Tuesday Jul 07, 2026

Tuesday Jul 07, 2026

Saturday, 13 August 2022 00:40 - - {{hitsCtrl.values.hits}}

|

Chairman Harsha Amarasekera (left) and Managing Director Nanda Fernando

|

|

Sampath Bank said yesterday it continued to maintain a solid capital base and stable liquidity profile in the first half of 2022 notwithstanding multiple economic challenges.

In a statement, the bank said it remains vigilant in identifying the current economic issues and has continued to implement in a proactive manner the required countermeasures, clearly demonstrating its strength and stability.

In line with that objective and in order to improve the foreign currency liquidity position, the bank continues to focus and promote inward remittances as well as to encourage the inflow of export proceeds. The bank further reinforced its commitment to all its stakeholders by continuing to support all affected segments to sustain their respective businesses in order to ride out the current economic crisis.

Despite the prevailing economic turmoil, the bank posted a commendable PAT of Rs. 7.1 billion and PBT of Rs. 9 billion for the period ended 30 June 2022, reflecting a minor increase of 0.3% and slight decrease of 5.5% respectively compared to the figures declared in 1H 2021. In the meantime, the Group declared a PAT of Rs. 7.4 billion and PBT of Rs. 9.6 billion, denoting a decline of 2% and 5.5% respectively over the first half of 2021.

Fund-based income

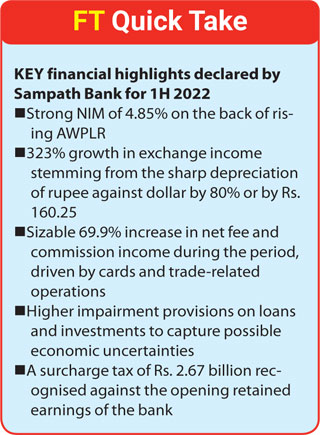

Total interest income increased by 41.1 % year on year to Rs. 59.2 billion in the first half of 2022, compared to Rs. 41.9 billion in the same period of the previous year. This significant increase in interest income is due to the upward trend in interest rates in the first half of 2022. The AWPLR at the end of the reporting period reached 22.62%, which is 1,711 bps higher than the rate reported on 30 June 2021.

Furthermore, the current AWPLR surpassed the end 2021 figure by 1,401 bps. At the same time, the interest rate on a one-year treasury bill climbed by 1,861 bps from the treasury bill rate reported at end of 30 June 2021 and stood at 23.84% at the end of 30 June 2022.

Interest expenses increased by 22.6% compared to the corresponding period of last year due to rising interest trend. The bank’s total interest expense was Rs. 27.8 billion at the end of the current reporting period compared to Rs. 22.7 billion reported in 1H 2021. Prudent asset and liability management however ensured that net interest income grew by 63% in 1H 2022. This trend is reflected in the NIM growth of 124 bps reported for the period.

Non-Fund based income

The bank recorded a significant increase of 69.9% in its net fee and commission income (NFCI) in 1H 2022 compared to the same period of the previous year. NFCI is made up of income from a variety of sources, including loans and advances, credit cards, trade, and electronic channels. In the period under review, significant growth was noted in card-related business volumes and as well as fee and commission income from trade-related activities.

During the first half of 2022, net other operating income increased to Rs. 16 billion, an unprecedented 378% increase compared to Rs. 3.4 billion recorded in the corresponding period of the previous year.

This was mainly due to the 80% depreciation of the rupee against the dollar. Meanwhile, the bank posted a net trading loss of Rs. 2.5 billion, compared to the gain of Rs. 46 million reported during the corresponding period of the previous financial year. Total exchange income for the first six months of 2022 was Rs. 13 billion compared Rs. 3 billion registered in 1H 2021.

Impairment charge

Continuing to act prudently, the bank recognised a total impairment charge of Rs. 28.2 billion for 1H 2022 compared to Rs. 5 billion reported in the corresponding period of last year, representing a 464% increase. The impairment charge for the period under review comprises Rs. 19.3 billion for loans and advances and Rs. 7.8 billion for other financial instruments. Further, impairment charge of Rs. 1.1 billion was recorded against commitments and contingencies.

Impairment charge on loans and advances: A sizable provision was made under Economic Factor Adjustment for the period under review as the bank continued to increase the probability weightage used in the computation of impairment to reflect the deteriorating macro-economic conditions. During the second quarter of 2022, the probability weightage allocated to the worst-case scenario was further increased.

The economic factor adjustment methodology was continuously refined to reflect the heightened economic vulnerabilities and captured the latest data with regard to all major economic variables. This was done to ensure that adequate impairment provisions were made to address the potential credit risk associated with the current economic challenges.

In order to absorb the possible losses, the bank decided to increase the allowance for overlay against the tourism sector customers. It was also decided to retain impairment provisions against the customers who exited the moratorium at the end of 2021. As a result, cumulative impairment provision against stage 1 and stage 2 loans reported a sizable increase of 27.3% and 63.5% respectively compared to 31 December 2021.

The bank continues to recognise elevated risk industries and moved such customers to Stage 2 during the period. In addition, the bank closely monitored the customers’ behaviour and shifted them from Stage 1 to Stage 2 based on their capacity to bear the adverse impacts brought on by economic issues.

Meanwhile, the cumulative impairment provision against Stage 3 loans increased by 40.52% in the first half of 2022. This was primarily caused by the increase in Stage 3 loans and the recalculation of impairment of a few Stage 3 customers compared to the year-end 2021.

Impairment charge on other financial instruments: The bank provided Rs. 7 billion against SLISBs and Rs. 11.8 billion against SLDBs as at 30 June 2022. This decision was influenced by the downgrade in Sri Lanka’s sovereign rating in May 2022 to RD from C by Fitch Ratings and other current debt restructuring actions taken by the Government.

Operating expenses

Operating expenses for the first half of 2022 amounted Rs. 13.7 billion, a 24.3% increase from the Rs. 11 billion recorded for the first half of 2021. The primary reason for the increase in operating expenses was an increase in the inflation rate, which rose significantly during the first six month of 2022.

Despite the growth recorded in the operating expenses, the bank’s cost to income ratio (CIR) dropped significantly by 1,406 bps and stood at 25.45% compared to 39.51% reported in the corresponding period of 2021. This decline in CIR was primarily triggered by an increase in total operating income that was greater than the increase in operating expenses.

Key ratios

The Return on Average Shareholders’ Equity (after tax) increased to 12.06% as of 30 June 2022 compared to 11.05% reported at the end of the year 2021. Return on Average Assets (before tax) stood at 1.43% as of 30 June 2022 as against the 1.44% reported for 2021.

Capital ratios

Throughout 1H 2022, the bank maintained all of its capital ratios well above the regulatory minimum requirements. The bank's CET 1, Tier 1, and total capital ratios on 30 June 2022 were 11.3 %, 11.3 %, and 13.82 % respectively, in comparison with 13.95 %, 13.95 %, and 17.02 % at the end of 2021.

The decline in the ratios during the reporting period is due to the combined impact of increase in risk-weighted assets resulting from the rupee depreciation, the payment of cash dividends and surcharge tax.

The bank maintained a strong position with regard to its capital ratios with sufficient buffers to absorb any shocks that may result from economic uncertainties.

Assets and liabilities

At the end of June 2022, Sampath Bank's total assets surpassed Rs. 1.3 Tn, denoting an increase of Rs. 122 billion (annualised growth of 20.2%) from Rs. 1.2 Tn as of 31st December 2021. Increases in net loans and advances and cash and cash equivalents have contributed towards the above.

Devaluation of the local currency that took place in 1H 2022 has increased the rupee value of foreign currency denominated assets which could be cited as a main reason for the balance sheet growth. If the impact of the currency fluctuation is eliminated, the bank would have recorded an annualised growth of approximately 5%.

Total advances grew by 29.7 % (annualised) in 1H 2022 to reach Rs. 933 billion as at 30 June 2022, up from Rs. 813 billion at the end of December 2021. The rupee loan book expanded by 13.6% (annualised).

It should be noted that following rupee depreciation of Rs. 160.25 against the dollar during the period, the value of foreign currency denominated loans increased significantly. If currency rate fluctuations were eliminated, the bank’s total loans and advances would have increased by 9.8% (annualised) during the period.

Further, the bank transferred Treasury Bonds worth of Rs. 33 billion classified under FVOCI to Amortised Cost during the reporting period as permitted by the SoAT on Reclassification of Debt Portfolio issued by CA Sri Lanka.

The rupee deposit portfolio contracted by 9.24% compared to the figure reported at the end of 2021. This was due to the fact that the bank had adequate liquidity throughout the period and therefore, deposit mobilisation activities were not actively pursued in 1H 2022.

At the conclusion of the first half of 2022, the bank’s CASA ratio stood at 40.6%. However, the bank resumed deposit mobilisation during the month of July 2022 by offering products under new tenors at competitive market rates.

Surcharge tax

As per the Surcharge Tax Act No. 14 of 2022, the bank is liable for the surcharge tax of Rs. 2,671 million out of the taxable income of Rs. 10,682 million pertaining to the year of assessment 2020/21. Further, the Group is liable for the surcharge tax of Rs. 3,233 million. According to said Act, the surcharge tax shall be deemed to be an expenditure in the financial statements commenced on 1st January 2020.

Since the Act supersedes the requirements of the Sri Lanka Accounting Standards, the surcharge tax expense has been accounted as recommended by the SoAT on Accounting for Surcharge Tax issued by the Institute of Chartered Accountants of Sri Lanka. Accordingly, the liability to the Surcharge Tax has been recognised as an adjustment to the opening retained earnings as at 1 January 2022, during the quarter ended 30 June 2022.