Saturday May 23, 2026

Saturday May 23, 2026

Monday, 6 February 2017 00:35 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The secondary bond market continued with its upward momentum witnessed over the previous three weeks driven by persistent foreign selling interest, as yields were seen increasing further during the early part of the week ending 3 February 2017. This was further supported by the outcome of inflation for the month of January 2017, where it increased to 5.5% and 4.5% respectively on the point to point and annual average from its previous month of 4.3% and 4.0%.

In addition, core inflation was seen spiking to 7% as well on its point to point against its previous month of 5.80% with its annualised average edging up to 4.70% from 4.40%. The more liquid maturities of 15.11.18 and the two 2021 maturities (i.e. 01.05.21 and 01.08.21) recorded the highest amount of activity as its yields were seen hitting weekly highs of 11.83%, 12.80% and 12.75% respectively against their previous weeks closing levels of 11.55/90, 12.62/72 and 12.60/68. The yield on the 01.07.19 maturity increased as well to a high of 12.00%.

Nevertheless buying interest towards the later part of the week in line with the outcome of the weekly Treasury bill auction at where the weighted average on the 182 day bill decreased for the first time in nine weeks, saw yields decreasing once again to close the week lower with the liquid maturities of 15.11.18, 01.05.21 and 01.08.21 hitting lows of 11.65%, 12.66% and 12.62% respectively. The generated demand was evident on the short end 2018 maturities of 01.02.18, 01.04.18 and 01.06.18 as it changed hands at levels of 10.65% to 10.80%, 11.00% and 11.30% as well.

The foreign holding in Rupee bonds was seen decreasing by a further Rs. 5.5 billion for the week ending 1 February 2017, to record a total outstanding amount of Rs. 233.96 billion.

Furthermore the first monitory policy announcement for the year 2017 will be due on 7 February at 7:30 a.m.

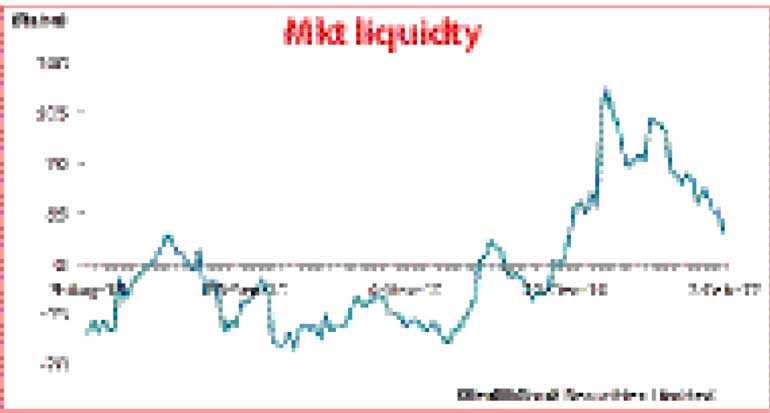

In money markets, despite average net surplus liquidity in the system dipping to Rs. 38.73 billion for week against its previous week of Rs. 55.98 billion, overnight call money and repo rates remained mostly unchanged to average 8.40% and 8.42% respectively for the week ending 3 February. The net surplus liquidity was seen dipping to a six week low of Rs. 20.61 billion on Friday. The Open Market Operations (OMO) Department of Central Bank was seen mopping up liquidity during the week by way of overnight repo auctions at weighted averages of 7.51% to 7.53%.

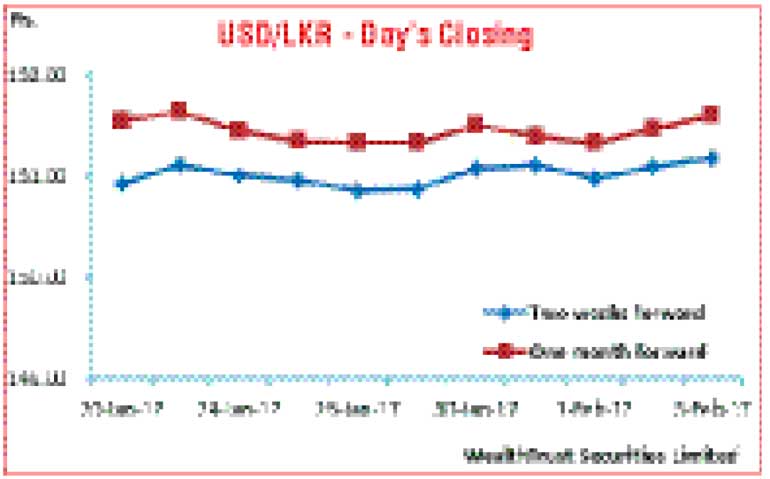

Rupee depreciates during the week

The USD/LKR rate on active two weeks and one month forward contracts depreciated during the week to close at levels of Rs. 151.15/19 and Rs. 151.55/65 against its previous weeks closing level of Rs. 150.80/95 and Rs. 151.25/40 on the back of foreign selling in Rupee bonds and importer demand outweighing export conversions. The daily USD/LKR average traded volume for the first four days of the week stood at $ 81.48 million.

Some of the forward dollar rates that prevailed in the market were three months – 153.45/55 and six months – 156.00/15.