Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 6 October 2020 01:30 - - {{hitsCtrl.values.hits}}

By Dr. Nisha Arunatilake

The world economy is predicted to contract by -4.9% in 2020 (International Monetary Fund, 2020). The performance of individual countries during the COVID-19 pandemic varies widely. A variety of factors, including severity of the pandemic, stringency of containment efforts, and the connection of economies with other affected countries determine the performance of individual economies. Disasters such as the COVID-19 can impede development in countries; while it is difficult to avoid being affected by disasters, being prepared can reduce the costs, and quicken the recovery.

The world economy is predicted to contract by -4.9% in 2020 (International Monetary Fund, 2020). The performance of individual countries during the COVID-19 pandemic varies widely. A variety of factors, including severity of the pandemic, stringency of containment efforts, and the connection of economies with other affected countries determine the performance of individual economies. Disasters such as the COVID-19 can impede development in countries; while it is difficult to avoid being affected by disasters, being prepared can reduce the costs, and quicken the recovery.

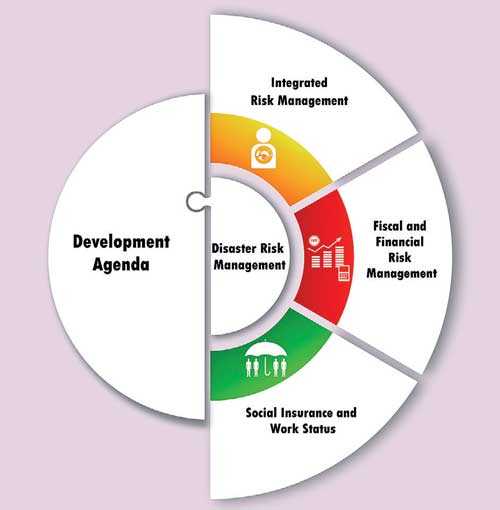

Countries can prepare for disasters in a variety of ways. Following the World Development Report 2014 recommendations, this blog concentrates on disaster preparedness along: a) integrated risk management; b) fiscal and financial risk management; and c) social insurance and work status.

Integrated risk management (IRM) involves strengthening the overall capacity of a country to manage all types of risks, rather than specific ones. IRM is both efficient and cost-effective. It helps countries prepare for different types of disasters using the same process, by providing a framework for exploiting synergies in the management of risks and balancing different trade-offs across risks.

For example, building capacity to provide relief to people during a disaster can be useful during different types of disasters. IRM also helps prepare for less frequent, but high impact disasters, such as pandemics, which receive less policy attention. An IRM system also takes into account both low probability high impact risks (e.g. tsunamis and pandemics) as well as high probability low impact risks (e.g. floods and droughts).

Fiscal and financial risk management is important to improve a country’s resilience to disasters. The ability to respond to a disaster effectively depends on its available fiscal space. Evidence shows that countries with sufficient funds to cushion the impacts of an adverse shock can minimise the costs of disasters, and facilitate a faster recovery. This requires increasing spending when economies are down, and saving during economic booms. Such counter-cyclical spending is possible only when countries plan to manage their finances keeping a long-term perspective.

Social protection and social insurance provide safeguards against poverty during adverse shocks and boosts recovery of economic activities by maintaining aggregate demand. The coverage of protection and the adequacy of benefits are important to improve the effectiveness of social protection. Social protection funds that are independent of governments and employers are more resilient, as they are not affected by economic downturns during disasters.

Building Sri Lanka’s resilience

Sri Lanka is highly vulnerable to different types of disasters. Preparedness can reduce the resultant socio-economic costs.

Over time, Sri Lanka has put in place a variety of institutions and mechanisms to respond to disasters. However, there is no IRM process in the country. For example, the epidemiology unit at the Ministry of Health is experienced in handling public health risks and has managed to contain COVID-19 successfully, but its functions are limited to the health sector.

Since the 2004 tsunami, Sri Lanka has followed international frameworks to improve its disaster preparedness through legal and institutional reforms and capacity building. However, the current framework is highly focussed on addressing hydro-meteorological disasters. As such, the relief activities of COVID-19 were coordinated by a task force under the Presidential Secretariat. The involvement of a high-level office has certainly improved the response effectiveness in the short-term; in the long term though, it is important to build the capacity of existing institutions to handle such disasters.

The importance of long-term fiscal discipline in Sri Lanka was exemplified by the COVID-19 pandemic. A stronger financial position would have enabled more relief to households and businesses for a faster recovery, including more investments to boost growth. Many countries increase public investments to create jobs and boost economic activity. For example, in the aftermath of the 2008 global financial crisis (GFC), the Chinese Government rolled out a massive investment plan to stimulate the economy, mainly focussed on improving infrastructure. This facilitated a quicker recovery in comparison to many other countries.

The COVID-19 experience highlights the need for stronger social protection coverage in Sri Lanka. The inadequate coverage of existing programs has hampered the effective channelling of relief to the most affected individuals. A universal program can overcome some of these issues. Such a programme can also be more efficient and flexible, as the administrative costs incurred will be minimised and the Government will have better information to target different types of populations in providing relief.

At present, Sri Lanka protects the incomes of formal sector workers by protecting jobs. Companies are compelled to pay their workers regardless of whether they work or not. Continuing to retain a full workforce during financially difficult times can be a challenge to many companies, especially amid severe reductions in business activities and revenue. Schemes that are not linked to the employer to provide unemployment insurance, can help the employers survive, while providing relief to workers.

The COVID-19 pandemic presents unprecedented economic and social challenges to countries across the world. Sri Lanka has been largely successful in containing the spread of the disease and maintaining low casualty levels. The recovery from similar pandemics in the future can be expedited if the country is better prepared to respond to disasters.

Given that Sri Lanka will remain highly vulnerable to the growing threat of pandemics like COVID-19 and other forms of disasters, improving its disaster preparedness can mitigate the human and economic costs arising from them.

(This blog is based on IPS’ forthcoming ‘Sri-Lanka: State of the Economy 2020’ report on ‘Pandemics and Disruptions: Reviving Sri Lanka’s Economy COVID-19 and Beyond’.)

(Nisha Arunatilake is the Director of Research at IPS. She heads the Labour, Employment and Human Resource Development research unit. Her research interests include labour market analysis, education and skill development, migration and development and health economics. She holds a BSc in Computer Science and Mathematics with summa cum laude from the University of the South, USA and an MA and PhD in Economics from Duke University, USA. Talk with Nisha via [email protected].)