Sunday Jul 12, 2026

Sunday Jul 12, 2026

Tuesday, 1 December 2015 01:34 - - {{hitsCtrl.values.hits}}

Moody’s has said that Sri Lanka’s continued high fiscal deficits are credit negative.

This assessment from Moody’s is following the maiden Budget presented by the unity Government on 20 November. At present Moody’s sovereign rating on Sri Lanka stands at B1 stable.

It said the Sri Lankan Government announced its budget for calendar 2016, which targets a fiscal deficit of 5.9% of GDP, close to the Government’s 2015 deficit forecast of 6.0% and underpinned by plans to increase spending on education, health and infrastructure.

“If implemented, such spending would enhance growth prospects but would further delay Sri Lanka’s fiscal consolidation and add to the Government’s already high debt, a credit negative,” Moody’s said.

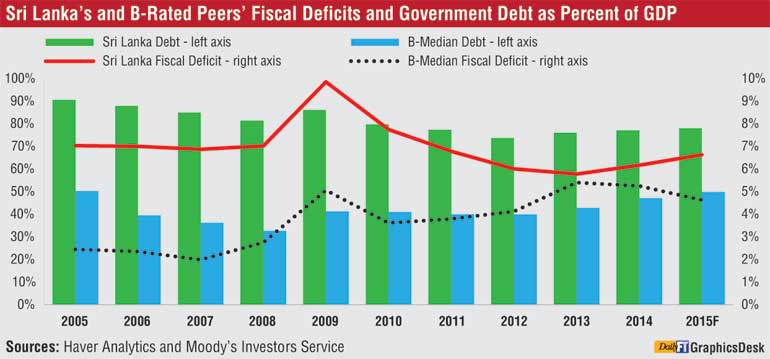

Although Sri Lanka’s deficits are down from a peak of 9.9% of GDP in 2009, fiscal consolidation has stalled, with deficits exceeding original targets in 2014 and 2015. “There is a similar risk of the 2016 budget deficit overshooting targets if nominal GDP growth is lower than forecast or if the Government does not receive the higher tax and non-tax revenues that the budget expects,” it added.

The budget foresees Government revenues, which have been 12%-13% of GDP over the past four years, increasing to 16.4% in 2016. Government expenditures, meanwhile, are set to rise to 22.3% of GDP from 18%-19% in the previous four years.

Moody’s said much of this increase in expenses will go toward public investment rather than current expenditures, which is a favorable incremental shift in the composition of expenses. However, if revenue underperforms during the year, as it has in the past two years, authorities may have to revisit investment plans to meet deficit targets, since recurrent expenses will be difficult to roll back. Moreover, even if Sri Lanka meets its budget deficit target, the Government’s fiscal position will remain weaker than most similarly rated sovereigns (see exhibit).

A weak revenue base is the key constraint on Sri Lanka’s fiscal position. Sri Lanka’s Government revenue

ratio, even if it meets the budget’s ambitious 16.4% of GDP target next year, will remain below the median for B-rated sovereigns, which is 21.4%.

In detailing its 2016 budget, the Government pointed out that Sri Lanka’s revenue ratios are also well below what they were two decades ago. In 1990, for instance, Sri Lanka’s tax revenue/GDP ratio was 19%. The decline in the ratio largely is due to lower growth in value-added taxes collected, which has led to a decline in their share of taxes to 26% in 2014 from more than 40% a decade ago.

“This is a result of weak tax compliance and a proliferation of tax exemptions,” Moody’s added.

It also said the coalition Government that took office earlier this year has acknowledged the macroeconomic constraints posed by high budget deficits, and pledged to address them. But its measures to increase public employee salaries and social welfare spending in 2015 have added to fiscal pressures.

In addition to the increase in public investment, the 2016 budget contains a few other credit-relevant measures. One proposes to increase the limit for public guarantees of investment in roads, electricity,

drainage systems and other infrastructure projects to 10% of GDP from 7%, while also increasing

guarantees for public-private partnership projects. This will raise sovereign contingent liabilities.

The budget also reduces the limit on purchases of domestically issued government debt by non-residents to 10% from 12.5%. Lower foreign holdings of domestic Government debt can lower the sovereign’s vulnerability to shifts in international market sentiment, and lowers exchange rate volatility that can occur from foreign flows related to domestic asset purchases. However, given that non-resident purchases were already below the limit, the measure is unlikely to have an immediate effect.

Business and investment measures

Moody’s said the 2016 budget also proposes a number of measures to enhance the business environment, including tax incentives, removing ownership restrictions on investments in certain sectors and opening up the management of Export Processing Zones to private companies.

“Although these measures are unlikely to immediately produce significant revenue or growth, they signal the government’s efforts to increase domestic and foreign private investment,” Moody’s said. Foreign direct investment into Sri Lanka averaged 1.5% of GDP over the past five years, less than half the median of 3.1% among similarly rated peers. “If the perception of greater openness to foreign direct investment translates into actual increases in investment, it would be credit positive,” it added.