Friday May 29, 2026

Friday May 29, 2026

Thursday, 2 June 2016 00:00 - - {{hitsCtrl.values.hits}}

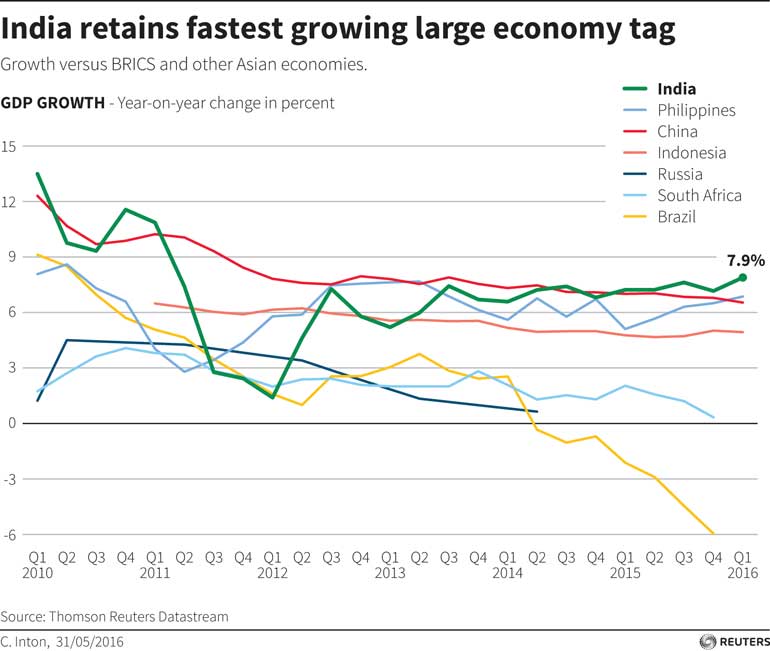

Reuters: India gathered momentum in the March quarter to extend its lead as the world’s fastest growing large economy, helping Prime Minister Narendra Modi craft an impressive sales pitch for meetings with investors in the United States next week.

Modi is due to travel to Washington on 7-8 June where he will meet heads of top U.S. companies.

Having swept to power two years ago promising to revitalise Asia’s third-largest economy, Modi has boosted spending on defence and infrastructure, while consumer demand has risen thanks to lower interest rates.

Those pro-growth policies helped gross domestic product grow 7.9% year-on-year in the March quarter, faster than the December quarter’s 7.2%.

A Reuters survey of economists had forecast growth of 7.5 in the March quarter.

The strong headline number masks subdued private investment and shrinking exports, which continue to hold India back.

Still, India’s growth has overtaken that of fellow Asian giant China, which grew 6.7% in the March quarter - the slowest in the world’s second largest economy in seven years.

The figures from India’s Statistics office also showed GDP grew 7.6% in the 2015/16 fiscal year that ended in March, in line with an earlier official estimate. Growth was 7.2% in 2014/15.

Success in bringing down inflation has given the Reserve Bank of India (RBI) room to cut its policy repo rate by 150 basis points since January 2015, reducing it to 6.50% - the lowest level in more than five years.

The GDP data reinforced expectations that the RBI would keep its policy rate on hold at a review next Tuesday.

“Momentum is building up faster than anticipated and there is a demand pick-up on the horizon,” said Yes Bank Chief Economist Shubhada Rao.

“This definitely spells out a positive story that there will soon be a recovery in private sector capex.”

Growth in the March quarter was driven by a rebound in farm output, an improvement in mining and a sharp pickup in electricity production.

The farm sector grew by 2.3% from a year ago compared with a 1.0% contraction in the December quarter. With a good rain forecast, after two successive years of drought, farm sector output should improve in coming months and lift depressed demand in the countryside where two-thirds of Indians live.

Mining grew 8.6% in the March quarter, up from 7.1% in the previous quarter. Electricity, water and gas production growth jumped to 9.3% from 5.6% in the December quarter.

Reuters: Pakistan achieved GDP growth of 4.7% in the fiscal year ending in June 2016, missing its target of 5.5%, the Prime Minister’s office announced on Monday.

The Government has set a growth target of 5.7% for the next fiscal year, according to a statement. Pakistan’s financial year runs from July to June.

Nawaz Sharif’s announcement comes ahead of Friday’s presentation of his Government’s budget for the 2016-17 financial year.

The Government has set a growth target of 3.5% for the agricultural sector, 7.7% for the industrial sector and 5.7% for the services sector for the coming year.

Friday’s budget will include 1,675 billion rupees ($15.98 billion) in National Development Outlay, including 800 billion rupees ($7.63 billion) in federal funds and 875 billion rupees ($8.35 billion) in funds to the provinces, the statement said.

Pakistan’s economy, despite its missed targets, grew at its highest rate for eight years this year. It remains plagued by chronic power shortages, poor infrastructure and flagging exports, however.

On May 21, Pakistan’s central bank cut its key policy rate by 25 basis points to 5.75%, mainly over concern at the missed GDP growth target.

In April 2015, China announced it would invest $46 billion in the China Pakistan Economic Corridor, a project that would link western China to the Arabian Sea through Pakistan, creating a major new trade route.

“CPEC has the capacity for further contributing to GDP and will have far-reaching effect in consolidating the economic outlook of the country in years ahead,” said Monday’s statement.