Monday Apr 20, 2026

Monday Apr 20, 2026

Friday, 18 March 2016 00:49 - - {{hitsCtrl.values.hits}}

Moody’s yesterday welcomed the $ 700 million currency swap between Sri Lanka and the Reserve Bank of India (RBI) as a means to ease pressure on the Balance of Payments but expressed caution as the country remains vulnerable.

On 10 March, Sri Lanka (B1, stable) received a $700 million currency swap from India (Baa3, positive) through the Reserve Bank of India (RBI), two days after securing a $400 million swap under the RBI’s South Asian Association for Regional Co-operation (SAARC) facility.

Moody’s said these arrangements, which replace the RBI swap line that expired the week before, will offset in the near term the balance of payments pressures posed by slowing capital inflows and more recently a dip in remittance inflows. Sri Lankan authorities are also negotiating a more medium-term financing arrangement with the International Monetary Fund (IMF).

The swap lines and potential IMF financing demonstrate Sri Lanka’s access to official funding during periods when global market financing is becoming more difficult.

However, recourse to such official funding also highlights the fact that Sri Lanka’s foreign exchange earnings and reserves fall short of its external financing requirements.

Moreover, these requirements have increased due to the country’s large fiscal deficits and the role that external funding has played in supporting domestic economic activity.

While the official financing will alleviate immediate external liquidity risks, Sri Lanka’s balance of payments is unlikely to meaningfully stabilise without a reduction in government deficits and debt, as well as an acceleration in non-debt sources of external financing, such as Foreign Direct Investment (FDI).

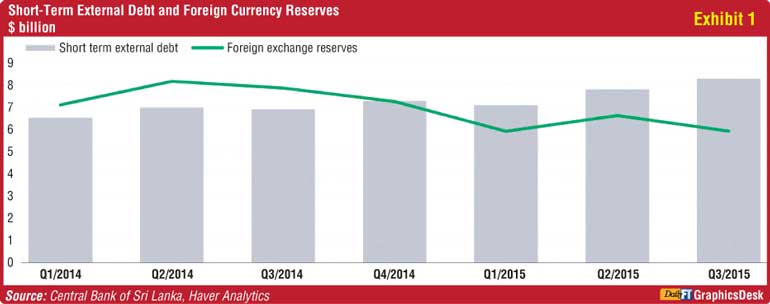

With short-term external debt of $8.3 billion as of Q3 2015 and a current account deficit not fully funded by net FDI inflows, Sri Lanka is dependent on external financing to stem the fall in its foreign exchange reserves. And external financing has become tighter over the last year. 2015 was a period of domestic political transition in Sri Lanka, marked by presidential and parliamentary elections. Election related spending and looser fiscal policy led to rapidly rising imports, while a slowdown in remittances added to the pressures on the current account.

At the same time rising global risk aversion lowered foreign capital flows. Foreign currency reserves fell to $5.6 billion at end-February 2016, from $6.6 billion in June last year.

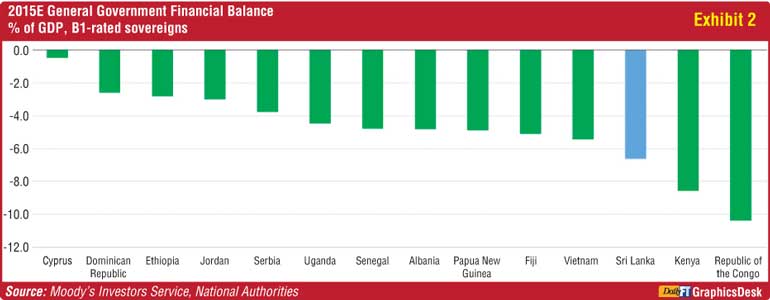

Sri Lanka’s sizeable fiscal deficits and large Government debt have raised external financing needs.

The country’s low revenue base is a key constraint on fiscal consolidation. To address its weak fiscal position, the Cabinet has recently approved fiscal reform measures which include increases in Value Added Tax (VAT) and income taxes.

While the measures await Parliamentary approval, the ruling party’s coalition majority increases the probability that they will be passed. Such measures are also likely to be part of the agreement with the IMF, currently being negotiated.

If they are implemented and effective, these measures would be credit positive in that they would partly address one of Sri Lanka’s key credit weaknesses – low and narrow-based government revenues.

On the other hand, higher taxes and in particular a higher VAT may dent economic growth and raise inflation which could lead to further interest rate increases.

Our assessment is that the overall impact of these measures will ultimately depend on how effectively the higher taxes will raise revenues. As such, the efficacy of tax collections is also important.

Alongside currency swaps, the Government is actively seeking longer-term multi-lateral financing and FDI, which will help bolster economic growth and provide relatively stable external financing. On top of a previously announced $2 billion (2.4% of GDP) in financing from the Asian Development Bank, the Sri Lankan Government has approved a $1.4 billion Colombo port city complex financed by Chinese investors. Between 2010 and 2014, Chinese investment backed the development of several infrastructure projects including the Hambantota Port, a coal power plant, and an airport.

Such infrastructure projects signal the re-emergence of Chinese financing support, especially since the unveiling of the Maritime Silk Road initiative in March 2015 which will continue to support trade flows between the two countries.

In 2015, net FDI inflows into Sri Lanka were estimated at about 1.0% of GDP, lower than for similarly-rated sovereigns.

An increase in FDI would reduce Sri Lanka’s reliance on debt to finance its current account deficit, a feature that has weighed on the sovereign credit profile. It would also mitigate any further rise in external debt, which at 53.1% of GDP is higher than that of Vietnam (B1, stable) and Pakistan (B3, stable), and above the 46.8% median for B-rated peers.