Tuesday Jul 07, 2026

Tuesday Jul 07, 2026

Monday, 28 November 2016 00:01 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

By Wealth Trust Securities

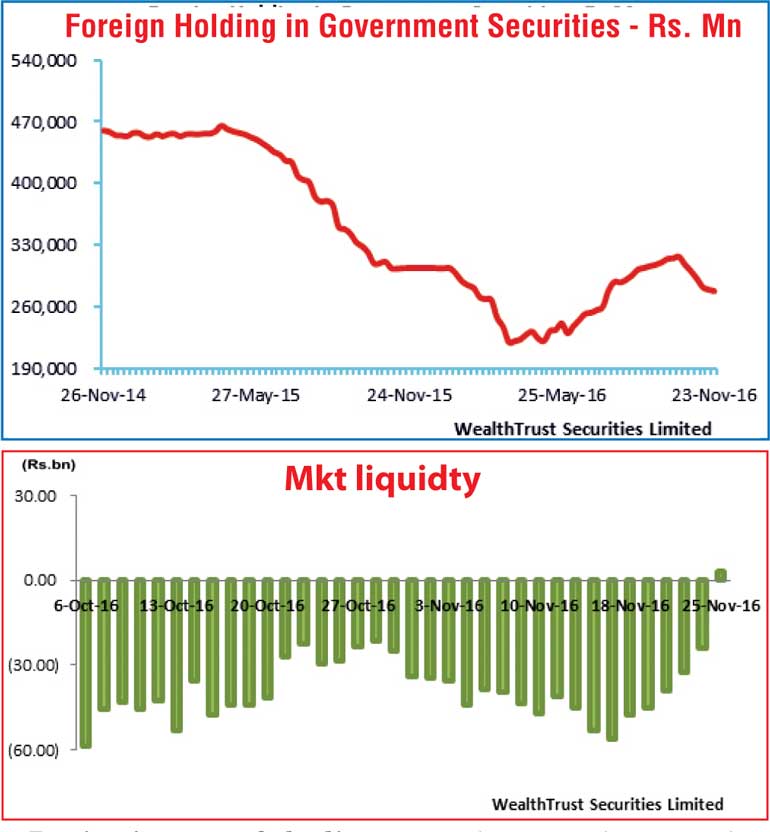

The Open Market Operations (OMO) Department of the Central Bank of Sri Lanka was seen conducting an overnight repo auction on Friday, the first time since 22 December 2015, as the market liquidity turned positive for the first time since 8 September 2016. The market recorded a net surplus of Rs. 3.02 billion on Friday while the net liquidity shortfall for the week stood at Rs. 27.57 billion, when compared against last week’s short fall of Rs. 48.73 billion. The overnight call money and repo rates remained mostly unchanged during the week to average at 8.44% and 8.63% respectively.

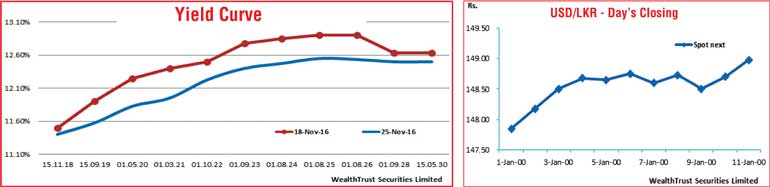

The increase in market liquidity coupled with the news of the release of $ 162 million as the second tranche of the IMF three year program, resulted in secondary market bond yields dipping during the week, reflecting a parallel shift downwards of the overall yield curve, witnessed for the first time in three weeks.

Buying interest of the liquid maturities of 15.09.19, 01.05.20, 01.03.21, 01.09.23, 01.08.24, 01.08.25 and 01.08.26 saw their yields dip to weekly lows of 11.50%, 11.75%, 12.00%, 12.30%, 12.34%, 12.55% and 12.45% respectively against its previous weeks closing levels of 11.70/10, 12.15/35, 12.25/55, 12.75/80, 12.80/90, 12.85/95 and 12.85/95. Furthermore, the 2018 maturities were seen changing hands within the range of 11.30% to 11.50%. This was despite, low volumes being accepted at the weekly Treasury bill auction, with the weighted averages continuing to edge up further and the foreign holding in Rupee bonds continuing to decrease by a further Rs. 1.8 billion, recording its sixth consecutive week of outflows.

Rupee continuesto dip further

Meanwhile in Forex markets, the USD/LKR rate on active spot next contracts depreciated further during the week, to close the week at Rs. 148.95/00 against its previous weeks closing level of Rs. 148.70/80 on the back of continued importer demand. The daily USD/LKR average traded volume for the first four days of the week stood at $ 47.46 million. Some of forward dollar rates that prevailed in the market were one month – 149.75/85; three months – 151.65/75 and six months – 154.30/40.