Tuesday Jul 14, 2026

Tuesday Jul 14, 2026

Wednesday, 4 May 2016 00:00 - - {{hitsCtrl.values.hits}}

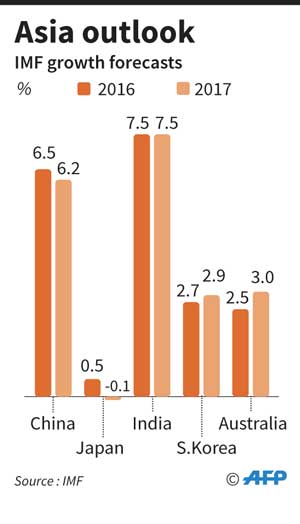

Sydney (Reuters): Japanese manufacturing activity shrank in April at the fastest pace in more than three years as deadly earthquakes disrupted production, while output in China and the rest of Asia remained lukewarm at best.

Even the former bright spot of India took a turn for the worse as both domestic and foreign orders dwindled, pulling its industry barometer to a four-month trough.

Surveys due later on Monday are expected to show only sluggish activity in Europe and the United States as the world’s factories are dogged by insufficient demand and excess supply.

“The backdrop remains one of sub-trend growth, inflation that is below target, difficulty in increasing revenue as margins are sacrificed to win modest volume gains, slow wage growth cramping spending and central banks that have used up much of their policy ammunition,” was the sober assessment of Alan Oster, chief economist at National Australia Bank.

That is exactly why the U.S. Federal Reserve has been dragging its feet on a follow-up to its December rate hike, leaving the markets in a sweat in case they move in June.

Doubts about policy ammunition mounted last week when the Bank of Japan refrained from offering any hint of more stimulus, sending stocks reeling as the yen surged to 18-month highs.

The Nikkei share index was down another 3.6% on Monday while the yen raced as far as 106.14 to the dollar and squeezed the country’s giant export sector.

Industry was already struggling to recover from the April earthquakes that halted production in the southern manufacturing hub of Kumamoto.

The impact was all too clear in the Markit/Nikkei Japan Manufacturing Purchasing Managers Index (PMI) which fell to a seasonally adjusted 48.2 in April, from 49.1 in March.

The index stayed below the 50 threshold that separates contraction from expansion for the second straight month.

The news was only a little better in China where the official PMI was barely positive at 50.1 in April, a cold shower for those hoping fresh fiscal and monetary stimulus from Beijing would enable a speedy pick up.

The findings were “a little bit disappointing”, Zhou Hao, senior emerging market economist at Commerzbank in Singapore, wrote in a note. “To some extent, this hints that recent China enthusiasm has been a bit overpriced and the data improvement in March is short-lived.”

South Korea’s activity did at least stabilise in April after contracting for three months straight, with the Nikkei/Markit PMI edging up to 50.0, from 49.5 in March.

Yet it also reported demand from China was the worst in three months, with exports to its biggest market tumbling 18.4% on-year. Likewise, weakness in new orders and exports dragged on Taiwanese activity in April. In Australia, firms reported another solid month of sales, profits and employment in April, suggesting the broader economy was coping with a protracted slowdown in mining investment.

National Australia Bank’s monthly survey of more than 400 firms showed its index of business conditions dipped three points to +9 in April. That was down from its highest since early 2008 but still above the long-run average.

That resilience has been cited by the Reserve Bank of Australia (RBA) as one reason it kept interest rates steady at 2% over the last couple of months.

The central bank holds its May policy meeting on Tuesday and there is much speculation it could cut rates following alarmingly low readings for inflation in the first quarter.

Surveys from Europe and the U.S. due later in the session are expected to show output continued to expand in April, albeit at a modest pace.

The euro zone version of the PMI is expected to hold at 51.5, though with scant sign of a return of pricing power across industries.

The influential U.S. reading from the Institute of Supply Management was forecast to dip back to 51.4, from 51.8, ahead of the always-pivotal payrolls report out on Friday.