Saturday Jul 04, 2026

Saturday Jul 04, 2026

Wednesday, 12 July 2017 09:42 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

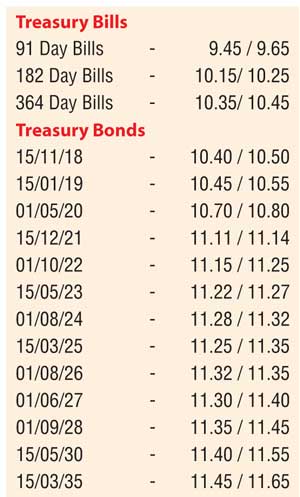

The weighted averages on the Treasury bond maturities of 15.05.2023, 15.03.2025 and 15.06.2027 were seen decreasing by 17, 11 and 12 basis points respectively to 11.21%, 11.30% and 11.37% against its previous weighted averages at its auctions conducted yesterday.

Meanwhile, the 15.12.2021 maturity recorded a weighted average of 11.14%, considerably below the 01.08.2021 average of 11.37% recorded on 13 June 2016. A total amount of Rs. 63.59 billion was accepted at the auctions against its total offered amount of Rs. 65 billion.

In secondary bond markets yesterday, yields were seen decreasing subsequent to auction results mainly on the liquid maturities of 15.12.21, 01.08.24 and 01.08.26 to intraday lows of 11.08%, 11.28% and 11.30% respectively against its previous day’s closing level of 11.17/19, 11.30/35 and 11.32/38. However, profit-taking at these levels curtailed any further downward movement. In addition, the 15.11.18 maturity was seen changing hands within the range of 10.45% to 10.50% as well.

Today’s weekly Treasury bill auction will have on offer a total amount of Rs. 29.5 billion consisting of Rs. 6.00 billion on the 91-day, Rs. 13 billion on the 182-day and Rs. 10.5 billion on the 364-day maturities. At last week’s auction, the weighted averages of both the 182-day and 364-day maturities decreased by three basis points and two basis points respectively to 10.26% and 10.45% while the weighted average on the 91-day maturity remained steady at 9.60%.

The total secondary market Treasury bond transacted volume for 10 July 2017 was Rs. 1.9 billion. Meanwhile, in money markets, the injection of liquidity by way of an overnight reverse repo auction amounting to Rs. 18.00 billion at a weighted average rate of 8.75% by the Open Market Operations (OMO) Department of the Central Bank resulted in the weighted averages of overnight call money and repo rates remaining mostly steady at 8.75% and 8.82% respectively.

The liquidity in the system stood at a net deficit of Rs. 19.99 billion with a further amount of Rs. 8.06 billion being accessed from the Standard Lending Facility at a rate of 8.75% (SLFR) against an amount of Rs. 6.07 billion being deposited with the Central Bank at the Standing Deposit Facility Rate (SDFR) of 7.25%.

Rupee remains

mostly unchanged

In the Forex market, the USD/LKR rates on spot contracts remained mostly unchanged yesterday to close the day at Rs. 153.70/75 on the back of an equilibrium market.

The total USD/LKR traded volume for 10 July was $ 41.00 million. Some of the forward USD/LKR rates that prevailed in the market were one month - 154.70/80, three months - 156.70/80 and six months - 159.75/80.