Friday Jul 10, 2026

Friday Jul 10, 2026

Tuesday, 9 August 2016 00:01 - - {{hitsCtrl.values.hits}}

SLFRS 15 Revenue from Contracts with Customers will supersede SLFRS 18 Revenue, SLFRS 11, Construction Contracts and revenue related interpretations

It is effective for financial periods beginning on or after 1 January 2018, with earlier application permitted.

Manil Jayesinghe Assurance leader for Ernst & Young Sri Lanka says, “SLFRS 15 requires entities to evaluate contractual terms and customary business practices to identify all the promised goods and services in a contract. The standard provides a greater amount of guidance to determine whether any of those goods and services should be accounted for separately.”

“The biggest challenge for companies will be to move away from transaction based accounting to contract based accounting. Present systems and procedures cater to accounting for transactions. SLFRS 15 and many other new accounting standards require companies to start record keeping when they enter into a contract, and not at the point of a transaction. This will require a significant mind set change and also to current systems and procedures.”

The principles in the new standard will be applied using the following five steps:

1. Identify the contract(s) with a customer

2. Identify the performance obligations in the contract

3. Determine the transaction price

4. Allocate the transaction price to the performance obligations in the contract

5. Recognise revenue when (or as) the entity satisfies a performance obligation

An entity will need to exercise judgment when considering the terms of the contract(s) and all of the facts and circumstances, including implied contract terms. An entity also will have to apply the requirements of the new standard consistently to contracts with similar characteristics and in similar circumstances.

The model applies to each contract with a customer. Contracts may be written, oral or implied by an entity’s customary business practices but must be enforceable by law and meet specified criteria. One of the criteria is that an entity must conclude it is probable that it will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to the customer. The amount of consideration to which an entity will be entitled as per the standard may differ from the stated contract price (e.g., implied price concessions, change in circumstance of your customer, etc).

“The collectability evaluation under SLFRS 15 will be crucial in many industries, and it will be a new process for many organisations in terms of financial reporting,” added Manil.

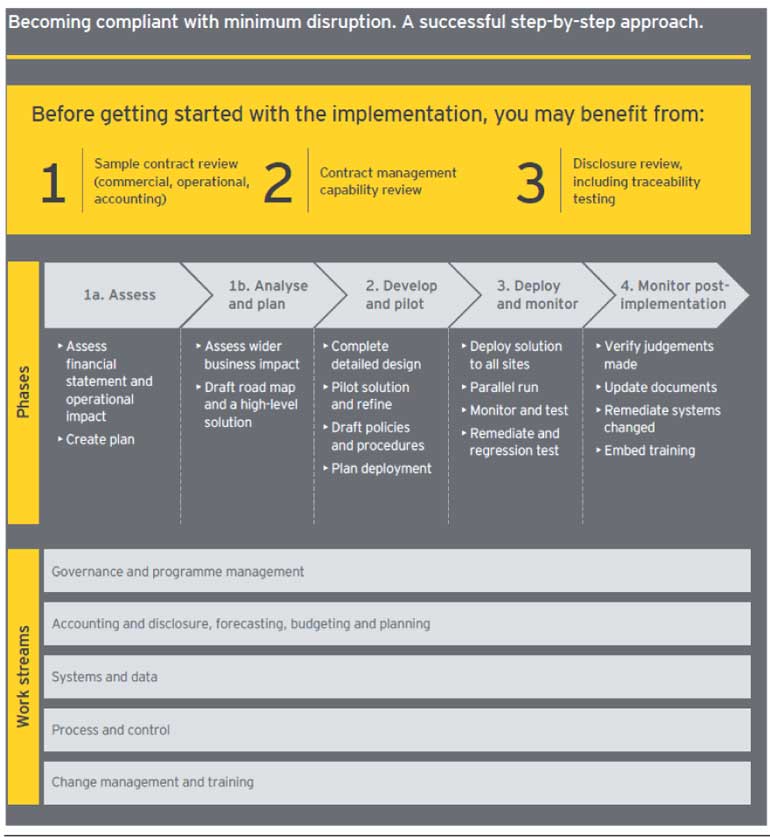

Boards of companies need to take early action in implementing the standard, in order to avoid nasty surprises in 2018. The changes required by SLFRS 15 may be drastic in terms on achieving key performance indicators such as, revenue and profit.

On both an interim and annual basis, an entity generally will have to provide more disclosures than it does today and include qualitative and quantitative information about its transactions accounted for under the new standard and significant judgments made (and changes in those judgments).