Tuesday Jun 30, 2026

Tuesday Jun 30, 2026

Thursday, 9 April 2026 00:22 - - {{hitsCtrl.values.hits}}

Sri Lanka urgently needs foreign capital. For years the country has relied on foreign direct investment (FDI) as the primary channel for external inflows. Yet FDI arrives slowly. Even when major investments materialise, their economic impact takes time: factories must be built, infrastructure developed and employment expanded.

Sri Lanka urgently needs foreign capital. For years the country has relied on foreign direct investment (FDI) as the primary channel for external inflows. Yet FDI arrives slowly. Even when major investments materialise, their economic impact takes time: factories must be built, infrastructure developed and employment expanded.

There is, however, a faster channel that remains largely underutilised — the capital market.

Equity investment can move instantly across borders. With a single transaction, international investors can deploy capital directly into an economy. Yet Sri Lanka’s stock market remains too small and shallow to attract serious global funds.

The problem is not simply valuation. The problem is scale.

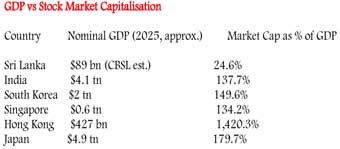

Sri Lanka’s equity market capitalisation is roughly $27 billion, a fraction of regional markets. Pakistan’s market stands near $70 billion, while India exceeds $5 trillion, Japan Exceeds $9 Trillion. For large institutional investors managing billions, Sri Lanka presents a practical dilemma: it is difficult to deploy meaningful capital without distorting prices or encountering severe liquidity constraints.

Low valuations alone cannot solve this problem.

Sri Lanka’s market trades at roughly 10 times earnings, far below India’s multiple of around 25. On paper this should attract investors. But institutional capital demands more than cheap prices. Investors need depth, liquidity, and a broad range of investable companies.

Sri Lanka’s stock market is tiny compared to global peers: its market capitalisation is only about 27 billion USD, while India, Hong Kong, Singapore, and Japan all have market caps that exceed their GDPs. This highlights the urgent need to expand listings—especially SOEs—to make Colombo attractive to foreign investors.

Implications for Sri Lanka

Sri Lanka currently offers too few.

Sri Lanka currently offers too few.

The Colombo Stock Exchange does not adequately reflect the true structure of the national economy. Many of the country’s most important sectors remain absent from the capital market — including major state-owned banks, utilities, insurance institutions, transport enterprises, and infrastructure companies.

As a result, the market remains narrow and lacks the scale required to attract significant foreign participation.

The solution is straightforward.

Sri Lanka must bring more companies to the market.

In particular, partial listings of state-owned enterprises (SOEs) would dramatically expand the capital market. This does not require full privatisation. The Government could retain majority ownership while offering 10–20 percent of shares to the public.

Such a move would achieve several critical objectives.

In successful economies, the stock market mirrors the real economy. Key industries are represented and investors can participate in their growth. Sri Lanka must move toward this model if it wishes to develop a deeper capital market.

The Airline question: From burden to opportunity

Sri Lankan Airlines illustrates the broader challenge.

For years the national carrier has operated under a heavy debt burden, limiting its attractiveness to investors. A debt-laden airline cannot realistically be listed on the market or presented to global investors as a compelling opportunity.

The alternative is restructuring.

If the airline’s balance sheet were cleaned and historical losses absorbed, a debt-free carrier could be transformed into an investable entity. With transparent governance and a credible operational strategy, Sri Lankan Airlines could be introduced to global investors through targeted roadshows in major financial centres such as Singapore, Hong Kong, London and Dubai.

Such investors are not interested in distressed assets. They seek growth stories backed by credible reform.

A clean airline could attract foreign exchange inflows, strengthen Sri Lanka’s aviation sector and reinforce the country’s ambitions to become a regional tourism and logistics hub.

Absorbing past losses may appear painful. In reality, those losses already exist. Restructuring simply converts a liability into a platform for investment.

A political window for reform

Reforms of this magnitude inevitably provoke resistance. Privatisation debates are politically sensitive, and vested interests often mobilise quickly against change.

Yet moments of political opportunity do arise.

When Governments enjoy strong parliamentary mandates, they possess the authority required to implement structural reforms. If capital market reform cannot be undertaken under such conditions, it becomes difficult to imagine when it ever will.

Key observations

What Sri Lanka can learn from Hong Kong

Hong Kong’s extraordinary ratio—stock market capitalisation at 1,420% of GDP—illustrates what is possible when a financial hub becomes a magnet for global capital. Its success was built on scale, liquidity, international listings, and investor-friendly policies.

Sri Lanka, by contrast, remains a “tiny dot” on the global investment map. To attract institutional investors, the country must expand market capitalisation, improve liquidity, and create investable assets. Listing state-owned enterprises (SOEs) even partially—banks, insurers, utilities, and airlines—would significantly enlarge the market, while retaining Government control.

Port City and a shifting global landscape

Global instability often reshapes economic opportunity. Recent tensions in the Middle East highlight how geopolitical risk can alter investment patterns. When uncertainty rises in one region, investors inevitably search for stable alternatives.

Historically, cities such as Dubai have attracted global wealth by offering stability, connectivity, and investor-friendly policies. Yet when regional risks increase, capital looks for other destinations.

Sri Lanka’s Colombo Port City is uniquely positioned to seize this moment. With its special economic zone framework, the Port City could host a modern, internationally oriented stock exchange designed to attract global listings and capital flows. By mirroring aspects of Hong Kong’s success, Sri Lanka could transform Port City into a gateway for international investors seeking stability and opportunity in South Asia.

The Port City Stock Exchange vision

Regulation in place for a Port City Exchange

A Port City Exchange could:

This vision aligns with global shifts in capital flows. As investors diversify away from regions marked by instability, Colombo Port City could emerge as a credible alternative—combining geographic advantage, policy innovation, and financial ambition.

Global instability can also reshape economic opportunity.

Recent tensions in the Middle East illustrate how geopolitical risk can alter investment patterns. When uncertainty rises in one region, investors inevitably begin searching for stable alternatives.

Historically, cities such as Dubai have attracted global wealth by offering stability, connectivity and investor-friendly policies. Yet when regional risks increase, capital looks for other destinations.

Asia naturally becomes part of that search.

Countries such as Thailand, Malaysia, Indonesia, India — and potentially Sri Lanka — come into focus for investors seeking both security and growth.

This is where Colombo Port City becomes strategically significant.

The project was designed as an international financial and residential hub capable of attracting global capital. If properly positioned, it could become a gateway connecting South Asia with international investment flows.

But opportunity does not materialise automatically.

Sri Lanka’s investment agencies must actively market the country. Global roadshows, investor forums and targeted outreach in major financial centres are essential. At the same time, regulatory clarity, competitive tax policies and efficient approvals must be guaranteed.

Investors compare jurisdictions constantly. Sri Lanka must ensure it remains competitive with regional financial hubs.

If approached strategically, Port City could attract substantial investment, strengthen the financial sector and enhance Sri Lanka’s international economic profile.

But the window for such opportunities rarely remains open indefinitely.

Conclusion: The need for policy courage

Sri Lanka does not lack economic potential.

What it lacks is scale.

By expanding the capital market through partial listings of major enterprises, the country could rapidly increase market capitalisation, attract institutional investors and strengthen governance standards.

Combined with strategic positioning of Port City, these reforms could transform Sri Lanka into a far more attractive destination for global capital.

The opportunity is visible.

What is required now is policy courage and strategic vision.

The choice is simple.

Act decisively — or watch the opportunity pass.