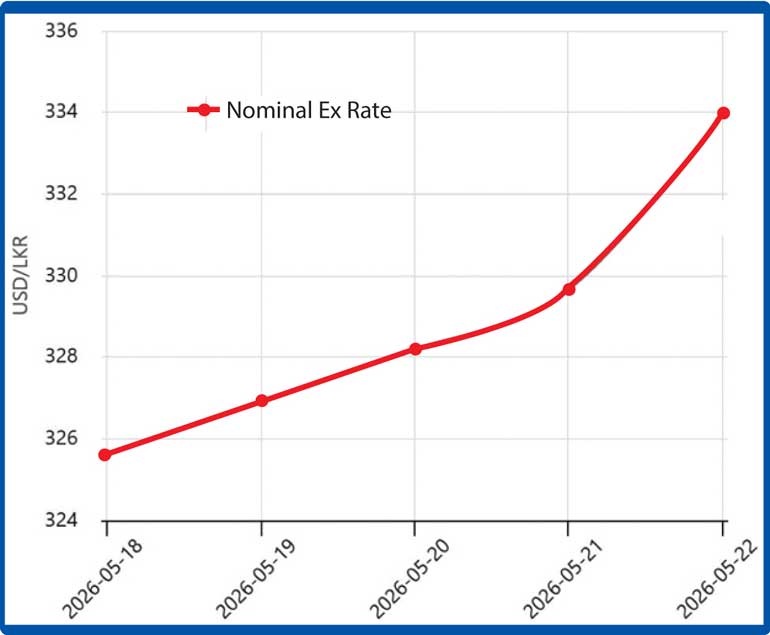

Many economic crises emerge not merely from lack of resources, but from misunderstandings of how the modern economy and monetary system work. Parliamentarians make policy decisions or they are led to make decisions by bureaucrats that directly affect the exchange rate, investment, the volume of tradable goods and services, inflation, growth, employment, debt sustainability, and social stability. Recent policy action to impose a 50% surcharge on vehicle imports and a single gazette publication in regard to that virtually led to the crash of the LKR (rupee). Still, the economy is feeling aftershocks. When things go wrong, defending the erroneous action is a catastrophe. See the chart below. It shows the recent unintended movement of the exchange rate.

Many economic crises emerge not merely from lack of resources, but from misunderstandings of how the modern economy and monetary system work. Parliamentarians make policy decisions or they are led to make decisions by bureaucrats that directly affect the exchange rate, investment, the volume of tradable goods and services, inflation, growth, employment, debt sustainability, and social stability. Recent policy action to impose a 50% surcharge on vehicle imports and a single gazette publication in regard to that virtually led to the crash of the LKR (rupee). Still, the economy is feeling aftershocks. When things go wrong, defending the erroneous action is a catastrophe. See the chart below. It shows the recent unintended movement of the exchange rate.

The previous narration a few years ago was different. It says that an increase in Government credit from the banking sector or printing money would lead to inflation and depreciate the currency. That was the story planted in the media and society. This time, there is no increase in Government spending through bank borrowings and absolutely no printing of money. But we have an exchange rate crisis. The Central Bank argues that even LKR depreciates there is no increase in external debt in dollar terms. This is true, but local currency depreciation could lead to many bad things. It may ruin investor confidence, the market could begin doubting the sustainability of the managed exchange rate, exporters might delay converting dollars, hoarding of foreign exchange might take place, and remittances might be delayed. All these create self-imposed pressure on the LKR. Are these things good?

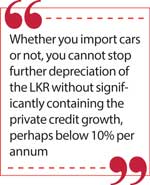

Those experts who are on the other side of the political divide want to ban the import of passenger cars. That’s a solution, but a bad one under the current circumstances. Responding to that argument, Minister Prof Anil Jayantha Fernando insisted that there would not be any ban on vehicle imports. But one thing is certain. Whether you import cars or not, you cannot stop further depreciation of the LKR without significantly containing the private credit growth, perhaps below 10% per annum.

There was excessive private credit growth in the first quarter of this year. It exceeds an annualised figure of over 20%. The IMF wanted to have private credit growth below 10% for the years 2025, 2026 and 2027, unadjusted for inflation. The private credit or loans, created by commercial banks, are virtual money, sometimes known as “credit money.” Therefore, any increase in private credit is like printing new money. This is an important monetary parameter. That’s the very reason the IMF wanted the private credit growth to be in the upper single-digit range. The Government lifted the ban on passenger car imports, but took no precautions to contain private credit growth as agreed with the IMF.

Sri Lanka is a country that Rs. 10,000 salary increase to Government employees destabilised the rupee heavily, by nearly a threefold increase of vehicle imports in one year when Ravi Karunanayake was the Minister of Finance. We should have learned from history. Instead of taking precautions to contain private credit growth, CBSL wanted to lift the ban on vehicle imports. As a result, “accumulated demand’ for 4 to 5 years kicked in and, with a relatively low rate of interest, car imports were significant and the private credit growth skyrocketed, destabilising the exchange rate mechanism now. The same previous story, amplified by external shocks created by geopolitical reasons.

Sri Lanka is a country that Rs. 10,000 salary increase to Government employees destabilised the rupee heavily, by nearly a threefold increase of vehicle imports in one year when Ravi Karunanayake was the Minister of Finance. We should have learned from history. Instead of taking precautions to contain private credit growth, CBSL wanted to lift the ban on vehicle imports. As a result, “accumulated demand’ for 4 to 5 years kicked in and, with a relatively low rate of interest, car imports were significant and the private credit growth skyrocketed, destabilising the exchange rate mechanism now. The same previous story, amplified by external shocks created by geopolitical reasons.

Now, some suggest to shrink the economy. This is not a proper solution. Instead, the solution is to contain the private credit growth so that the economy will grow in a reduced phase while stabilising the currency in the short term.

Stable exchange rate mechanism means the predictability of the rupee, subject to a stable depreciation of 5 to 7% annually. There is no need to bring it back to 300 for a USD range. The Government should not be fascinated by thinking that there are foreign reserves of around $ 7 billion. On paper, it is true, but a significant portion of it too, is borrowed money by Central Bank. Policy makers must be more careful because policy failures are often unintentional.