Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 24 January 2023 00:00 - - {{hitsCtrl.values.hits}}

Geneva, Switzerland: A majority of the World Economic Forum’s Community of Chief Economists expect a global recession in 2023, see geopolitical tensions continuing to shape the global economy, and anticipate further monetary tightening in the United States and Europe.

These are the key findings of the Chief Economists Outlook, launched last week at the World Economic Forum Annual Meeting in Davos-Klosters, Switzerland.

Almost two-thirds of chief economists believe a global recession is likely in 2023; of which 18% consider it extremely likely – more than twice as many as in the previous survey conducted in September 2022. A third of respondents consider a global recession to be unlikely this year.

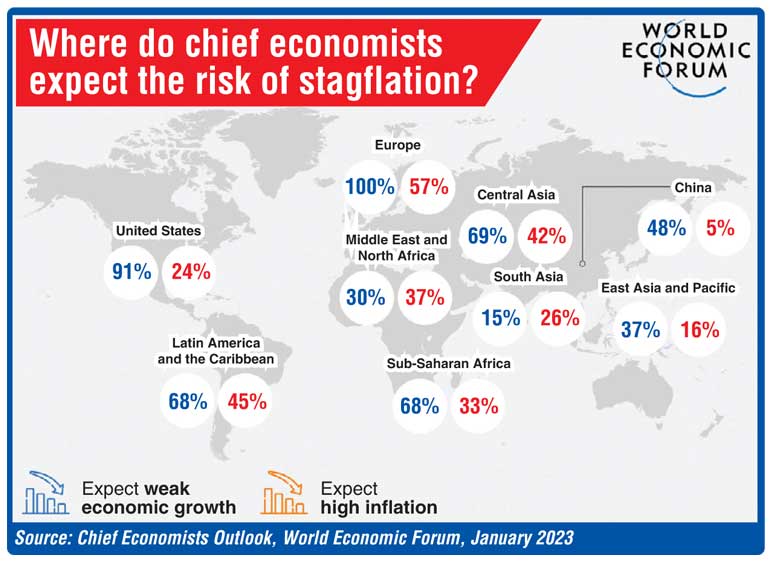

There is, however, a strong consensus that the prospects for growth in 2023 are bleak, especially in Europe and the US. All of the chief economists surveyed expect weak or very weak growth in 2023 in Europe, while 91% expect weak or very weak growth in the US. This marks a deterioration in recent months (at the time of the last survey, the corresponding figures were 86% for Europe and 64% for the US).

In China, expectations of growth are polarised, with respondents almost evenly split between those who expect weak or strong growth. Recent moves to unwind the country’s highly restrictive zero-COVID policy are expected to deliver a boost to growth, but it remains to be seen how disruptive the policy shift will be, particularly in terms of its health impacts.

On inflation, the chief economists see significant variation across regions, with the proportion expecting high inflation in 2023, ranging from just 5% for China to 57% for Europe. Following a year of sharp and coordinated central bank tightening, the chief economists said they expect the monetary policy stance to remain constant in most of the world this year. However, a majority expect further tightening in Europe and the US (59% and 55%, respectively). They noted that 2023 is likely to involve a difficult balancing act for policy-makers between tightening too much or too little.

“With two-thirds of chief economists expecting a world-wide recession in 2023, the global economy is in a precarious position. The current high inflation, low growth, high debt and high fragmentation environment reduces incentives for the investments needed to get back to growth and raise living standards for the world’s most vulnerable,” said World Economic Forum Managing Director Saadia Zahidi. “Leaders must look beyond today’s crises to invest in food and energy innovation, education and skills development, and in job-creating, high-potential markets of tomorrow. There is no time to lose.”

Multiple headwinds are also expected to exert a drag on business activity in 2023. Nine out of 10 respondents expect both weak demand and high borrowing costs to weight on firms, with more than 60% also pointing to higher input costs. These challenges are expected to lead multinational businesses to cut costs, with many chief economists expecting firms to reduce operational expenses (86%), lay off workers (78%) and optimise supply chains (77%).

More broadly, the chief economists expect the global landscape to remain challenging for businesses – 100% of respondents expect global geopolitical trends to continue redrawing the map of global economic activity along new geopolitical fissures and fault lines. This wider economic shift will likely reverberate through trade, investment, labour and technology flows, creating myriad challenges and opportunities for business.

One positive signal is that supply chain disruptions are not expected to cause a significant drag on business activity in 2023.

While the Forum’s Global Risks Report 2023 recently found the cost-of-living crisis to be among the world’s most urgent risks, the chief economists see the crisis potentially nearing its peak, with a majority (68%) expecting it to have become less severe by the end of 2023. A similar trend is evident in relation to the energy crisis, with 64% expecting some improvement by year end. In addition, survey respondents highlighted a number of potential sources of optimism at the start of 2023, including the strength of household finances, growing signs of easing inflationary pressures and continued labour-market resilience.