Saturday Jul 18, 2026

Saturday Jul 18, 2026

Saturday, 5 December 2020 00:05 - - {{hitsCtrl.values.hits}}

Indian Prime Minister Narendra Modi (left) and Chinese President Xi Jinping. India and China see a chance to deepen their geopolitical influence in cash-strapped and increasingly vulnerable Sri Lanka and the Maldives, both strategically located in the Indian Ocean – Source photos by Reuters

Xi (left) waves while standing next to Sri Lanka’s then President Mahinda Rajapaksa during an official welcoming ceremony at Bandaranaike International Airport in Katunayake, Sri Lanka September 2014 – Reuters

Maldivian President Ibrahim Mohamed Solih (left) and Modi smile after delivering a joint press statement in New Delhi in December 2018 – Getty Images

By Marwaan Macan-Markar

asia.nikkei.com: Sri Lanka’s Navy scours the island nation’s northern waters in search of Indian smugglers hauling boatloads of turmeric, a staple spice used widely in South Asian cooking. The ultranationalist Government of President Gotabaya Rajapaksa this year added the yellow seasoning to a list of banned imports in a desperate bid to prevent an outflow of precious US dollars.

asia.nikkei.com: Sri Lanka’s Navy scours the island nation’s northern waters in search of Indian smugglers hauling boatloads of turmeric, a staple spice used widely in South Asian cooking. The ultranationalist Government of President Gotabaya Rajapaksa this year added the yellow seasoning to a list of banned imports in a desperate bid to prevent an outflow of precious US dollars.

Meanwhile, the Maldives, to Sri Lanka’s southwest, has imposed limits on the use of dollars by locals to settle their monthly debit and credit card bills. The Bank of Maldives, the largest commercial bank in the region’s smallest country, in September set a monthly limit of $ 250 for each card, widely used by small businesses in the archipelago to pay for imports.

The commodity and currency crackdowns by the two Indian Ocean countries have a common thread spotlighting their shared need to shore up fast depleting foreign – overwhelmingly dollar – reserves. The cash crunch is forcing both governments to seek for financial lifelines to settle mounting international debts.

And that vulnerability is providing a fresh opportunity for China and India to deepen their influence in the nations as they engage in a growing contest to gain the upper hand in the strategic Indian Ocean. Though part of ongoing broader economic, financial and geopolitical ambitions on display by the world’s two most populous countries, it marks a new stage of engagement in a region where they have already been competing in infrastructure financing for years.

Officials in Sri Lanka and the Maldives are quick to acknowledge how beholden they are to the Asian giants as they struggle to stay solvent in a growing sea of red ink, problems plaguing other indebted countries in the region from Pakistan to Cambodia.

“India has offered a swap arrangement,” Nivard Cabraal, Sri Lanka’s Minister overseeing Money, Capital Markets and State Enterprise, told Nikkei Asia. “We have been in touch with the Chinese Development Bank as part of the options available to Sri Lanka to have inflows coming on a bilateral basis.” The country’s dependency on New Delhi and Beijing has increased after the one-year-old Rajapaksa Government eschewed seeking a bailout from the International Monetary Fund. According to Mohamed Nasheed, the former President of the Maldives, the Government of President Ibrahim Solih is in talks with China for a reprieve from the multimillion-dollar debt owed to Beijing. “It is still being negotiated, but not yet settled,” Nasheed, currently the speaker of parliament, told Nikkei. The Government hopes “the Chinese will delay the repayments by a few years at least,” he said.

India’s debt-relief offer differs from China’s approach. In Sri Lanka, New Delhi provided a $ 400 million currency swap facility this year through the Reserve Bank of India, its central bank, helping to boost the island’s reserves. It has kept the Rajapaksa Government guessing, however, on its other requests – a further $ 1 billion currency swap and a $ 1 billion debt moratorium on loans Sri Lanka owes India. Diplomatic sources in the Sri Lankan capital say that India has an opportunity to leverage the current moment as Sri Lanka’s economy nears default.

China, which styles itself as an “all-weather friend” to Sri Lanka, has pumped in $ 500 million dollars this year out of a $ 1.2 billion syndicated loan it has pledged through the China Development Bank. Sri Lankan authorities have reportedly approached Beijing for a further $ 1.5 billion currency swap.

Not surprisingly, Chinese diplomats in Colombo welcome being the lender of last resort. “The $ 700 million facility agreement is to be finalised between China Development Bank and the Finance Ministry of Sri Lanka,” Luo Chong, the Chinese Embassy’s Spokesperson, told Nikkei, referring to the remainder of the $ 1.2 billion loan. “So, we are positive about the process.”

In the Maldives, conversely, it is India that has been more generous after Solih’s pro-Indian Maldivian Democratic Party defeated former President Abdullah Yameen, who was openly pro-China and anti-India, in a shock election outcome in 2018. New Delhi has steadily injected an estimated more than $ 2 billion through loans, grants, credit lines and currency swaps.

“India has adopted a package approach in which it works on the demand basis of South Asian countries while assisting them in short projects,” said Pankaj Kumar Jha, Professor of Defence and Strategic Studies at New Delhi-based Jindal Global University. “At the same time, [it is] providing grants and aid which can be restructured through deferred payments and the repayment terms have built confidence.”

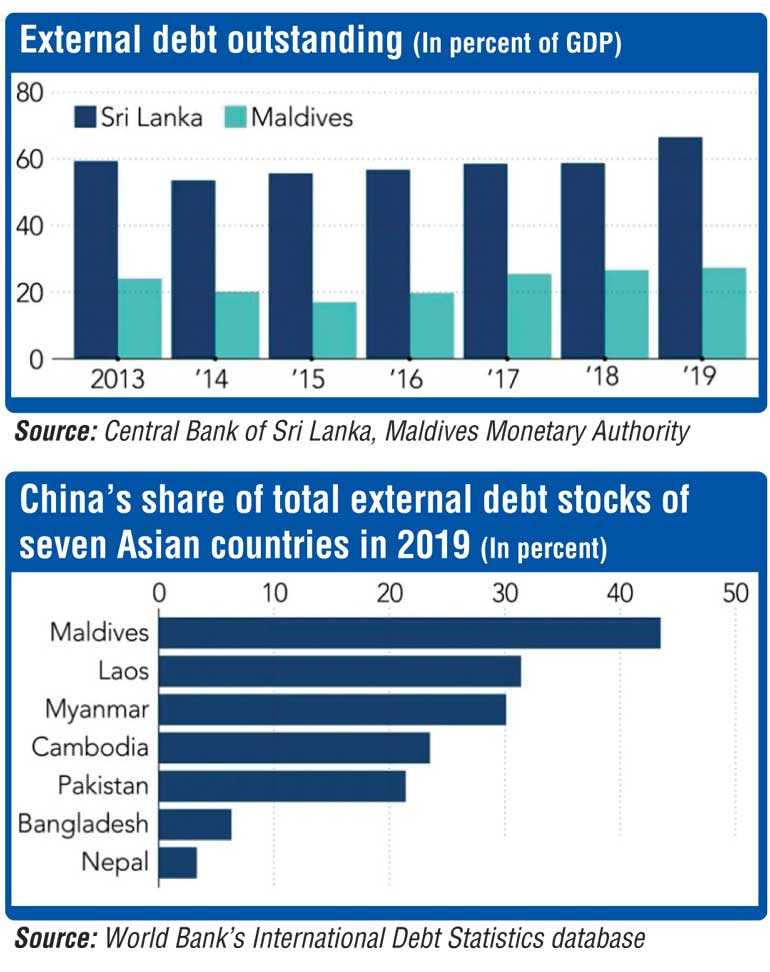

Despite India’s munificence, China still holds the influential hand. The Maldives had to swallow a bitter pill served up by a World Bank report in mid-2020 that ranked it among nine countries facing “debt distress” due to Chinese loans that exceed over 30% of its national obligation – in the Maldives, it is 45%. Consequently, China agreed to slash $ 25 million from the $ 100 million in official debt the Maldives had to settle with it this year. It was a special arrangement under the Group of 20 Debt Service Suspension Initiative, or DSSI, to postpone debt servicing on bilateral loans.

The groundbreaking offer was greeted with relief in the capital Male. “We have received the DSSI for our direct debt obligations from the official bilateral creditors,” a senior official from the President’s office told Nikkei. “The Government of the Maldives has strongly advocated for this to be extended until the end of 2021.”

Recent downgrades by global ratings agencies have compounded the debt crisis for the Maldives and Sri Lanka, leaving little room for them to seek alternative financing in international markets.

In November, Fitch Ratings downgraded the Maldives to a “CCC” rating from the previous “B” rating due to the coronavirus pandemic. It forecast the tourism-dependent economy to contract by 30% and government debt to jump to 110.7% of gross domestic product in 2020.

Two months earlier, Moody’s Investors Service downgraded its rating on Sri Lanka two notches from “B2” to “Caa1” – junk status – saying the pandemic’s economic shock exposed the country to financial risks. “We expect Sri Lanka’s debt burden to increase to 100% of GDP over 2020-21, above the Caa-rated median of 88%,” Moody’s said last week. Fitch immediately followed Moody’s with further bad news, downgrading Sri Lanka’s rating to “CCC” from “B-” after the government presented its 2021 budget to the parliament in November. The “risks to the sovereign’s ability to meet its external-debt servicing obligations have increased,” Fitch said.

Seasoned analysts are not surprised by the severe measures -- such as the imported turmeric ban – that Sri Lanka has imposed to preserve its dwindling dollars. This policy shift is “to tackle a macroeconomic issue of a worsening balance of payments deficit due to [a] fall in foreign receipts from exports, foreign direct investment and tourism,” said Ganeshan Wignaraja, Senior Research Associate at the London-based Overseas Development Institute. It is also for a “longer-term structural issue of inadequate domestic production in agriculture and manufacturing which has led to high import dependence,” he added. The debt picture for Sri Lanka’s $ 88 billion economy confirms an appetite for living on borrowed money. It had $ 50.8 billion in loans by the end of June, the largest slice from international markets that cannot be renegotiated. Bilateral lenders like China account for 10% of the debt, mostly for large infrastructure projects, followed by Japan, previously Sri Lanka’s largest lender.

This year, Sri Lanka had to settle $ 4.2 billion in foreign debt, which included paying off a $ 1 billion sovereign bond in October. Interest payments to service loans were $ 1.4 billion and a further $ 1.8 billion in loans to multilateral and bilateral lenders were settled, according to the finance ministry. From 2021 until 2024, Sri Lanka faces annual foreign debt payments averaging $ 4 billion, with next year’s principal at $ 2.6 billion and estimated interest at $ 1.4 billion. The turn to India and China coincided with Sri Lanka’s diminishing foreign reserves, which have slumped to a three-year low of $ 5.8 billion after the October’s sovereign bond was settled. “We have a situation where we have high annual foreign debt repayments over the next several years,” said Trisha Peries, Head of Economic Research at Frontier Research, a Colombo-based think tank. “If the government doesn’t approach the IMF for funding, Sri Lanka would have to rely more on bilateral lenders who would be able and willing to provide continuous support over the next few years and not just in the short term.”

The foreign debt picture in the $ 5 billion economy of the Maldives is more opaque and characterized by public spats over how much the country owes China. The outspoken Nasheed told Nikkei that the amount is over $ 3 billion. “My figure is from the Parliament Finance Committee; we work from first principals as well,” he said. The Chinese Government disagrees, saying it is closer to $ 1.45 billion.

Experts in the Maldives say the country should consider the financial lifelines to stave off default as a measure of political benevolence. At a time of great difficulty in the Maldives, a willingness on the part of the Chinese Government to intervene is “a big help not to the Government of the Maldives, but to the people,” said Fazeel Najeeb, former Governor of the Maldives Monetary Authority, the Central Bank. “An agreement to negotiate [outstanding loans] is always a matter of goodwill.”

The Maldives’ depleted international reserves of $ 649 million are due to be tapped to meet multiple foreign debt servicing commitments from the fourth quarter of this year through 2022. One loan of $ 142 million has to be settled next year, and a foreign bond of $ 250 million matures in June 2022.

But for both the Maldives and Sri Lanka, there are warning signs over just how far China, with much deeper pockets than India, is willing to go to prevent defaults.

“China has offered debt relief [to cash-strapped countries like Pakistan, Angola and Zambia] that is short term relief and meant to complement the IMF, not replace it,” said Akhil Bery, South Asia Analyst at Eurasia Group. “It was clear that China was not willing to bail out Pakistan, despite their all-weather friendship.”

(Source: https://asia.nikkei.com/Spotlight/Asia-Insight/India-and-China-compete-over-Indian-Ocean-debt-relief-diplomacy)

Workers are seen at a construction site near a China-funded bridge in Male, the capital of the Maldives, in September 2018. The Chinese-language sign says: “Here, we are representing China! Actively promote Chinese technology, Chinese standards, Chinese management – Reuters

Port City Colombo is seen under construction in Colombo, Sri Lanka, in November 2019. Built on land reclaimed from the Indian Ocean and funded with $ 1.4 billion in Chinese investment, the massive business, financial and leisure project managed by China Communications Construction Company lies on 65 million cubic metres of sand spanning 269 hectares – Getty Images