Thursday May 14, 2026

Thursday May 14, 2026

Wednesday, 5 April 2017 01:02 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

The weighted averages at yesterday’s Treasury bond auctions were seen decreasing as the 4.08 year maturity of 15.12.2021 dipped by 29 basis points to 12.60% while the weighted average on the 6.09 year maturity of 01.01.2024 recorded 12.92% against 13.14% recorded on the 01.08.24 maturity.

All bids received on the 9.04 year maturity of 01.08.2026 were rejected. The auction drew Rs. 11.48 billion in successful bids against its total offered amount of Rs. 11.5 billion. Given below are the details of the said auction.

In the secondary bond market yesterday, activity centered on the two auctioned maturities of 15.12.21, 01.01.24 and the maturity of 01.08.24 as its yields were seen dipping to intraday lows of 12.50%, 12.73% and 12.75% respectively post-auction against its opening highs of 12.60%, 12.85% and 12.87%.

In addition, the 01.05.21 and 01.08.21 maturities were seen changing hands at levels of 12.50% and 12.53% to 12.55% respectively as well.

This was ahead of today’s Treasury bill auction where a total amount of Rs. 25 billion will be on offer consisting of Rs. 8 billion of the 91 day maturity and Rs. 8.5 billion each on the 182 day and the 364 day maturities. At last week’s auction, the weighted averages continued to increase, with the 91, 182 and 364 day maturities increasing by six basis points and 16 basis points each to 9.63%, 10.62% and 10.98% respectively.

The total secondary market Treasury bond transacted volume for 3 April 2017 was Rs. 0.74 billion.

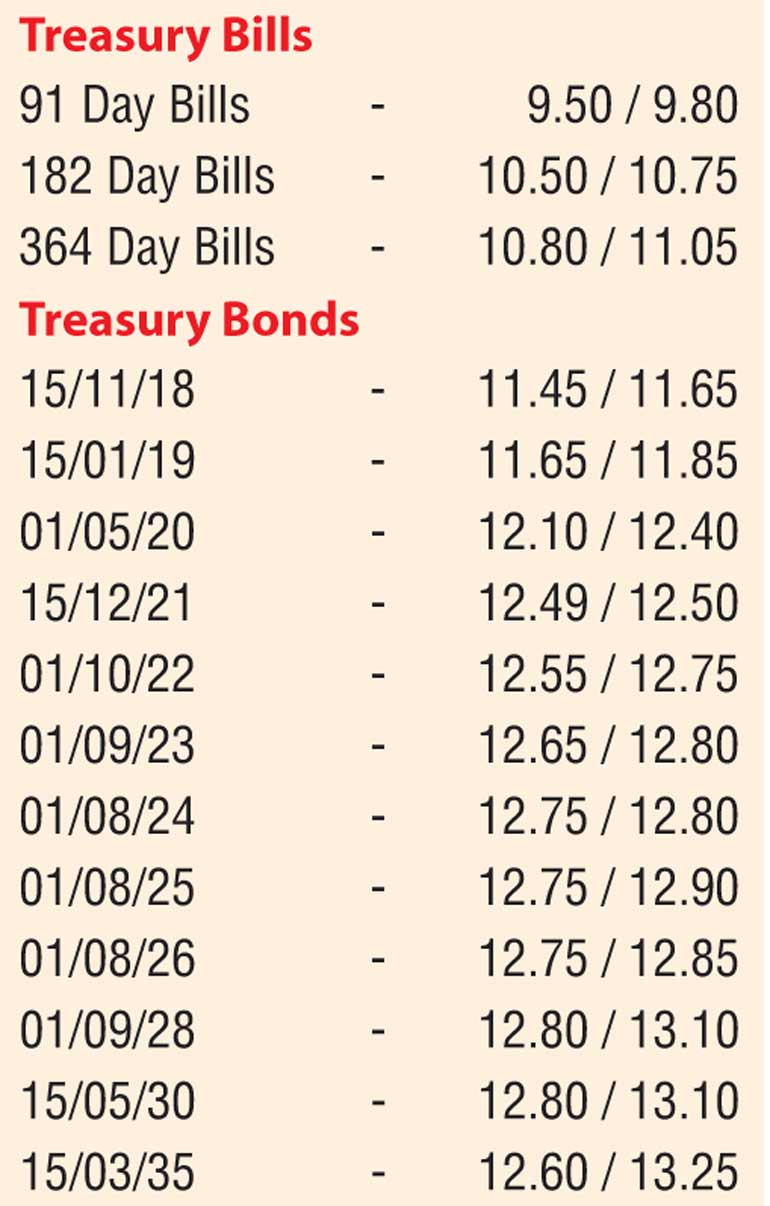

Given below are the closing, secondary market yields for the most frequently traded T-bills and bonds.

Meanwhile, in money markets, the overnight call money and repo rates averaged 8.75% and 8.84% respectively as the net liquidity shortfall in the system stood at Rs. 20.25 billion yesterday. The OMO department of the Central Bank was seen infusing an amount of Rs. 21.00 billion at a weighted average of 8.74% by way of an overnight reverse repo auction.

Rupee remains mostly unchanged

The USD/LKR rates on two-week forward contracts were seen closing the day mostly unchanged at levels of Rs. 152.35/45 while spot next contracts were traded at levels of Rs. 151.90-Rs.151.93 yesterday.

The total USD/LKR traded volume for 3 April 2017 was $ 101.75 million.

Given below are some of the forward USD/LKR rates that prevailed in the market.