Friday Jul 10, 2026

Friday Jul 10, 2026

Friday, 10 July 2026 00:00 - - {{hitsCtrl.values.hits}}

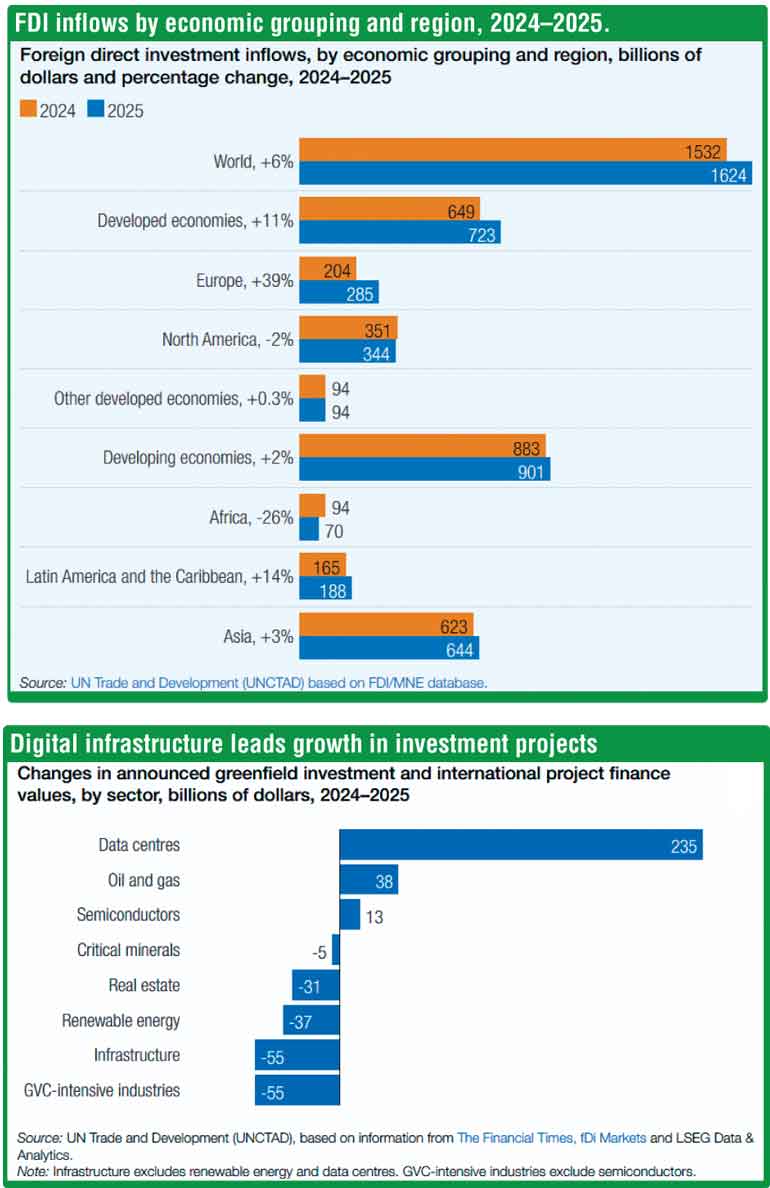

Global foreign direct investment (FDI) rose 6% to $ 1.6 trillion in 2025, ending two years of decline, but the recovery remains narrow, fragile, and uneven, according to the World Investment Report 2026 by UN Trade and Development (UNCTAD) released this week.

Inflows to developed economies rose 11%, while developing economies recorded only 2% growth, reaching $ 901 billion. The figures point to a rebound that is not translating evenly into development opportunities. The issue is not only how much capital is moving, but where it is going, what it is building, and whether it is expanding productive capacity, creating jobs, strengthening skills, and supporting technology transfer.

The world’s top 20 host economies attracted more than 80% of global FDI in 2025, underscoring a trend that runs throughout the report: investment is becoming more concentrated across countries, sectors, and projects.

The recovery should also be interpreted with caution: headline FDI numbers do not always translate into new factories, infrastructure, jobs, or technology transfer.

Developing economies received more than half of global FDI in 2025, but growth was modest and uneven across regions. Developing Asia remained the largest recipient region, attracting $ 644 billion, while Latin America and the Caribbean rose 14% to $ 188 billion and Africa received about $ 70 billion, still one third above its 2010-2024 average despite falling from the exceptional level reached in 2024. Least developed countries saw inflows rise 21% to $ 43 billion, but still accounted for only 2.7% of global FDI, with flows concentrated in a small number of mostly resource-rich economies.

This concentration is particularly visible in industries linked to technology, energy, and industrial policy. Strategic sectors such as Artificial Intelligence (AI) infrastructure, semiconductors, critical minerals, and energy-transition technologies and services accounted for 44% of global greenfield project values in 2025, up from 16% in 2020.

The growth in project values was driven mainly by data centres, followed by oil and gas and semiconductors. Most other sectors registered declines, including renewable energy, infrastructure, and manufacturing, showing how narrow the recovery remains.

Low-income and lower-middle-income economies attracted only about 10% of strategic-sector investment between 2020 and 2025, compared with more than 20% in other sectors.

Governments are also taking a more active role in shaping investment flows. In 2025, countries adopted a record 229 investment policy measures. While most remained favourable to investors, many were designed to attract investment into strategic industries, strengthen domestic economic priorities, or respond to economic security concerns.

For developing countries, the new investment landscape brings both opportunities and risks. But many countries risk being left behind as investment becomes more capital-intensive, technology-intensive, and shaped by policy support that many developing economies cannot easily match.

UNCTAD says developing countries need more than investment promotion to compete in this environment. They need realistic entry points into evolving value chains, stronger investment facilitation, reliable infrastructure, workforce skills, supplier development, and regional markets that make projects more viable. International cooperation will also be needed to ensure that investment partnerships support both resilience for investors and development priorities for host economies.

Prospects for 2026 remain difficult. Trade policy uncertainty, geopolitical tensions, conflicts, high financing costs, and economic fragmentation continue to weigh on investment decisions. At the same time, competition for projects linked to strategic industries is expected to intensify as governments seek to secure future sources of growth and technological advantage.

The findings will help frame discussions at UNCTAD’s World Investment Forum 2026, to be held in Doha, Qatar, from 25 to 27 October, where governments, investors, and development partners will examine how to turn a more selective investment landscape into broader development gains.

The central question is no longer simply how much investment is moving across borders. It is where that investment is going, what it is building, and who stands to benefit from it.