Tuesday Jul 14, 2026

Tuesday Jul 14, 2026

Wednesday, 25 January 2017 00:00 - - {{hitsCtrl.values.hits}}

For the sixth consecutive year, MTI Consulting in partnership with Daily FT, Daily Mirror and Sunday Times, has concluded the MTI CEO Business Outlook Survey, collectively outlining the Sri Lankan business community’s perception for the state of business in 2017.

For the sixth consecutive year, MTI Consulting in partnership with Daily FT, Daily Mirror and Sunday Times, has concluded the MTI CEO Business Outlook Survey, collectively outlining the Sri Lankan business community’s perception for the state of business in 2017.

Supplemented by MTI’s experience as a thought leadership-oriented organisation, the annual survey collated and analysed the perceptions of over 200 Sri Lankan business leaders with regard to their business’ past and expected performance, their predictions regarding the state of the local and global economy in 2017, and the main challenges they believe Sri Lanka and their companies will face in 2017.

The results of the survey, including its supplementary analysis, will enable organisations to streamline their strategic decision making for 2017, effectively enabling them to gear their operations in accordance with the economic sentiments of their peers.

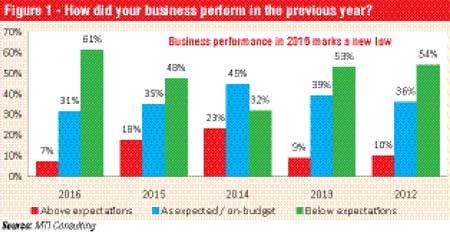

A total of 61% of the CEOs reported their businesses have performed below expectations in 2016. This shows an increasing trend from 2014 onwards. As opposed to 68% and 53% respondents from 2014 and 2015 respectively, only 38% of respondents stated that their business performed either as expected or above expectations.

A total of 61% of the CEOs reported their businesses have performed below expectations in 2016. This shows an increasing trend from 2014 onwards. As opposed to 68% and 53% respondents from 2014 and 2015 respectively, only 38% of respondents stated that their business performed either as expected or above expectations.

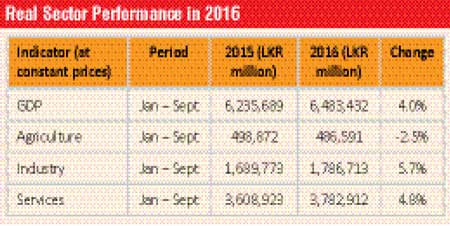

To supplement the CEO perceptions on 2016, MTI analysed the key macro-economic indicators of Sri Lanka for 2016.

The growth drivers in the Industry sector in the third quarter were Construction and Mining and Quarrying. Growth in the Service sector in the third quarter was a result of expansion in the categories of Financial Services, Insurance, Telecommunication, Education and Wholesale and Retail Trade. Amidst unconducive weather conditions such as droughts and flooding, the Agriculture sector witnessed a contraction of 2.5%. Reduction in the production of tea and rubber also contributed to the decline.

The growth drivers in the Industry sector in the third quarter were Construction and Mining and Quarrying. Growth in the Service sector in the third quarter was a result of expansion in the categories of Financial Services, Insurance, Telecommunication, Education and Wholesale and Retail Trade. Amidst unconducive weather conditions such as droughts and flooding, the Agriculture sector witnessed a contraction of 2.5%. Reduction in the production of tea and rubber also contributed to the decline.

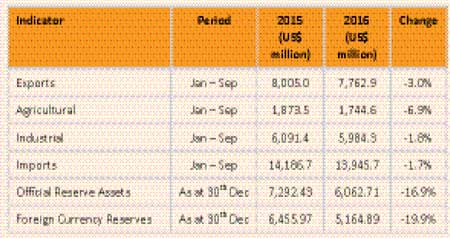

Considering many indicators, including exports and reserves, the External sector performed poorly in 2016 compared with 2015. The decline in the country’s reserves, despite the IMF package is a serious cause for concern – according to economists. The three-year $ 1.5 billion loan from the IMF was approved in June 2016. However, despite IMF support, the present reserves are not sufficient to meet Sri Lanka’s debt repayments for this year.

Considering many indicators, including exports and reserves, the External sector performed poorly in 2016 compared with 2015. The decline in the country’s reserves, despite the IMF package is a serious cause for concern – according to economists. The three-year $ 1.5 billion loan from the IMF was approved in June 2016. However, despite IMF support, the present reserves are not sufficient to meet Sri Lanka’s debt repayments for this year.

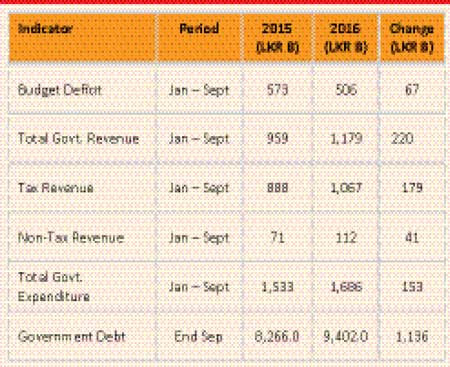

The reduction in the budget deficit and the increase in total Government revenue are encouraging signs. However, these positives are perhaps more than offset by an increase in total Government expenditure and more importantly a rapid increase in Government debt. The stock of Government debt has risen by 13.7% – when comparing the end September debt stock in 2016 against the same period of 2015.

The reduction in the budget deficit and the increase in total Government revenue are encouraging signs. However, these positives are perhaps more than offset by an increase in total Government expenditure and more importantly a rapid increase in Government debt. The stock of Government debt has risen by 13.7% – when comparing the end September debt stock in 2016 against the same period of 2015.

Upward movement could be seen in both the policy interest rates and lending rates of commercial banks (by 1% and 4% respectively). After increasing the Statutory Reserve Requirement (SRR) in December 2015, in July 2016 the Central Bank increased the Standing Deposit Facility Rate and the Standing Lending Facility Rate, by 50 basis points each. According to media reports, total private credit granted during the first nine months of 2016 has increased to Rs. 516 billion from Rs. 398 billion recorded during the same period the previous year. This represents an increase of nearly 30%. The Central Bank expects inflation to remain at mid-single digits in the period ahead.

The All Share Index (ASI) declined by 9.7% to 6,228 points and S&P SL20 index declined by 3.6% to 3,496 points at end 2016 with compared to 6,895 and 3,626, respectively, as at end 2015. CSE lost Rs. 193 b from its market capitalisation by the end of 2016 to stand at Rs. 2,745 b as compared to Rs. 2,938 b at the end of 2015. Annual turnover stood at Rs. 176.9 b which was lower by Rs. 76.3 b and Rs. 164 b than 2015 and 2014 respectively. According to an analysis of the latest (September 2016) quarterly reports published by the CSE S&P 20 revealed that 20% of the companies experienced a year-on-year drop in net earnings while 10% experienced only single digit growth.

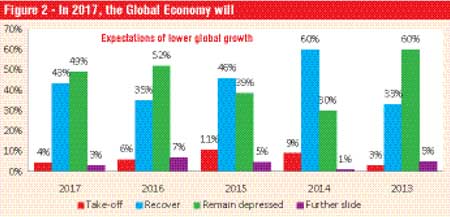

Global economic growth remained soft in 2016 for numerous reasons which vary by region. Generally, the culprits include structural adjustments in many countries, efforts to reduce overcapacity, recurring natural disasters, geopolitical events such as Brexit and the ongoing civil war in Syria. Appointment of new president in USA, Donald Trump, as well as potential policy changes in the US created many uncertainties in global economy. Comprehensive data showed that the global economy grew 2.6% year-on-year in Q3 (at current exchange rates) and remains on track to have grown 2.5% overall in 2016.

Global economic growth remained soft in 2016 for numerous reasons which vary by region. Generally, the culprits include structural adjustments in many countries, efforts to reduce overcapacity, recurring natural disasters, geopolitical events such as Brexit and the ongoing civil war in Syria. Appointment of new president in USA, Donald Trump, as well as potential policy changes in the US created many uncertainties in global economy. Comprehensive data showed that the global economy grew 2.6% year-on-year in Q3 (at current exchange rates) and remains on track to have grown 2.5% overall in 2016.

In contrast to what CEOs predicted, World Bank and the IMF forecasted the real value of goods and services produced globally to grow by 2.7% and 3.4% respectively in 2016 – up by 0.4 and 0.3 percentage points respectively from the previous year.

Goldman Sachs forecasted rising interest rates and inflation and upward pressure for USD as the key challenges for USA this year. There will be further impact from the new Trump administration’s tax reforms, fiscal easing, and investments in infrastructure and protectionist propagandas.

Growth is seen slowing slightly in the Eurozone in 2017, after coming in at an expected 1.6% in 2016. A rise in inflation will reduce tailwinds to consumption, and investment growth is likely to slow amid heightened uncertainty. Despite the easy monetary policy and improvements, crowded election cycle can create political and economic uncertainties in Europe.

Key growth drivers of Asia would be high productivity, especially in China and other emerging economies. China is expected to grow due to increased infrastructure and consumer spending. Key challenges for the Asian economies would be geo-political issues, territorial disputes, political transitions, US interest rate hike and protectionist policies. The economy of India is expected to slow down with the currency reforms.

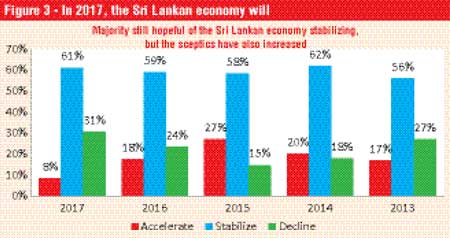

Likewise, both the Asian Development Bank and the World Bank expect a slight increase in Sri Lanka’s real GDP growth rate. The ADB expects the economy to grow by 5.5% this year (up from 5% in the previous year) and the World Bank expects the economy to grow by 5% (up from 4.8% in the previous year). World Bank expects Sri Lanka’s GDP growth to remain unchanged in 2016 and grow marginally over 5% in 2017 and beyond driven by public and private investment, tourism and reduced negative impact on growth from commodity imports. The impact of past currency depreciation and the increase in the VAT rate is expected to increase inflation in 2017 despite downward pressure from low international commodity prices. ADB lowered growth forecast of Sri Lanka to 5.5% in 2017 because of tight monetary and fiscal policies.

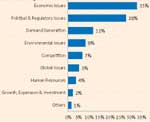

A total of 47% of the CEOs perceive political, legal and governance area to contribute to more challenges. This is closely followed by economic policies with 44%. Less cited primary challenges were international factors or the volatilities of the global economy that are likely to impact the Sri Lankan economy, the cost of living due to increased taxes and human capital issues ranging from difficulty to find and retain skilled workers.

A total of 47% of the CEOs perceive political, legal and governance area to contribute to more challenges. This is closely followed by economic policies with 44%. Less cited primary challenges were international factors or the volatilities of the global economy that are likely to impact the Sri Lankan economy, the cost of living due to increased taxes and human capital issues ranging from difficulty to find and retain skilled workers.

They key issues under political, legal and governance were concerns on policy consistency and effective implementation of policy decisions. According to MTI Research, several experts and economists have emphasised the importance of having consistent and coherent policies. Especially as mentioned by ambassadors of USA and China, having consistent investment policies is vital to attract US and Chinese investments. Equal amount of concern is shared between political stability of the coalition government and attracting Foreign Direct Investments and building investor confidence. Less frequently cited concerns were, government having a clear direction and effective decision making, fight against corruption and ensuring good governance, etc.

A closer look at the composition of responses citing economic policies as a challenge revealed that the depreciation of the Sri Lankan currency, increased taxes due to fiscal policy reforms, high interest rates, need to improve net trade were considered as the most significant issues among Sri Lankan business leaders. Less frequently cited issues cover ensuring economic stability and growth, managing national debt, stability of monetary policy, etc.

Exchange rate: Sri Lankan Rupee (LKR) was highly volatile during the year of 2016. It started at the Rs. 144 range and ended Rs. 150 per $ 1 at the end of the year, leading to 4% depreciation.

Interest rates: All the policy interest rates were increased by 1% (standing deposit facility rate 6%-7% and standing lending facility rate 7.5%-8.5%). Prime lending rates of commercial banks increased by 4%, from 7.5% to 11.52%.

Tax revisions: With the budget proposal for 2017, the Government has increased several taxes. Few revisions are mentioned below. Corporate income tax rate is proposed to be revised to create a three tier structure of 14%, 28% and 40%, Income tax rate of 10% currently applicable on funds, dividends, treasury bills and bonds will be increased to 14%, Withholding Tax (WHT) on interest income will be increased to 5% from the present level, Capital Gain Tax will be introduced with effect from 1 April at a rate of 10%, etc.

Despite performing below expectations in 2016, 45% of the surveyed chief executives are optimistic on achieving better performances in 2017. This is an improvement from last year where only 38% were expecting higher growth. The number of CEOs who expect to grow at a same level has reduced from 45% in 2016 to 41% in 2017. Only 13% CEOs are expecting a lower growth rate as oppose to 18% last year. Despite the economic, monetary and fiscal challenges, increasing confidence on world economic recovery and growth opportunities may have been the reason for better expectations than the previous year.

Despite performing below expectations in 2016, 45% of the surveyed chief executives are optimistic on achieving better performances in 2017. This is an improvement from last year where only 38% were expecting higher growth. The number of CEOs who expect to grow at a same level has reduced from 45% in 2016 to 41% in 2017. Only 13% CEOs are expecting a lower growth rate as oppose to 18% last year. Despite the economic, monetary and fiscal challenges, increasing confidence on world economic recovery and growth opportunities may have been the reason for better expectations than the previous year.

In the same vein as the previous year’s results, two-thirds of the surveyed CEOs believe that their organisations’ success in 2017 will be primarily affected by factors external to their business.

In contrast, only 34% of respondents believe that the problems lie either within their organisations or within their span of control.

Main external challenges the CEOs have identified are related to the economy. Such as devaluation of Sri Lankan rupee, rising interest rates, fiscal policy and tax reforms etc. Hence the key challenges for the Sri Lankan economy and businesses are more or less the same. Second most significant issues are, political and regulatory issues, which cover policy inconsistency and implementation, political stability and rules and regulations. External demand generation challenges mainly cover the low disposable income and purchasing power of consumers.

Main external challenges the CEOs have identified are related to the economy. Such as devaluation of Sri Lankan rupee, rising interest rates, fiscal policy and tax reforms etc. Hence the key challenges for the Sri Lankan economy and businesses are more or less the same. Second most significant issues are, political and regulatory issues, which cover policy inconsistency and implementation, political stability and rules and regulations. External demand generation challenges mainly cover the low disposable income and purchasing power of consumers.

Environmental issues have pointed out the threat of facing a severe drought in 2017, which can especially affect agriculture and plantation industries. Other less frequently cited issues cover, competition from both local and foreign companies, global protectionist schemes and crisis in tea importing countries, difficulty to find and retain talent, etc.

Although less mentioned, the internal factors were majorly comprised of concerns towards being able to successfully pursue expansion strategies or attract further investments, such as expanding to new territories, lack of funding. This was followed by the need to enhance productivity, efficiency and to reduce costs of production with special mentions on improving labour productivity. Finally a few respondents expressed their difficulties in attracting, training and retaining good talent, and the internal difficulties to increase business volumes and attract more customers.

Although less mentioned, the internal factors were majorly comprised of concerns towards being able to successfully pursue expansion strategies or attract further investments, such as expanding to new territories, lack of funding. This was followed by the need to enhance productivity, efficiency and to reduce costs of production with special mentions on improving labour productivity. Finally a few respondents expressed their difficulties in attracting, training and retaining good talent, and the internal difficulties to increase business volumes and attract more customers.

2017 will be an interesting and challenging year for business leaders, considering uncertainties and volatilities both at home and abroad. Despite majority having performed below expectations in 2016, CEOs enter the New Year with relatively positive expectations for their businesses. However the confidence on the recovery of both global and local economies have not been fully restored. Nation-wide political and economic challenges such as policy inconsistencies, political stability, fiscal and monetary policies are expected to directly impact the businesses making them the key concerns for business leaders. All the Sri Lankan companies and business leaders are encouraged to consider re-strategising and gearing their organisations to overcome the mentioned challenges, to achieve the expected business objectives and results.