Saturday Apr 25, 2026

Saturday Apr 25, 2026

Thursday, 22 September 2016 00:00 - - {{hitsCtrl.values.hits}}

One bad season has the ability to throw the smallholder away from cultivation for good. Hence smallholder farmers in countries like ours are more vulnerable to shocks

Agriculture production is vulnerable to many changes. These are mainly environmental and technological. Environmental changes can be floods, droughts, sea level rise (for coastal agriculture), change in the atmospheric temperature and even land degradation.

Environmental changes are hard to deal with since they have a lower predictive power. Even the most sophisticated scientific models are only capable of predicting environmental changes to a certain degree. Thus controlling environmental changes relies on either adaptation or mitigation. The best example is the impact of climate change on agriculture.

Changes brought on by technological needs are opportunities rather than challenges. The technological needs call for innovation and the increased use of machinery in agriculture, which positively impacts production efficiency.

Whether it is a change caused by a changing environment or technological need, the impact of it comes through the market system. Both environmental and technological changes will cause either supply or demand to change causing prices to fluctuate. These price fluctuations can either favour the farmer or the consumer.

In economic terms the changes caused by the environment and technology are called ‘shocks’. Some shocks are only short-term and some are long-term. For example a drought will only effect cultivation for a couple of seasons but the impact will wear off afterwards. However, land degradation caused by excessive fertiliser use might take 5-10 years to recover.

Whenever such a shock occurs, the market system is supposed to respond. If there is a price hike, then consumers will move on to substitutes. This is very common with the vegetable market. When the price of a particular vegetable is high consumers will buy less (or some other vegetable) and the opposite occurs when the price is low. Then the question arises, “Why do we have to worry about this, can’t we allow the market system to respond and wait till things get settled?”

Time series fluctuations due to environmental and technological changes might not be an issue for a large-scale commercial farmer. The economies of scale he works on will balance off any changes over time. However, this is not the case for the smallholder who operates on formal and informal credits, small land holdings and inefficient value chains. One bad season has the ability to throw the smallholder away from cultivation for good. Hence smallholder farmers in countries like ours are more vulnerable to shocks. This is the main reason why governments get involved whenever there is a shock without waiting for the market system to adjust.

The Government’s involvement in mitigating the impact of shocks in agriculture markets takes many forms. There are subsidies, guaranteed price programs, out output sealing and taxes. These interventions need the direct involvement of the Government. However, there are ways that could potentially address the impacts of shocks but with less Government involvement. Crop Insurance is one such popular approach.

Why Crop Insurance?

Crop Insurance is something that agricultural producers have to purchase. The insurance is mainly against the losses suffered due to environmental changes, chiefly floods and droughts.

It can also cover losses in profits due to unexpected declines in the prices of agricultural commodities. In many developing countries, farmers operating all sizes of farms retain the risk of crop losses. Their risk management mainly consists of diversifying their income sources by planting a variety of crops and breeding cattle. They have hardly any risk transfer tools, which in turn limits the availability and range of agricultural production credit offered by banks. Therefore, the development of sustainable risk management systems and tools, one of them being agricultural insurance, will be a key topic in future agricultural development strategies as well as in climate change mitigation strategies.

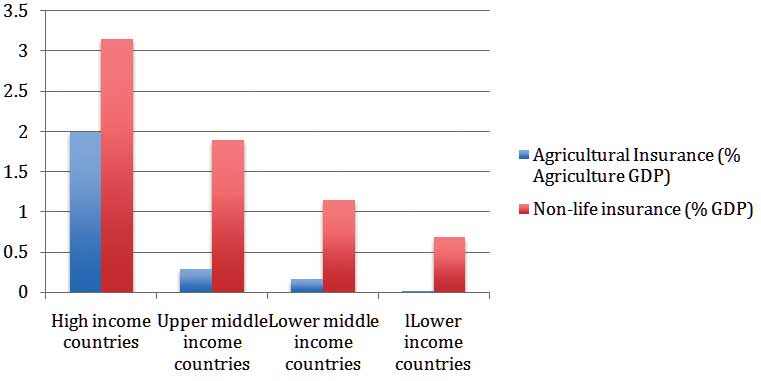

Though many talk about the importance of crop insurance for developing countries, the uptake of such programs has been slow. Figure (1) illustrates the slow uptake of crop insurance in developing countries.

Types of available crop insurance

In the discussion on agricultural insurance in developing countries and emerging markets, it is misleading to look for the solution at the product level first and foremost.

The problem of appropriate risk management tools in agriculture cannot be solved with an insurance product alone, neither with an index-based insurance product nor an indemnity-based insurance product. This is why none of the proposals of index insurance over the last few years have resolved the problem of a lack of risk management tools in developing countries.

This is not necessarily due to the type of product but to the lack of implementing the adequate framework that any insurance product needs. In other words, a systematic approach has to be pursued before we can tackle the question of which insurance product is appropriate. Such a systematic approach creates the adequate legal, institutional and organisational framework in which insurance products and other risk management tools can work efficiently.

This means that the challenge involves developing national agricultural insurance systems corresponding to the specific needs of the different production sectors and addressing the interests of all stakeholders (producers, Government, lending institutions and insurance industry). The objective of such a crop insurance system is to make insurance covers available to the majority of production sectors and to farmers.

Broadly, there are indemnity-based insurance and index-based insurance products. Indemnity-based insurance products assess losses at the farmer level. The main examples of such crop insurance programs are damaged-based insurance products and yield-based insurance products. Index-based insurance products assess losses using a measure of an index that is assumed to proxy the actual losses.

Famous approaches under this category are area yield-based insurance index, weather index-based insurance and normalised difference vegetation index insurance.

Among the approaches explained, their application will vary from country to country. However, some are quite popular among many developing countries.

One of the most popular methods is the weather index-based insurance program.

The advantages of a weather index-based insurance program are that it is objective and transparent and creates quick payout, reduced administrative costs, promotes access to finance and facilitates international reinsurance.

However, there are disadvantages as well and those are the risk of a mismatch between losses and payouts, single risk protection, high input requirements during the development stage and it is slow in scaling up. It is clear that the process of introducing crop insurance is not easy. Much has to be done in order to figure out what works for you best. Maybe we have to think out of the box.

Integrating modern technology into insurance products such as weather index-based insurance could be a potential solution. I will focus on this during the last part of this article.

Implementing a successful crop insurance program: essential ingredients

The implementation of a successful crop insurance program demands that many areas are looked at. The aim of this section of the article is to highlight some of these important things for the future planning of crop insurance programs:

(1) Ability to respond to the heterogenic structures in the crop production sector (e.g. large-scale, medium-sized and smallholder farms as well as different production sectors) and provide individual risk management solutions to each of them. Sustainable production methods and the use of the best available production techniques are a prerequisite of insurance. Cooperation with extension services might be beneficial.

(2) Crop insurance systems to be organised and financed as public-private partnerships between the Government, farmers and the insurance industry.

(3) Joint market approach by all insurance providers and risk carriers, e.g. in the form of a coinsurance pool. In such a pool, all crop risks of one country or even several (smaller) countries are combined, thus creating a better spread of risk. This joint market approach includes market-wide uniform insurance terms and conditions, which are technically sound and applied by all insurance providers. This is a very important element to guaranteeing the sustainability of the system.

(4) Centralised technical entity run by the insurance industry, which bundles the technical expertise, maintains an extensive database and carries out loss adjustment according to standardised procedures and methods.

(5) Integrate financial institutions like rural banks as well as agricultural input, output and extension service providers (including co-operatives) in order to promote and market insurance products efficiently.

If you look at these important areas, one of the most important of them is public-private partnerships. The importance of it requires further analysis on the process. The following things are very essential in establishing public-private partnerships in building a crop insurance program:

(1) Underwrite agricultural insurance through Private Commercial Insurers wherever possible.

(2) Important areas of Government support are data infrastructure (speed, reliability/quality and transparency), education, training and capacity building, technical support on product design and rating and creating enabling legal and regulatory framework.

(3) Exercise caution with agricultural insurance premium subsidies – smart subsidies to support well‐defined social objectives.

(4) In some circumstances, Government support as a Reinsurer of Last Resort may be justified.

(5) Innovations in distribution channels and delivery mechanisms.

(6) Long‐term effort that needs strong political commitment and strong technical counterparts.

Focus for Sri Lanka

Much research has been done and much more is under way to understand the crop insurance process in Sri Lanka. However, many crops, especially ones that are in the export value chain, operate without proper crop insurance schemes.

A popular argument of insurance suppliers is that farmers are reluctant to pay an insurance premium. At the same time farmers argue that they are never compensated properly when needed. However, with changing environmental conditions and technological changes, shocks in the agricultural production process are inevitable, thus crop insurance is essential. We need to solve four main problems in order to establish a sound crop insurance program in Sri Lanka:

(1) A lack of clarity over the respective roles of the public and private sectors.

(2) A lack of the risk market infrastructure necessary to foster agricultural insurance.

(3) Domestic insurance providers and public decision-makers often lack technical capacity.

(4) A lack of adequate tools and indicators to monitor and evaluate agricultural insurance programs (particularly index-based insurance).

Thinking out of the box

I expressed concerns over popular methods such as weather index-based insurance. The fact that this kind of insurance leaves a considerable basis risk with the individual farmer was simply overlooked. This is due to the relatively low correlation (as low as 60 %) between trigger and actually harvested yield and the fact that only one or in the best case two natural hazards are covered.

This has resulted in situations where farmers have suffered considerable crop losses without the policy indemnifying a situation, which is disastrous for the farmer as well as the insurance industry because of the loss of confidence and acceptance amongst farmers and Government representatives.

Another problem arising from index insurance is that the farmer, especially the smallholder farmer, does not understand and cannot trace the real mechanism of the cover. To give an example: smallholder farmers very often don’t really know how many millimetres of rainfall are needed for a decent crop. As a consequence, demand by farmers for such covers has generally been much lower than anticipated by the promoters of index insurance.

Consequently, index insurance based on meteorological triggers should be offered to individual farmers only under clearly defined conditions: a thorough understanding by the farmer of the mechanism of index insurance and the basis risk involved; financial capability of farmers to bear the basis risk.

This does not mean that index insurance might not play a role in risk transfer for the agricultural sector. Area yield index insurance for instance has proved to work for smallholder farmers under certain conditions (catastrophic losses, homogeneous regional production potentials) too.

The potential for covers based on meteorological triggers, however, lies more at the aggregate level than at the level of individual farmers. Instead of covering the individual farmer, the cover should apply at the aggregate level e.g. for covering a crop credit portfolio or a portfolio of a cooperative. Under these circumstances, the aggregating body can absorb the basis risk. The problem regarding how to distribute indemnification in case of losses to the individual lenders or co-operative members still has to be solved, e.g. by providing individual covers to them.

With the development of microfinance in the last decade, microinsurance has been developed and promoted strongly as well. Nevertheless, so far, neither microfinance nor microinsurance (defined as finance or insurance designed for low-income people or businesses not served by typical social or commercial insurance schemes) have made their way into the area of crop production.

Although this is not surprising, it is often not realised because rural microfinance or insurance normally does not include crop production. To serve smallholder farmers with much needed capital via production credits, a joint effort by different sectors is necessary. Microfinance institutions play a vital role in this process but they will be successful only if they integrate their efforts with input and output marketing services along the agricultural value chain. Furthermore, the (micro) finance and insurance industry as well as the Government need to form a public-private partnership.

Nowadays, remote-sensing technology for agricultural applications is rapidly developing: plot identification, yield estimations and assessment of loss events and vegetation status are only some examples which will enhance crop insurance and other risk management tools. Once it is possible to determine yields accurately with remote-sensing technology, yield-based coverage might be feasible also for smallholding farming.

Furthermore, insurance products using a remotely sensed vegetation index will gain further importance, especially in covering extensive farming.

(Chatura Rodrigo PhD is an agriculture and environment economist. This article is based on literature and filed explorations. Literature is available upon request. He can be reached at [email protected] and 94 77 986 7007).