Tuesday Jul 07, 2026

Tuesday Jul 07, 2026

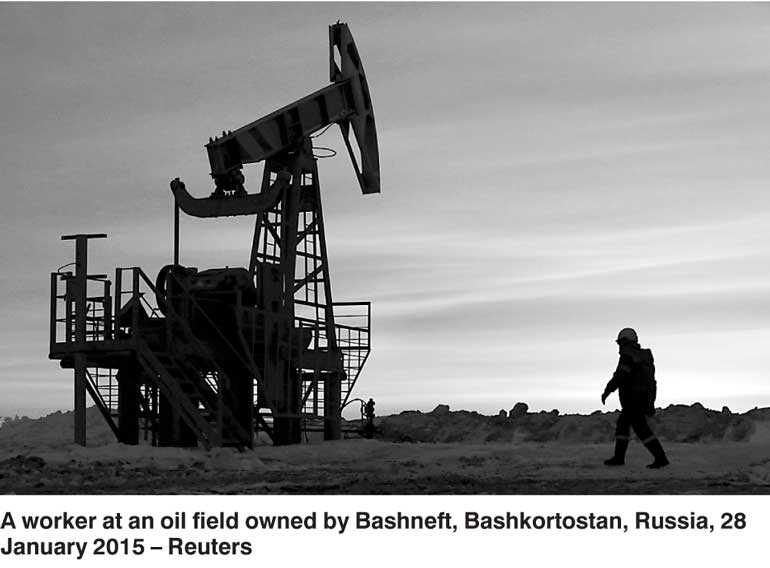

Saturday, 18 August 2018 00:10 - - {{hitsCtrl.values.hits}}

MOSCOW (Reuters): Stiff new US sanctions against Russia will only have a limited impact on its oil industry because it has drastically reduced its reliance on Western funding and foreign partnerships and is lessening its dependence on imported technology.

Western sanctions imposed in 2014 over Russia’s annexation of Crimea have already made it extremely hard for many state oil firms such as Rosneft to borrow abroad or use Western technology to develop shale, offshore and Arctic deposits.

While those measures have slowed down a number of challenging oil projects, they have done little to halt the Russian industry’s growth with production near a record high of 11.2 million barrels per day in July – and set to climb further.

Since 2014, the Russian oil industry has effectively halted borrowing from Western institutions, instead relying on its own cash flow and lending from state-owned banks while developing technology to replace services once supplied by Western firms.

Analysts say this is partly why Russian oil stocks have been relatively unscathed since US senators introduced legislation to impose new sanctions on Russia over its interference in US elections and its activities in Syria and Ukraine.

The measures introduced on 2 August, dubbed by the senators as the “bill from hell”, include potential curbs on the operations of state-owned Russian banks, restrictions on holding Russian sovereign debt as well as measures against Western involvement in Russian oil and gas projects.

While the rouble has fallen more than 10% and Russian banking stocks have slumped 20% since the legislation was introduced, shares in Russian oil firms have climbed 2%, leaving them 27% higher so far in 2018.

“The main driver of the Russian oil industry’s profitability is the oil price denominated in rubles and it is currently posting new records as the rouble is getting weaker. Hence the sanction noise often even has a positive impact on Russian oil stocks,” said Dmitry Marinchenko at Fitch Ratings. The prospects for the latest US sanctions bill are not immediately clear. It would have to pass both the Senate and House of Representatives and then be signed into law by President Donald Trump.

To be sure, Washington could really hurt the Russian oil industry if it introduced Iran-like measures forbidding oil purchases from the country. But given Russia produces more than 11% of global crude, such a measure would lead to a major spike in oil prices and hit the United States itself hard as it is the world’s largest oil consumer.

Russian gas exporting monopoly Gazprom, for example, has maintained its output since 2014 and actually increased exports to Europe to an all-time high in 2017, securing a 34% share of EU markets amid rising demand.

But of all Russian oil and gas companies, it is the only one to have borrowed significant sums from the West – about $5 billion in 2017 and $3 billion in 2018 so far – using Eurobonds and syndicated loans.

What’s more, those amounts are only equivalent to a small proportion of Gazprom’s annual capital spending of $22 billion. The rest of the Russian oil industry invests a similar amount each year as well, mostly without Western funding.

That represents a major departure from the years prior to the sanctions when the lion’s share of Russian oil industry’s borrowing came from Western banks or export-backed facilities with trading houses and major oil companies.

In 2013, for example, a year before the first Western sanctions, Rosneft alone borrowed more than $35 billion from Western institutions to buy smaller rival TNK-BP and to fund its capital spending.

The weakest link in the Russian oil industry in the face of sanctions has traditionally been high-end Western technology such as complex drilling, hydraulic fracturing or IT, said Denis Borisov, director of EY’s oil and gas centre in Moscow.

Russia’s drilling and oil servicing market is worth about $20 billion a year and the share of the market held by Western service companies has remained fairly steady over the last few years and at about a fifth.

“But the process of replacing foreign equipment with local production has gathered pace,” said Borisov.

Rosneft, which produces 40% of Russian oil, has recently tested its own simulated hydraulic fracturing technology – the extraction technique that spurred the boom in US shale oil production.

The technology first came to Russia mainly via major Western oil services firms such as Schlumberger and Halliburton.

Companies such as Schlumberger are still doing a lot of complex drilling work in the Caspian Sea and West Siberia for Lukoil, as well as working on the world’s longest extended reach well for Exxon and Rosneft off the Sakhalin island.

But Fitch’s Marinchenko said the reliance of Russian oil firms on Western technology has declined since 2014 thanks to imports from China and local production of drilling equipment.