Saturday May 30, 2026

Saturday May 30, 2026

Monday, 1 June 2015 00:00 - - {{hitsCtrl.values.hits}}

Following is a statement issued by former Minister of Foreign Affairs Prof. G.L. Pieris and former Minister of Education Bandula Gunawardena on the Government’s International Bond Issuance on 29 May

The Finance Minister and the Governor have claimed that the 10-year International Sovereign Bond of $ 650 million issued on 29 May at an interest rate of 6.125%, is a great success. They have even gone to the extent of making an unprofessional and comical exercise of combining the results of this 10-year International Sovereign Bond with two short-term 13 and 35 month locally-floated Sri Lanka Development Bonds to portray a lower interest rate of around 5.2% and a higher issue amount of $ 989 million. That has been obviously done to mislead the public in order to cover-up the Government’s woeful inadequacies.

While the issuance of the international sovereign bond at a very high interest rate is a massive loss to the country, it is also a huge loss of credibility for Prime Minister Ranil Wickremesinghe, who in 2007, demonstrated in front of HSBC and threatened to cancel its banking license when he assumes power, if the bank were to participate in a bond issue at that time, on behalf of the Government.

Making an abrupt U-turn, Prime Minister Wickremesinghe is now following the policy of the Mahinda Rajapaksa administration which he and his Finance Minister so bitterly criticised for nine years, by issuing the present Sovereign Bond, although the Bond has been the worst-ever Bond issued by Sri Lanka, signifying a huge debacle for his struggling, incompetent and corrupt administration.

It is clear that continuously declining external reserves, difficulty of servicing newly-added recurrent expenses in the Government Budget, declining Government revenues, mounting pressure on the rupee, and limited availability of rupee funds and foreign exchange to meet local and foreign liabilities, has led this Government to a desperate situation to issue Sovereign Bonds in the international market, at any cost.

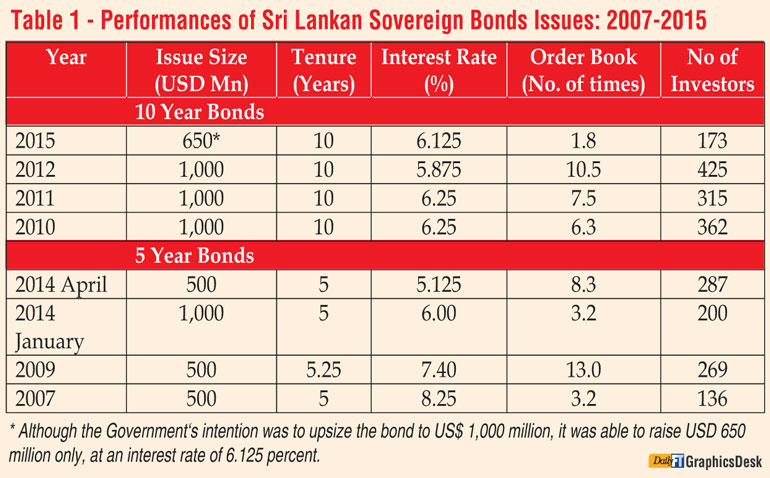

However, although the Government intended to issue $ 1,000 million on a 10-year tenor, it had been able to mobilise only $ 650 million even at the high interest rate of 6.125%. The order book was also for $ 1,800 million or 1.8 times the intended issue size under the initial price guidance of 6.375% interest rate, with the participation of 173 investors only. This pathetic outcome of high interest rate, inability to raise the intended volume, and the limited number of investors reflect the serious concerns among global investors about the current Government’s abilities and policies.

The Government of Sri Lanka first entered the international capital market while the terrorist war was in progress in 2007, and since then, had become a frequent Sovereign Bond issuer. The previous Government’s record with Sovereign Bond issues was also extremely impressive, and interest rates were on a clear down-ward path with an extended yield curve up to 10 years. The number of investors too, had rapidly increased with each Sovereign Bond, showing improvements in comparison to each previous issue, as shown in Table 1 below, with the 2015 issue being the glaring exception.

A similar situation was observed in the latest Sri Lanka Development Bonds issued to the commercial banks operating in the local market earlier this week, as well. In that case, the acute lack of appetite for longer-term SLDBs resulted in the Government having to mainly issue 13-month short-term Bonds of $ 330 million, and a very small quantum of 35-month Bonds of just $ 9 million. This outcome also confirms the serious lack of investor confidence for longer tenure Sri Lankan Bonds, even in the local market.

From the above, it is patently clear that international investors are now openly displaying intense anxiety due to the haphazard and unprofessional policies implemented by the present Government. They also appear to be deeply concerned about the instances of massive corruption that have been practiced recently including the unprecedented Treasury Bond scam and the major Customs scam, both of which are pointing towards top officials of the present administration.

Notwithstanding the above, the Finance Minister and the Governor have unashamedly attempted to showcase these failed Bond issues as successes by bluffing their way through. However, the acute loss of confidence in the Sri Lankan economy is now becoming more and more obvious, and no amount of white-washing is likely to be able to arrest the rapid erosion of the country’s economic goodwill.