Saturday Jul 04, 2026

Saturday Jul 04, 2026

Monday, 5 November 2018 00:00 - - {{hitsCtrl.values.hits}}

HONG KONG(Reuters): The economic impact of the intensifying trade war between Washington and Beijing appeared to deepen last month with factory activity and export orders weakening across Asia, but analysts warned the worst was yet to come.

In a sign conditions for exporters and factories were deteriorating, manufacturing surveys showed marginal growth in China, a slowdown in South Korea and Indonesia and a contraction in activity in Malaysia and Taiwan.

Those figures follow weaker-than-expected industrial production data from Japan and South Korea, with output in the latter shrinking the most in over 1-1/2 years.

By contrast, the US ISM manufacturing survey for October was expected to show a much faster growth pace than in Asia, albeit a tad slower than in September, supporting the outlook for further Federal Reserve rate hikes.

Worryingly, the prospects for higher US rates could feed back more market pain for the region’s externally vulnerable economies — Indonesia, India and the Philippines, which have already been forced to raise rates to mitigate a sell-off in currencies, stocks and bonds.

“You have a tightening of monetary conditions around the world, a slowdown in Chinese demand, and financial market turmoil that affects sentiment and investment decisions,” said Aidan Yao, senior Asia EM economist at AXA Investment Managers.

Yao said many orders from abroad are still frontloaded in anticipation of yet more tariffs and the impact is still mostly indirect, through the business confidence channel.

“The real economic shock is yet to come,” he said.

China’s manufacturing sector barely grew last month after stalling in September and export orders contracted further, according to a private sector manufacturing report. An official survey showed the manufacturing sector expanding at its weakest pace in over two years, hurt by slowing demand both externally and domestically.

Japan showed more resilience, with activity picking up, though at a slower rate than in a previous flash estimate. The world’s third-largest economy faces pressures in other areas with its central bank trimming the inflation outlook on Wednesday, flagging external risks.

Its tech-specialist neighbour and Southeast Asian economies look more exposed, however.

A DBS analysis of Asian supply chains for products bound for the United States shows the biggest exposures in machinery and electrical equipment in South Korea, Singapore, Malaysia, the Philippines and Taiwan.

South Korea’s minerals and petrochemicals exports were also exposed, as well as Indonesia’s transportation industry, according to the DBS report, which looked at the correlation between China’s imports from Asia and its US exports.

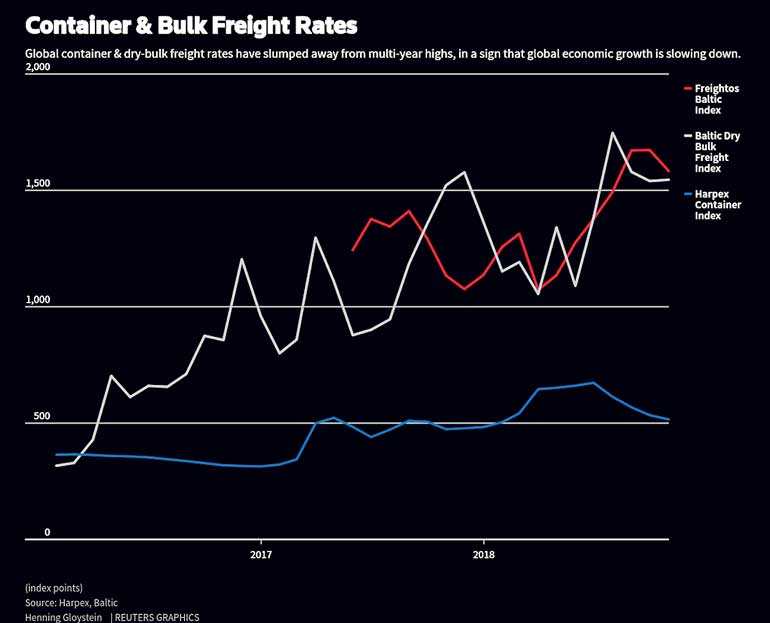

The Harpex index, which tracks weekly container shipping rate changes and is a measure of global shipping activity, is now down 25% since its June peak.

China slowdown

The pressure on China’s economy is not just external. Economic growth cooled to its weakest quarterly pace since the global financial crisis at 6.5%, exhibiting lacklustre domestic demand by Chinese standards.

Things can get worse.

Washington has already imposed tariffs on $250 billion worth of Chinese goods, and China has retaliated with duties on $110 billion worth of US goods in a row sparked by US President Donald Trump’s demands for sweeping changes to China’s intellectual property, industrial subsidies and trade policies.

But absent any deal between Trump and Chinese leader Xi Jinping, who are expected to attend a G20 summit this month in Buenos Aires, the recently introduced 10% tariffs on $200 billion of Chinese goods will be raised to 25% and other tariffs may be placed on the remaining $250 billion-or-so of Chinese products which escaped the initial rounds.

“As everyone anticipates a further tariff hike...there is still a lot of front-loading going on. After Jan. 1, we expect many trade and economic activities to tumble,” said Kevin Lai, senior economist at Daiwa Capital Markets.

That all bodes ill for Asian financial markets, with many of the region’s currencies and bourses deep in the red this year. Those economies with high current account deficits have been particularly vulnerable to capital flight.

The rate hikes that central banks deployed to stop rapid declines in their currencies might also further slow activity.

“I would argue it to be wise to remain wary of EM currencies into those trade discussions a few weeks hence, and lean towards the US dollar instead,” said Michael Every, senior APAC strategist at Rabobank.

Outliers

Manufacturers in India, which rely more on domestic demand, defied expectations for a slower expansion in activity in October and grew at the fastest pace in four months.

Vietnam was another standout economy in the region, showing an acceleration in manufacturing activity in October. The country’s labour base is still cheap by regional standards while its trade ties with the United States remain clear of the kind of disputes with which its larger Asian peers are wrestling.

As such, it’s seen as potential winner from the Sino-US trade war as companies consider rebasing and re-routing their supply chains away from the crossfire between the world’s two largest economies.

“Vietnam, by our estimation is the least impacted country in Asia...because if global companies have to move, Vietnam is a viable option,” AXA’s Yao said.

“But it will take a long time for Vietnam to take up some of the market share that China leaves behind.”