Friday Jul 03, 2026

Friday Jul 03, 2026

Tuesday, 5 January 2016 00:03 - - {{hitsCtrl.values.hits}}

In a pioneering move, MBSL constructed a stock market index: the ‘MBSL MIDCAP Index’, which measures the aggregate price level and price movements of medium size companies listed on the Colombo Stock Exchange (CSE). The index which came into operation in the year 1999 is revised annually and looks at the Middle Range Market Capitalisation, Liquidity and the Profitability of the firms to be included in the MBSL MIDCAP Index.

Benefits of the MBSL MIDCAP Index

MBSL MIDCAP Index can be used as the benchmark index by individual and institutional investors who prefer growth but are prepared to withstand only conservative levels of volatility in their equity investments.

It can be used as the benchmark index for the introduction of MBSL MIDCAP linked index funds.

MBSL MIDCAP Index generates valuable signals for portfolio managers for switching from larger-cap more sensitive stocks to midcap less sensitive stocks with more growth potential in response to changing capital market conditions. The MBSL MIDCAP Index focus in profitability helps to screen stocks with better future prospects that will cross to higher market capitalisation in the coming year.

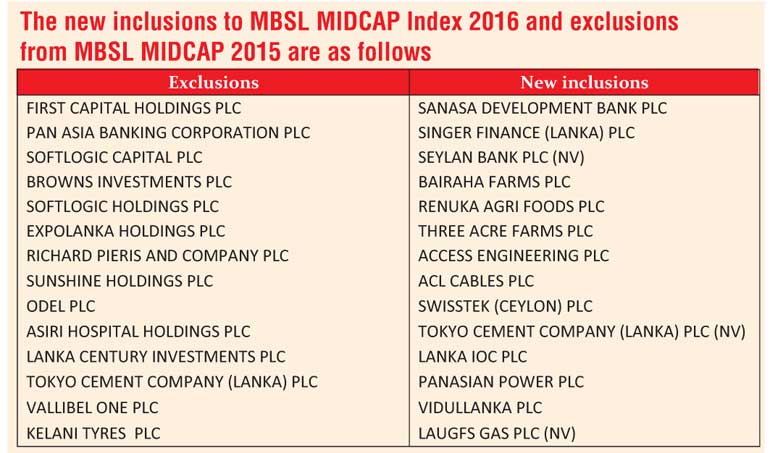

MBSL MIDCAP Index which is in effect from 1 January 2016 and the criteria for selecting the 25 stocks of the index remained unchanged. They are:

Accordingly the range of market capitalisation for the year 2016 is Rs. 2.57 billion-Rs. 25.7 billion.

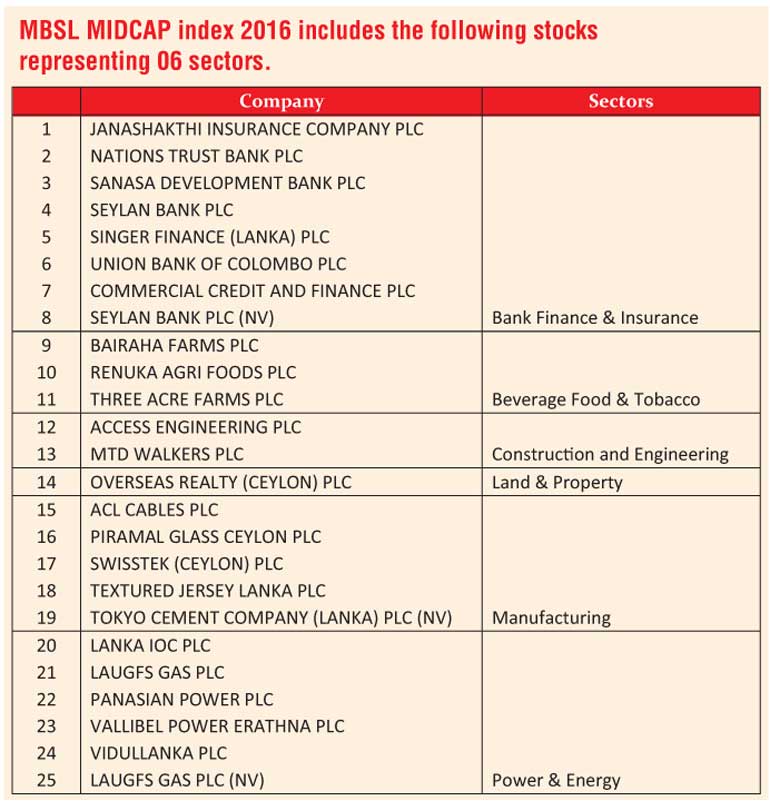

Based on the above criteria the MBSL MIDCAP index 2016 includes the following stocks representing six sectors.