Sunday Jul 05, 2026

Sunday Jul 05, 2026

Tuesday, 11 September 2018 00:00 - - {{hitsCtrl.values.hits}}

From left: Ustocktrade LLC Founder and Cainan Foundation Co-Founder Tony Weerasignhe, CIMA Global PresidentSteven Swientozielskyj. Dialog Chief Operating Officer Dr. Rainer Deutschmann, Moderator HNB Chairman Dinesh Weerakkody, Central Bank Governor Dr. Indrajit Coomaraswamy and KPMG in

From left: Ustocktrade LLC Founder and Cainan Foundation Co-Founder Tony Weerasignhe, CIMA Global PresidentSteven Swientozielskyj. Dialog Chief Operating Officer Dr. Rainer Deutschmann, Moderator HNB Chairman Dinesh Weerakkody, Central Bank Governor Dr. Indrajit Coomaraswamy and KPMG in

Sri Lanka Managing Partner Reyaz Mihular

By Divya Thotawatte

Professionals will not fear technology if companies work to proactively reskill employees, thereby giving them the opportunity to increase productivity through greater interpretation and communication of their roles within respective industries.

Delivering the keynote address at the 41st Business Leaders’ Summit organised by the Chartered Institute of Management Accountants (CIMA) recently under the theme ‘From Insight to Impact-Unlocking Opportunities,’ CIMA Global President Steven Swientozielskyj highlighted the changes businesses would have to increasingly grapple with to remain competitive.

The Thought Leadership session was held on 29 August with international speakers and academics deliberating on current and relevant topics such as the future of finance, global trends in transforming business and disruptive business models in Sri Lanka.

The summit featured guest speakers including CIMA Global President Steven Swientozielskyj, Dialog Chief Operating Officer Rainer Deutschmann, N-Able Managing Director and Chief Executive Peter D’Almeida, Xtrategize Technologies Co-Founder and Partner Boonsiri Somchit FCMA CGMA and Innovation Quotient Founder and Managing Director Abdul Cader Irfan.

Swientozielskyj stated, “Accelerating change is the new norm. Within business across the globe, technology is driving that change and is the enabler for disruption we see in many industries.”

“Change provides great opportunities for financial professionals as we move from a role of knowledge collection and production to one of curation, interpretation, and communication. A shift from insight to impact. It requires us, however, to enhance our ‘human skills’ including judgement, emotional intelligence and creativity. To take advantage fully of the opportunities that change will bring we need to be agile-to have a growth mind-set that is committed to lifelong learning and with the ability to overcome obstacles,” he added.

Technology as the game changer

Addressing the topic of the panel ‘Future of Finance,’ Swientozielskyj stated that by 2030, 375 million people might need to switch occupations and learn new skills because technology is changing the game.

“We’re positioning ourselves for the future. The issue for all of us is the relevance for what we do. Things change fast and if we don’t adapt we’ll be left behind. We live in a world that is volatile, things change rapidly and it’s hard to conquer them.”

According to Swientozielskyj, the main drivers of change are globalisation, geopolitics, consumer empowerment, demography and technology. He said that some of the technologies transforming industries include artificial intelligence, autonomous vehicles, big data analytics and cloud, custom manufacturing and 3D printing, robots and drones, social media and platforms and blockchain.

“The impact of these changes is increasing complexity. The current focus of finance is in the rational area and future finance skills must move to the areas of complexity and chaos,” he said.

Swientozielskyj explained the implication of technology on future of finance. He said that work activities like managing others, applying expertise, stakeholder interactions, unpredictable physical work, data collection, data processing and predictable physical work were at risk from automation.

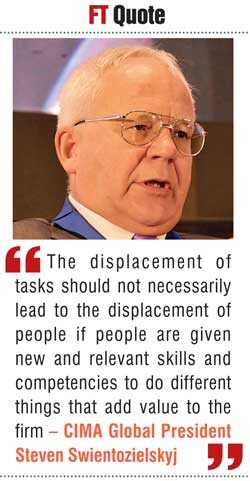

“Technology will take over, things will change. That trend cannot be stopped. If you try to stop that, your organisation, or professional career will be ruined. The displacement of tasks should not necessarily lead to the displacement of people if people are given new and relevant skills and competencies to do different things that add value to the firm,” he noted, stressing on the importance of reskilling people, especially in human-machine hybrid activities as a solution.

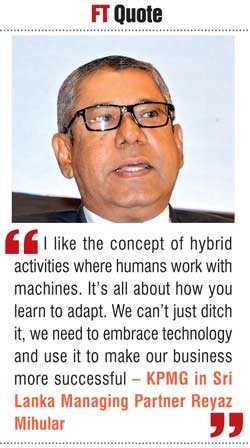

KPMG in Sri Lanka Managing Partner Reyaz Mihular stated that human resource is still necessary to control technology, “Machines don’t comprehend morals or ethics so you need humans to control them. For example, if you told a machine that you want peace and quiet, it would probably kill everyone in the room. I like the concept of hybrid activities where humans work with machines. It’s all about how you learn to adapt. We can’t just ditch it, we need to embrace technology and use it to make our business more successful,” he elaborated.

Ustocktrade LLC Founder and Cainan Foundation Co-Founder Tony Weerasinghe spoke on how every sector has changed with globalisation and how even education is dominated by Internet of Things (IOT) worldwide.

Central Bank Governor Dr. Indrajit Coomaraswamy elaborated on how the banking sector in Sri Lanka is undergoing change due to the digitalisation of the world. “The impact of the technology can’t be denied. By large our banking sector is now digitalised. Financial services sector is a lifeline in the economy and financial intermediation is a critical determinant of the competitiveness of the economy. Central Bank is constantly looking at reducing comebacks for financial intermediation. The challenge for the Central Bank is to balance and embrace the technology progress without destabilising the economy.”

“Technologies is inherently disruptive. But how does one embrace the benefit that comes with the disruption without the whole system being failed. That’s the constant challenge that we face and that’s the balance we are trying to strive,” he added.

Disruptive business models

Linear Squared Founder Sankha Muthu-Poruthotage said that most people understand disruption in hindsight. “Only a very few people understand disruption in foresight and that’s the first thing we need to understand. Our mind-set being open to failure is disruption.”

“As a data scientist I try to see a bigger impact on this. A common trait that I see in disruptive models is sharing. Sharing is a part of  disruption. Sharing your house is disruptive. Sharing your experience, like Trip Advisor, is disruptive. Another feature of disruptive business models is getting customers do work for you. The best example, a company that makes customers work really hard for them and is the largest furniture company in the world, is Ikea. I think these are recurring features of disruptive models,” he explained.

disruption. Sharing your house is disruptive. Sharing your experience, like Trip Advisor, is disruptive. Another feature of disruptive business models is getting customers do work for you. The best example, a company that makes customers work really hard for them and is the largest furniture company in the world, is Ikea. I think these are recurring features of disruptive models,” he explained.

Nations Trust Bank Chief Operating Officer and Senior Executive Vice President Tilak Piyadigama also spoke on how creating a platform is essential for disruptive business models. He said that Trip Advisor was a good example of a disruptive business model in the leisure and hotel sector. Piyadigama noted that it had simply established a platform and that a platform is nothing but getting people together to interact seriously.

“The reviews in Trip Advisor guarantee that you would have a pleasant experience. All that put together, the consumer as well as the producer and the service is connected and it provides a better customer experience. This wouldn’t have been possible if there wasn’t a platform and I think platforms are disruptive,” he elaborated. Iron One Technologies Chairman Lakmini Wijesundera said that one should connect technology innovation and finance for disruption to take place, “When it comes to business model disruption, we always talk about digitalisation. Digital means IT, and technology is coming to play because of the speed at which we operate as we are challenged by IT and technology. The disruption can actually happen if we can create an impact, and the impact can actually happen by reaching larger audiences. That’s where finance people come in; they can bridge technology innovation along with finance and take it to the markets.”

Innovation for incumbents

N-Able Managing Director and Chief Executive Peter D’Almeida gave his ideas on how large companies could try to innovate without being stuck in their traditional business models.

According to him, if models of incumbent businesses are carefully operated with innovation, there is still a possibility of obtaining profits from these businesses.

He stated that the incumbents don’t respond when the disruptors are coming into the market due to the pre-model which has made the incumbents so comfortable in what they’re doing, that they miss the disruption that is taking place at the low-end of the market. D’Almeida also emphasised on the fact that incumbent businesses can improve if they learn from the disruptive business models.

“We engage with our customers, we work on the process, but essentially we have to respond to disruption. Therefore we have to start a separate practice like, one based on data or quality analytics, etc.”

“Then comes the accounting problem and you aggregate over this and look at some metrics and say that the innovative model isn’t making profits. Even though within companies, you break it up, you still face challenges to get the necessary investment because you’re looking at the wrong set of metrics of the income because that’s what you’re used to. So yes, big businesses can start innovation but we will face challenges and we’ll have to start things differently,” he stated.

Pix by Lasantha Kumara