Tuesday Jul 14, 2026

Tuesday Jul 14, 2026

Monday, 14 August 2017 00:05 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary market bond yield curve reflected a parallel shift upwards during the week ending 11th August 2017, for the first time in five weeks, mainly on the belly end to the long end of the curve on the back of foreign and local selling interest and profit taking.

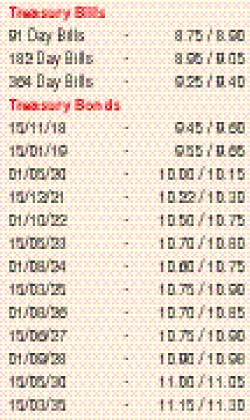

Yields on the three 2021s (i.e. 01.03.21, 01.08.21 and 15.12.21), 15.05.23, 01.08.24, 01.09.28 and 15.05.30 were seen hitting weekly highs of 10.44%, 10.50%, 10.35%, 10.80%, 10.72%, 10.92% and 11.05% respectively against its previous weeks closing levels of 10.17/21, 10.18/25, 10.17/19, 10.38/42, 10.43/48, 10.70/80 and 10.82/88.

Nevertheless the weighted averages at the weekly Treasury bills auction were seen decreasing further for a sixth consecutive week while on the short end of the yield curve, the 2018 and 2019 bond maturities continued to change hands within the range of 9.25% to 9.60% and 9.60% to 9.86%, signaling a steepening yield curve.

Meanwhile, the foreign component in rupee bonds decreased for a second consecutive week to record an outflow of Rs.866 million for the week ending 9 August.

The daily secondary market Treasury bond transacted volume for the first three days of the week averaged Rs.17.44 billion.

In money markets, the overnight call money and repo rates decreased marginally to average at 8.66% and 8.72% respectively for the week as the average net surplus liquidity in the system increased to Rs.23.41 billion against its previous week’s average of Rs.20.81.

The OMO department of Central bank continuously drained out liquidity by way of overnight repo auctions at weighted averages ranging from 7.30% and 7.33%.

Rupee appreciates further

The rupee on spot contracts continued its appreciating trend during the week to close at Rs.153.06/10 against its previous weeks closing levels of Rs.153.35/45 on the back of exporter dollar sales outweighing importer demand.

The daily USD/LKR average traded volume for the three days of the week stood at $ 76.12 million. Some of the forward dollar rates that prevailed in the market were one month – 153.70/75; three months – 155.25/35; and six months – 157.65/75.