Wednesday Jul 01, 2026

Wednesday Jul 01, 2026

Monday, 4 July 2016 00:00 - - {{hitsCtrl.values.hits}}

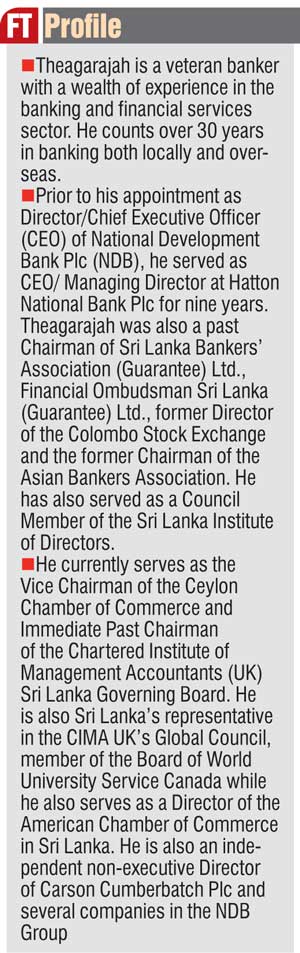

With interest rates on the rise, banks and their top strategists have been compelled to revise their game plan to remain on top. The unforeseen VAT increase, which has resulted in lower disposable income, is set to create waves within the banking industry if a platform to minimise its after effects is not created. To gain a better understanding about how National Development Bank Plc (NDB) is fairing in this area, the Daily FT recently sat down with its CEO Rajendra Theagarajah to discuss how he intends to overcome tough operating conditions to drive profitability. Following are excerpts from the interview:

NDB CEO Rajendra Thyagaraja

Q: What are your thoughts about NDB’s performance and key highlights and the way in which they were achieved?

A: The first quarter performance was below expectation given that we were relatively behind some of our peers. The reason for the lower than anticipated profitability in Q1 2016 was some one-off specific provisions made for few customers, based on sound judgement and objective evidence of impairment.

When you take that out for that particular industry, the NPL (Non-Performing Loans) of that particular category was just over 3% while the overall Gross NPL for the bank was 2.6%. While we are seeing margins compressing I think we are not short of opportunities for business itself. The real challenge is to steer through constantly declining margins and a highly competitive environment for deposits themselves because of two reasons; one being the industry itself is seeing a shortage of liquidity which means everyone is going after the same pool of money. Secondly, when interest rates are not what they were a few years ago, people try to allocate assets away from deposit. Some funds are shifting to investments such as Government Treasury Bills and Bonds, crowding out the private sector while others are moving towards real estate. However we believe that in every challenge there also lays an opportunity.

Although the growth NDB reported in Q1 2016 was below industry levels, we are on the precise trajectory towards achieving a full year 2016 performance which will be an improvement over 2015.

NDB has embarked on a new vision ‘to be the driving force for a financially empowered Sri Lanka’. This vision is complemented by our new mission to be the catalyst in the financial services industry by creating superior value for our shareholders and contributing to national development. This is driven by a simple tagline – ‘Our Commitment is Your Success’.

The bank’s performance is well aligned with these missions. Our unique business proposition of Development Oriented Commercial Banking has enabled us to reach out to individuals as well as SMEs and corporates, to empower them financially and assist them in developing their respective ventures. This proposition combines the age-old and perfected competence of NDB in development banking which it inherited from the inception, with the commercial banking stance which the bank took up around 2005. For us, commercial banking sans the development orientation is lacklustre. The excitement is in developing the individuals, the corporates and ultimately the nation, in the course of carrying out our business.

All of our business lines are highly motivated and committed to serving our clientele in this proposition. Our Project and Infrastructure Financing (PIF) Division, with its rich repository of knowledge and competence in funding long-term projects of medium to large scale continues its mission.

The PIF portfolio includes Agri value addition, aluminium can manufacturing, hydropower projects, thermal power projects, biomass projects, etc. During the last six months we have co-financed one of the largest investments by a local entrepreneur in a world-class canning venture to a multi-billion rupee water project giving clean water access to a township. These projects have made direct contributions toward national development, thus we are of the firm conviction that we are giving life to our mission to contribute towards national development.

The versatility of our PIF division has also been endorsed by the Asian Banking and Finance Magazine of Singapore, with the title of Best Project Financing Bank of Sri Lanka 2015.

Our development orientation encompasses individuals as well, because we firmly believe that you have to build individuals and their families to build the nation. As such, the developmental orientation reigns over our retail banking product portfolio as well. Be it our Shilpa children’s saving account, the Salary Max accounts/loans, our education loans or the home loans; we are committed to the sustained development of every Sri Lankan citizen who benefits from a meaningful array of our retail banking products.

Our offerings are not standalone products; they are complemented by a best-in-class service level at our branches and technology-enabled banking solutions such as mobile banking.

These may be the reasons why we were recognised as the Best Retail Bank for three consecutive years in 2013, 2014 and 2015, by the Asian Banking and Finance Magazine of Singapore which covers our industry.

Furthermore, in 2014 we grew our total asset base by 31%, almost twice as much as industry growth, followed by an 18% growth in 2015. Though numerically lower, the growth recorded in 2015 is also commendable. This was achieved in the aftermath of the substantial growth in 2014, where the bank tapped its potential to very high levels. Global Finance Magazine recognised NDB as Sri Lanka’s Best Bank in their Best Bank Awards for 2015. This recognition was particularly rewarding, having replaced a premier peer bank which had won this recognition for 16 consecutive years.

This is the immense potential that lies within NDB. We have what it requires to be better than the best. Our efforts are relentless in actualising these potentials and yielding sustainable benefits to all our stakeholders and our nation through improved performance and results.

Q: What are the bank’s targets this year for deposits, loans and profit growth?

A: I cannot mention specific numbers but I can say that from an overall results point of view we would certainly want to end the year better than last year. In terms of loans and deposits, we grew loans by 19% and deposits by 22% in 2015, where the deposits growth was better than the industry average. This year we expect the loan growth to be better than last year maybe something in excess of 20%. We expect that deposits will also grow at that pace. The challenge is at what cost you grow the deposits and at what price you grow your loan book. We are mindful of maintaining healthy margins and will not sacrifice our margins in pursuit of growth.

Q: The increase of VAT by 4% and the pressure on the rupee is going to spike up inflation which will in turn slow down disposable income growth. Market forecasters say this will slow down banking sector loan book growth to 18% from 25% in 2015. What are your thoughts on this and where does NDB stand at this juncture?

A: We saw this coming well in advance. Even though the absolute number is low, inflation has grown quite fast during the first half of 2016 compared to previous years. Internally, we have already started looking at some of the categories of loans or lending opportunities which can be more susceptible to inflation and balance that against the portfolio which is less vulnerable. If I can put it in another way, some of these loans are ‘nice-to-haves’ and some are ‘must-haves’ for the retail customer and I think what we are trying to do is shift the ‘nice-to-haves’ to ‘must-haves’.

We see moderation in the growth of products such as the ‘dream maker personal loan’ in an environment where consumption is challenged and inflation is spiking. One of the first areas which will be affected is consumption, which has to be managed. Therefore instead of pushing that product, for us, home ownership is still a very important aspect in Sri Lanka’s growth and it will continue to grow at a pace less than what it could grow at. We still believe that home ownership will not only improve asset quality at NDB but will also improve the resilience of the borrower.

If I look at NDB’s retail and SME segment, which tends to account for over 40% of the portfolio, we may see a greater emphasis on the SME element at the expense of more moderation in the retail element because with inflationary pressure we feel the SMEs which are more business-oriented will be more ‘need-to-have’ rather than ‘nice-to-have’ requirements.

On the other side in terms of project and infrastructure financing and corporate banking, the bank has an excellent pipeline through which working capital opportunities come. There may be some moderation in working capital but I don’t think in terms of overall growth it will slow us down. We currently don’t see a slowdown in our project pipeline.

Q: What new initiatives has NDB taken to increase profitability this year?

A: The key thing here is to look at four to five elements. One is to manage our portfolio quality while also growing the business and I think despite the one-off event which had an impact on our provisioning in the first quarter, our NPLs of 2.6% is one of the lowest in the industry and we are confident of defending it.

Secondly, if you look at the cost structure, the increase in operating expenses is well within our envisaged budget and at NDB it is not about cutting cost but managing cost, predominantly based on improved procurement. Furthermore, the costs are being managed while we have expanded our reach to over 100 plus branches in a very short period.

In terms of the revenue side you have two elements there. You have the pricing of the assets and the cost of funding. On the pricing side we have started our re-pricing already to reflect slightly upward movement in interest rates. The positive impact of re-pricing loans is already visible. On the liability side, yes as interest rates creep up so does the costs of funding. The only good thing about that is on the fixed deposits side it doesn’t jump overnight, sometimes till the contracts end. Approximately 70% of the bank’s portfolio is made up of fixed deposits.

What certainly has hurt us, like most other banks in the last few months, is that the element of borrowings from the money market where the rates have spiked up much more than the deposit costs. Our challenge has been to go into the market for deposits to reduce the money market borrowing element as much as possible so that we manage our overall average cost of deposits. Fee income has shown continuous and steady improvement. Trade finance has slowed down because of macro effects internal and external to Sri Lanka. Fees from bank assurance, credit and debit cards are growing though the composition may shift slightly. But the overall growth in fees is still in the right direction and is satisfactory.

In terms of the deposits side, our biggest challenge is to gradually increase the contribution of our savings and current accounts (low-cost deposits) as a composition of our total deposit base. It’s not an easy thing for a bank which has been in the commercial banking business for just over 10 years in mobilising public deposits, when you compare us with banks that are four to five times older than our bank.

This is challenging, however we are getting there. What I’m most happy about is that the newer branches we started in the last two to three years are taking that on board. This means we have to look at the cluster of the more mature branches which started originally as development-oriented branches, to shift some of those branches to be as agile as some of the newer branches. We have a relatively young pool of talent and we are rapidly introducing new technology by facilitating services such as mobile banking which we believe will take on the deposit mobilisation challenge.

Q: What’s the bank’s position when adopting international standards of reporting, capital adequacy provisioning and risk management?

A: If you look at IFRS I think NDB has been at the forefront and been conscious about international accounting standards. With the type of shareholding we have, which is not only locally held, and with the fact that we have been engaging with a number of multilateral lenders for years, it’s very important for us to maintain this stance in reporting. Therefore we have always been cognizant of having the understanding of accounting standards as close as possible to the West and rest of the world.

Advocating with the rest of the industry by helping to implement best in class financial reporting, we have been at the forefront. We are not scared of it; we see it as a positive correlation to our share price in the long run.

In addition to IFRSs, we have recalibrated our annual reporting to be in line with international integrated reporting guidelines. The bank’s sustainability reporting is in accordance with Global Reporting Initiatives – GRI G4 version. We continually review our reporting methods and ensure that our practices are updated and best in class such that our stakeholders better understand who we are through our reports.

If you look at capital adequacy, in fairness to the local regulator when the draft regulations came there was a sort of a realisation that local banks should do a ‘what if’ scenario which I think all the banks did some three years ago to see how they would manage this journey in creating those buffers. I think most banks have ratios today which are well above what’s currently regulatory prescribed as well as buffers which are regulated.

If you look at capital adequacy, in fairness to the local regulator when the draft regulations came there was a sort of a realisation that local banks should do a ‘what if’ scenario which I think all the banks did some three years ago to see how they would manage this journey in creating those buffers. I think most banks have ratios today which are well above what’s currently regulatory prescribed as well as buffers which are regulated.

You can look at risk management firstly as a minimum to have secondly by creating a framework which is proactive and not reactive and something that will help us to take on more and more business in a sound and manageable manner. NDB has always been at the forefront of designing a robust risk management framework and continually reviewing that framework to support the business.

Q: The bank’s impairment charge has significantly increased during the first quarter. What sort of strategies are in place to minimise such losses?

A: We have an internally developed board approved framework for collective impairment for smaller loans. We have a process which is embedded in a board approved policy regarding how we identify impairment on specific loans. That policy gets reviewed regularly by the board and is also subjected to external input. We believe that this framework gives us the tools to be proactive.

Having said that about impairment, it is also important to mention that NDB has in place a very strong credit review process, which evaluates the level of the risk the bank is assuming in doing its business. This review process is further strengthened by a post disbursement monitoring process and a recoveries process, to ensure the quality of our portfolio.

As was mentioned before, the increase in impairment charges in Q1 2016 was due to a few specific customers. For what it’s worth, these customers have maintained many years of healthy relationships with the bank, having serviced their commitments satisfactorily. Certain institution-specific as well as macroeconomic conditions have caused rough times for them. The same prevails for the future, where today’s prime customers may encounter difficulties in the times to come. This is the inevitable nature of businesses, which we have very well understood and have incorporated in designing our lending strategies.

Q: You speak about the importance of CASA repeatedly. However market forecasts show that growth in this segment is sluggish as customers are increasingly moving towards fixed accounts. How geared is NDB to face this challenge?

A: We are very mindful about this. Saying that it’s a relative thing if the industry finds itself in a difficult situation, so be it. However, you can do two things. Firstly, see if you can get something slightly above average because you’re offering something different in terms of better customer service and engagement, such as our mobile banking app which we launched recently. The experience will give better reasons certainly on the retail side to keep more money in the savings and current account due to convenience. Certainly there is increasing emphasis being put on the SME sector in trying to position NDB as the preferred small business banking provider and that brings in a different element of CASA. We are mindful that the institutional and the big ticket savers are very rate conscious and they are not going to keep stuff there. However, another thing we have done recently is that we have attracted the higher volume guys by saying we know that you’re not going to keep everything here but here is one area we will help you and help ourselves in capturing the need for wealth management and still keep as much as possible, a minimum amount of money in your current and savings accounts, by launching NDB ‘One Account’.

It is still unique for Sri Lanka where you have a money market, unit trust, wealth management proposition embedded into a savings or current account and a credit card in a commercial bank. All you have to do is keep that minimum amount and you have an automatic position to a different account which can be operated as either a money market movement account, unit trust account or fixed deposit; you decide depending on your risk appetite. At the same time it can be used literally as a current account where you encash it on demand without a penalty. Our strategy of leading the converged retail banking and wealth management space is well under way and this vertical is expected to be a strong contributor, going forward to building our CASA.

Furthermore, NDB’s savings campaign is rooted in the philosophy of ‘Ithuru Karana Maga’ or ‘The Path to Save’. This unique proposition, which has stretched itself beyond pure business orientation to create a more conducive lifestyle for our customers through responsible savings, has made a considerable contribution towards improved CASA within the bank. In just over 10 years of accepting deposits from the public, we today enjoy the benefit of having approximately 25 cents of every 1 rupee mobilised in deposits as a savings or current account balance.

Q: What’s your prediction for the interest rate scenario for the next six months given that interest rates have already gone up 340 basis points since the beginning of 2016?

A: I’m not a policymaker but the way we read things as long as the liquidity remains like this there will be gradual continuation of the increase of interest rates. However, saying that, there are a couple of things we hear from the policymakers and what is publicly available.

We hear about an IMF restructure or pool of money coming in, obviously it doesn’t come free of charge, it comes with certain terms. Nevertheless, as long as those terms are conducive to improving fiscal discipline and more consistent monetary policy I think it will be in the right direction. We believe that as a country we may need some additional funding and the recent announcement regarding the appointment of four international banks for a sovereign bond issue will probably have some insulating effects as far as liquidity is concerned. Given that most of these will be short-term measures on the other hand if you look at what was spelt out two years ago when this Government came into power one of the main things they recognised was that one cannot continuously depend on debt to anchor the growth of a country.

We hear about an IMF restructure or pool of money coming in, obviously it doesn’t come free of charge, it comes with certain terms. Nevertheless, as long as those terms are conducive to improving fiscal discipline and more consistent monetary policy I think it will be in the right direction. We believe that as a country we may need some additional funding and the recent announcement regarding the appointment of four international banks for a sovereign bond issue will probably have some insulating effects as far as liquidity is concerned. Given that most of these will be short-term measures on the other hand if you look at what was spelt out two years ago when this Government came into power one of the main things they recognised was that one cannot continuously depend on debt to anchor the growth of a country.

Two things this Government recognised in its policy statement are the importance of continuous FDIs and a sustainable export-driven strategy which will improve the diversification of export markets and drive it with competitiveness rather than depending on a depreciating rupee. Again the success of those two policy initiatives will I’m sure have a clear impact on the way domestic interest rates will eventually move in the medium to long term, whereas in the short term we see an upward stride.

Q: What are your sentiments on the behaviour of the NPL (Non-Performing Loan) ratio for 2016 given that as interest rates go up asset quality declines?

A: Yes and not so yes. If we look at interest rates in the past 10 years and if you look at NDB’s NPLs before 2013 there were times when your typical treasury bill rates which may have been in the middle 10s as opposed to it going down below 10 but even during that era the bank had a NPL percentage of less than 2%, well below the industry. Therefore yes while you may have a general correlation it doesn’t mean it’s specific to any particular bank.

The second thing is also yes, interest rates will go up but it doesn’t mean that every aspect of a borrower gets impaired because there are those who borrow to consume probably have a greater propensity to get into difficulty with irresponsible spending than perhaps people who borrow because they have a need to spend. When interest rates are one element as a cost of funding/borrowing, on the other hand if an intelligent borrower borrows and as part of inflation re-prices his/her own business intelligently this can be managed. The question is how well we manage portfolio quality versus business growth. We are confident that the internal processes in place have in the past and will continue to give us the agility of doing so.

Increasing interest rates is a business opportunity which the banks should embrace. It is not a situation from which you should shy away on the premonition that borrowers will not honour their increasing commitments. Customers who borrow for spending on essentialities should demonstrate financial intelligence to manage their expenses and make sufficient provisions to meet their financial commitments.

Q: What are your thoughts on banking sector consolidation?

A: Well I have always been vocal about consolidation being good for the industry and the country. This is not for the sake of consolidation but because it certainly has showed the world that it brings in an element of efficiency, sharpness and reallocation and the revisiting of limited resources. Saying that, it cannot be forced on people, it has to be voluntary.

All we can say is that for NDB, organic growth is our bread and butter and I don’t think that detracting our attention from this at the expense of trying to do consolidation is the answer. As a team we are mindful of opportunities for consolidation and believe in preparing ourselves and shaping our mindset to embrace it if it comes knocking with the right terms and right price instead of being shocked into it.

Q: What are your prospects for NDB’s SME and microfinance banking segment?

A: SMEs have been identified as the backbone of Sri Lanka’s economic prosperity. We have embedded this stance into our own SME strategy; more strikingly, not since the recent past, but since our origin.

Empowering SMEs and the development of rural economies have been spelt out in our inaugurating purposes as well. So of course originally the focus was to get into project-oriented lending for SMEs and now over the last 10 years having being converted into a full-scale commercial bank the real opportunity is to link the working capital requirements also with project lending and support an SME in its entire evolution and the entire value chain.

Along with that comes the opportunity on account of the SME playing a pivotal role on both ends of the spectrum; at the very top with the large local corporates and the multinationals to see as to how you plug in.

The bank itself has a tremendous opportunity of being originally a more wholesale centric bank with very good business developed over the years with the MNCs as well as the large exporter corporate community to be able to assist the SMEs to scale up.

When getting into microfinance if you look at what we call entrepreneurial poor and not the labour poor, people keep on lamenting and saying that there isn’t much done on the microfinance front and you cannot do much because there is no collateral base for these people. I think the way NDB has prided itself in handling this area is we do recognise that we don’t have the bandwidth of trying to empower every micro entrepreneur in every part of the country and there is cost to it as well.

The bank has not just gone and said here’s a loan and a concessionary rate of interest now you repay because we believe that what those people need more is handholding advice, responsible saving and access to markets.

A few segments of the Sri Lankan population that are direct beneficiaries of NDB’s financial inclusion endeavours are female apparel industry workers, the mobile food vendors at Galle Face Green, small-scale floriculturist and seed paddy farmers in villages like Giridamana. The stories of these people as to how they have prospered in their lives through the carefully structured financial products offered by NDB is strong affirmation of the lasting impact the bank is making through its financial inclusion endeavours.

What is more is that some of these initiatives will take into consideration the pragmatic restrictions faced by these segments in banking. For example, female factory workers are not able to visit the bank during work hours hence our teams visit them at their factory premises during their breaks thus providing a doorstep service. Such initiatives have largely reduced the reliance of the unbanked population on informal moneylenders and have rooted them in the formal banking streams.

Furthermore, our SME endeavours are strategically thought out and executed, such that we empower the entirety of the value chain of the benefiting industries. Hence not only the individual links of the value chain but the full industry or segment prospers through formal financial assistance. The best example NDB can quote for such total value chain financing is its initiative targeting the cinnamon industry in Sri Lanka, named ‘Cinnamon to the World’.

Having said that about ourselves, I would also like to make reference to what others think about us. The Banker Magazine of UK, which covers our industry globally, recognised NDB as the sole global awardee for financial inclusion in 2014, for NDB’s efforts in ‘Cinnamon to the World’. This was indeed a great feat for the bank and all its stakeholders as the award is bestowed on a single bank chosen from across the globe.

The Asian Banking & Finance Magazine of Singapore has recognised NDB for three consecutive years since 2013 as the Domestic SME Bank of the Year for Sri Lanka, again affirming the sustainable impact our endeavours have created.

Q: Will we be able to see fresh debenture issues in the near future?

A: It’s still too early to say as far as our debenture strategy is concerned. In 2013 we raised Rs. 10 billion via a listed debenture, the largest quantum of money a single corporate had raised via a debenture issue in the country. We had another debenture issue in mid-2015. Who knows maybe with the growth we will look at it but at this juncture I don’t see it happening any time soon.

On the flipside, that is issuing debentures for other corporates in our capacity as an investment bank, our wholly-owned subsidiary company NDB Investment Bank Ltd. (NDBIB) is well geared towards this as the undisputed market leader in Sri Lankan investment banking. Speaking of NDBIB, we are proud to acknowledge that NDBIB has been recognised as the best investment bank in Sri Lanka for four consecutive years from 2012 to 2015 by the Euromoney Magazine of the UK.

Q: As a veteran banker and someone who has seen the financial system’s ups and downs what are your views about the Government’s economic policy and its impact on the financial system of the country?

A: For me what I saw as positive in this regime is the willingness for open communication and to say here is a policy framework. What now remains as a challenge and also as an opportunity is to what extent those policies will be implemented consistently and to what extent will the impact of these policies be assessed and made available to the public in a transparent manner.

Two things which I personally felt important were firstly the recognition of the importance of education in the future of Sri Lanka and the ability to plug economic growth with employment and education curriculum. This is a very relevant policy to upskill the present and next generation of youth.

The second area which we certainly welcome is the fact that we recognise a whole geographic area from the South of Colombo to the North of the airport what we believe can hold up to five million people and call it the western megapolis. We now have, from the view of local and foreign businesses, a slated framework available to say that this is the planned urbanisation of a super megapolis. Any of you want to come in and invest, this is the framework, thus you cannot do things arbitrarily in a haphazard manner damaging the environment and also you can pick your sweet spot, let it be public-private partnerships, private investments or what you chose it to be. That I think is a good thing even though there’s a lot more work to be done.

What all of us must understand is that the megapolis will not be achieved overnight. The full completion of this project will take at least a decade. Hence it also involves a lot of patience to see the ultimate results. But the well spelt out plans in place with promising potential, which connect public enterprises, private enterprises and leads to collaborative public-private partnerships alone is encouraging. What is important now is the execution of these plans. It also gives NDB as a bank an opportunity to harness our resources for the next few years.

Q: NDB is expanding its branch network aggressively this year and opened its 100th branch recently. Are there any plans for a new branch opening? Have any locations been earmarked?

A: We opened our 101st branch in Warakapola on 10 June and on 15 June we opened our 102nd branch at Thambuththegama. They are all in agri-belt areas outside the Western Province. We will open a few more branches, maybe a total of 15 new branches for this year. Most of them will be out of the Colombo region because we believe that more and more inclusion and opportunities to engage with SMEs lie in these areas.

Why we thought we should establish ourselves in these areas is even though there is a belief that 30% of the workforce is contributing to 10% of the GDP in agriculture, there are pockets there that if correctly harnessed are able to contribute to the agri value chain significantly. NDB, as a bank focused on development-oriented commercial banking, can really plug into this agri chain and provide a meaningful solution to middle-class Sri Lanka.

Q: Going forward what can you say about the stability of the bank?

A: NDB is governed by a robust corporate governance framework and risk management strategy. The bank is steered by the able and competent leadership of a board of directors who bring to the table an amalgam of rich experience and competencies of many years in multiple sectors. The bank’s business is based on a carefully articulated five-ear strategy, which I may say is efficiently executed by the management and the employees of the bank. The bank’s top management is also a dynamic fusion of talent and capabilities, and includes some who carry many years of experience with NDB and others who are relatively new, bringing in new knowledge and experience of their own.

We uphold a set of corporate values in all of what we do, those values being integrity, excellence, creativity, accountability and sincerity. NDB has always looked at the safety of the depositors and the importance of a sound, robust balance sheet along with a risk management culture as the underpinning foundations of growth. We believe that those foundations will be nurtured and continued without disruption. The only difference will be that we will keep on loading more and more business onto that framework.

Pix by Upul Abayasekara