Wednesday Jun 10, 2026

Wednesday Jun 10, 2026

Monday, 6 July 2015 00:00 - - {{hitsCtrl.values.hits}}

Former Central Bank Governor Ajith Nivard Cabraal

Former Central Bank Governor Ajith Nivard Cabraal

An alleged draft of the Committee on Public Enterprises (COPE) Report on the bond scam of 27 February, as well as the comments made by one or two members of that COPE Investigation Subcommittee, has supposedly attempted to draw a nexus between the former Central Bank Governor Ajith Nivard Cabraal and the bond scam, by stating that Cabraal’s sister, Siromi Wickramasinghe, was on the board of Perpetual Treasuries Ltd., the primary dealer company owned and controlled by Governor Arjuna Mahendran’s son-in-law, that made the controversial bids for the Treasury bonds on 27 February 2015.

Based upon such a premise, the draft report is also alleged to have observed that “there could have been a conflict of interest in the transactions carried out by Perpetual Treasuries Ltd. at that time also” thereby indirectly suggesting that scams in the nature of the February 2015 bond scam may have taken place during the tenure of office of the former Governor as well.

In this regard, the factual position is as follows: Siromi Wickramasinghe, attorney at law, former Chairperson of the HDFC Bank and former Deputy General Manager of the Hatton National Bank, was never a member of the Board of Directors of Perpetual Treasuries Ltd. (PTL), and had not been involved at all in any transaction or bid that had been made by that company. However, the innocent confusion or deliberate misrepresentation has probably arisen because Ms. Wickramasinghe had served as a member of the Board of Directors of Perpetual Capital Holdings Ltd., which is the owning company of PTL and the other companies within the Group.

Further, while it is a fact that Siromi Wickramasinghe had been on the Board from 23 December 2013 until 9 March 2015, she did not own any shares of the company at any time.

Absence of connivance

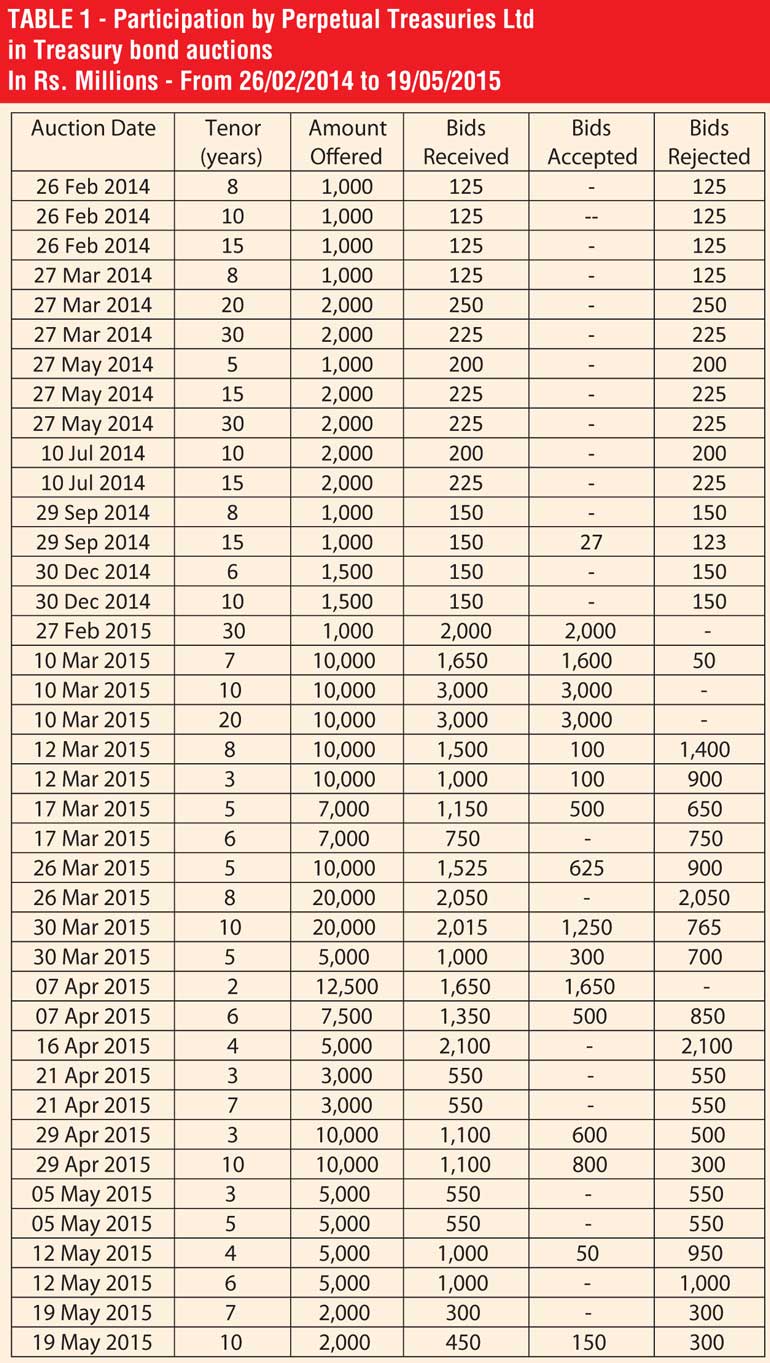

In addition, most importantly, as per a document that has been reportedly submitted at the COPE investigation, other than in just one instance where PTL was allotted Rs. 27 million out of bids for Rs. 150 million in a Treasury bond auction on 29 September 2014, all other bids submitted by PTL during the time Ajith Nivard Cabraal served as the Governor, have been totally rejected by the PDD of the Central Bank.

This fact, although based on the competitiveness of the bids, this outcome undeniably supports the position that there would not have been any connivance between PTL and the then Governor, through his sister or otherwise. (See Table 1).

The table, however, shows that after Governor Mahendran assumed office in late-January 2015, PTL had become highly active, and had been successful in its unusually aggressive bids, commencing with the controversial bond of 27 February 2015. Hence the observation that there may have been a conflict of interest in the transactions carried out by PTL during the tenure of office of Cabraal as per the alleged draft COPE Report is not tenable, and has no basis or foundation whatsoever.

Nevertheless, since a ‘conflict of interest’, which is a very critical issue, has now been validly raised in the open, it may be relevant for the public in this country to also consider the following instances of possible ‘conflicts of interest’ that could have arisen in relation to this bond scam which has shaken the economy as well as damaged the credibility of the Central Bank and the Government at its very roots.

Sudden fund requirement

Arjuna Mahendran, a non-citizen of Sri Lanka, was invited to Sri Lanka and appointed as the Governor of the Central Bank by Prime Minister Ranil Wickremesinghe notwithstanding vociferous protests by several Ministers.

However, according to media reports, those Ministers had agreed not to pursue their opposition to the appointment on the assurance given by the Prime Minister that he would take personal responsibility for Mahendran’s actions.

According to reports and statements made by various parties, a “sudden” fund requirement had surfaced at a Cabinet Subcommittee just a day or two before the fateful bond issue, at which, as supposedly admitted by Governor Mahendran, the Chairman of the United National Party (UNP), Malik Samarawickrema, who is a very close confidant of Ranil Wickremesinghe, had also attended. It was at this meeting that the so-called “decision” to increase the bond issue the next day or the day after, from Rs. 1 billion to Rs. 10 billion was made.

As per media reports, at the COPE investigations, Mahendran had admitted that it was Ranil Wickremesinghe who had ordered him to suddenly change the public debt issue system from the hybrid “auction cum direct placement” to an “auction only” system.

This change provided an opportunity for Mahendran to override the recommendations of the PDD, and instruct the PDD officials to accept bids at substantially higher rates, flouting the all-important objective of the Public Debt Department that the Central Bank raises funds for the Government at the least possible cost.

Mahendran physically went to the PDD auction room twice and personally ensured that the bonds be issued in the manner as directed, notwithstanding the huge price differential in the bond bids or the massive loss that such action was going to inflict on the government finances.

So far, the loss due to the interest increase has exceeded Rs. 55 billion, according to analysts. In addition, by issuing the bonds at a deep discount, the Government had suffered a loss of nearly Rs. 291 million per each bond of a face value of Rs. 1,000 million, in respect of the vast majority of the bonds issued on that day, the bulk of which was issued to PTL, owned by Governor Mahendran’s son-in-law.

PM’s denial

Notwithstanding the mounting, massive losses, as the Minister who is responsible for the Central Bank, Ranil Wickremesinghe has been completely silent on the losses, and has not taken any measures whatsoever to mitigate the losses or address the underlying aberration that was caused by the arbitrary increase of the interest rate through the reckless action of Governor Mahendran.

In fact, Ranil Wickremesinghe has been in an incredible sense of denial, leading to the suspicion that he is keen to whitewash the incident by giving the impression that no untoward incident has taken place.

A critical factor in the bond scam was the financial support of Rs. 13 billion provided by the Bank of Ceylon in a matter of a few hours to PTL. Officials of the Bank of Ceylon are supposed to have also informed COPE that this was the first instance where the Bank of Ceylon had ever made a bid on behalf of another primary dealer.

In that context, it could be reasonably concluded that the appointment of a person who is closely connected to the UNP as the Chairman of the Bank would have been a vital factor that ensured that the staggering facility to a fledgling primary dealer company was granted, without following the usual credit procedures which surround the approval of such an enormous funding facility.

Needless to say, it was the facilities provided by the Bank of Ceylon that enabled the scam to be carried out on this magnitude.

In mid-March 2015, a complaint was submitted by two MPs to the Commission to Investigate Allegations of Bribery or Corruption (CIABOC), stating that Governor Mahendran had violated the provisions of the Bribery Act.

In that regard, many persons had been summoned to give evidence, and according to certain knowledgeable sources, this inquiry has been proceeding satisfactorily. There has however been some speculation in the media and social media that a powerful person has thwarted the filing of legal action against Mahendran by the CIACOC, by persuading one of the commission members to prematurely resign, thereby creating a legal impediment towards the serving of an indictment under the CIABOC Act against Mahendran.

Thereafter, on or about 17 March 2015, possibly to provide an official cover to an investigation and avoid an investigation over which he may not have any control, a panel of three UNP lawyers was appointed by the PM to report on the controversial bond issue.

From the time this panel was appointed, the general public and media expressed their deep suspicion about this attempted cover-up and many indicated grave doubts of any useful purpose being served other than to whitewash the entire sordid episode.

Misdirecting public attention

However, the PM insisted on this course of action and made the appointments and the panel duly obliged by pronouncing that the Governor was not “directly involved” in the scam. The report however, perhaps cunningly, raised doubts about the PDD’s universally-accepted ‘direct placements’ methodology of issuing Treasury bonds by shrewdly referring to such placements as ‘private placements’, and by doing so, cast aspersions on the bond issues from 2012 to 2014. That was probably done in order that the focus would be shifted elsewhere, thereby providing a convenient opportunity for the Government to claim that all was well with the 27 February 2015 bond, but not so, in the past bond issues.

That ‘private placements’ suggestion therefore seems to be a well-planned and carefully orchestrated ploy to shift the attention of the public in a new direction.

In the meantime, around 27 March 2015, a few so-called ‘good governance activists’, who have been generally sympathetic to the UNP, filed a Fundamental Rights Petition in the Supreme Court of Sri Lanka, supported by two Counsel who have also been closely associated with UNP leaders and activities.

To the outside world the ‘public interest’ petition seemed to be a petition to take the Governor and all others who were involved in that deal, to task. However, upon close examination of the pleas contained in the petition, it is clear that the prayers sought by the petitioners lacked penetration, depth or a desire to obtain “justice” or to punish the wrongdoers.

In fact, as reported in the Daily FT of 30 March 2015, the main prayer of the petition was “for a declaration that the Governor, Deputy Governor and Chairman of the Treasury Bond Tender Committee, and the Superintendent of Public Debt have not discharged their duties in a manner that is necessary for the preservation of public trust; The Monetary Board to carry out an independent inquiry by a competent panel of professionals well-versed in the rules, systems, procedures and processes applicable to the public debt management under the supervision of Court and to report thereon; and direct the Monetary Board and other associated Respondents, in consultation with stakeholders, to formulate new systems, processes, rules and regulatory frameworks which assure transparency and best governance practices are in place in respect of future public debt issuance.”

Hence, as pointed out by a special correspondent in an analysis published in the Daily FT of 1 June 2015, the rejection of this petition on 13 May 2015 by the Supreme Court meant in practical terms, “That the case will not be allowed to proceed to a full hearing because, strictly speaking, procedures of the Central Bank had not been transgressed and no law has been violated by any of the respondents. The judges seem to have taken a strictly legalistic view and decided to reject the petition, ruling out any further consideration. The ruling does not mean that the actions taken by the respondents in this instance were fair and above board, or that the Treasury did not incur unnecessarily higher interest costs. What it means is that, in the opinion of the judges, there was no legal basis for the granting of leave to proceed to a hearing.”

In the above background, the subsequent claims that are now being made by certain MPs that the Supreme Court has found Governor Mahendran “not guilty”, seems to be the canard that has been cleverly designed and constructed to mislead the public through the tacit suggestion that the Supreme Court petition was to decide on the guilt or otherwise of the Governor.

Lawyers Report

In mid-May 2015, the three-member Lawyers Report was tabled in Parliament on 3 June 2015 and based on such report, the Government claimed that Mahendran had been “cleared” of all charges. At the same time, the Prime Minister went on to accuse Cabraal, the former Governor, of personally directing the issue of Treasury bonds to the value of Rs. 2.7 trillion during the years 2012 to 2014 via private deals to Cabraal’s friends as well as “cronies” of the former regime.

The accusation against the former Governor resulted in the former Governor responding strongly in denying the allegations, while pointing out the irregularities in the 27 February bond issue, in a detailed analysis. Cabraal also invited Ranil Wickremesinghe to a public TV debate on the bond scam, but Ranil Wickremesinghe has so far not responded to that challenge.

On 19 May 2015, a 13-member subcommittee of COPE was appointed to investigate the scam, from its many angles. However, when the COPE investigations were nearing completion, it was reported in the media that the Prime Minister was getting agitated and was working furiously towards having Parliament dissolved, so the COPE report would not see the light of day.

There were also several reportedly frantic efforts by several parliamentarians to delay the report. Finally, when it was imminent that the Interim COPE Report was about to be presented to the Speaker on 26 June 2015, Parliament was dissolved, resulting in the report being suppressed.

The above-mentioned instances of “nexus” and the possible “conflicts of interest are clearly suggestive of a powerful hidden hand that has probably been in active operation in the planning, implementation and the cover-up of this massive scam.

Needless to say, this scam has almost irreparably damaged the credibility of the Central Bank and the Government while causing losses in interest in the amount of over Rs. 55 billion so far, although earning a minimum of Rs.2 billion to those involved, at the taxpayers’ expense. Hence, in order to restore at least some form of credibility and to bring the perpetrators and the mastermind of this bond scam to justice, a wide and credible investigation must be launched once again to unearth the truth and expose these “suit-attired” criminals.

Unlike in earlier allegations of bribery and corruption against various leaders of the previous regime where the allegations were not supported by hard facts, definite figures or well-documented evidence, in this instance there is clear evidence as well as credible leads that would support an extensive and methodical investigation.

Hence, in the interest of the country and the economy, a wide investigation must be launched so that the truth is revealed, and the mastermind and other perpetrators of this largest ever crime against the economy of Sri Lanka, are brought to justice, however highly placed they may be.