Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 11 July 2017 00:00 - - {{hitsCtrl.values.hits}}

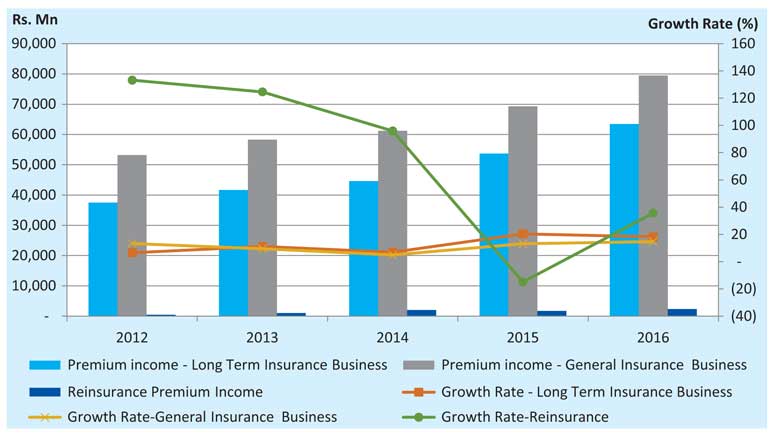

Premium income and growth rate

The Sri Lankan insurance industry continued its growth during the year 2016. The industry recorded growth in Gross Written Premium (GWP) of both Long Term and General Insurance business sectors. The total GWP income for both sectors in 2016 was Rs. 142,969 million compared to Rs. 122,962 million in 2015 reflecting a growth of 16.27%.

The long term insurance sector generated GWP amounting to Rs. 63,495 million in 2016, up by 18.26% against the GWP of Rs. 53,691 million generated in 2015. This significant growth was attributable to factors such as increased awareness on life insurance, introduction of new life insurance products to cater dynamic customer requirements such as retirement solutions and investment products, enhanced customer service, etc.

The general insurance sector recorded GWP amounting to Rs. 79,474 million in 2016, posting a growth of 14.73% compared to Rs. 69,271 million recorded in 2015. General insurers were able to increase their premiums steadily year on year amid strong competition prevailing in the general insurance market by means such as focus on niche markets, introduction of innovative general insurance products, implementing Enterprise Risk Management strategies, focusing on risk selection and pricing, etc.

The reinsurance premium income generated by the National Insurance Trust Fund (NITF) from the compulsory reinsurance cession of general insurance business amounted to Rs. 2,357 million during 2016, recording a significant increase of 35.62% against the reinsurance premium of Rs. 1,738 million generated in 2015. NITF’s reinsurance premium has risen substantially in 2016 mainly due to acceptance of reinsurance business from a wider range of different classes of general insurance business.

Insurance penetration and density

Insurance penetration which reflects the insurance premium as a percentage of GDP amounted to 1.21% in 2016. Although insurance penetration had increased in 2016 compared to 2015 which was recorded as 1.12%, it is still low compared to most of the other countries in the Asian region. Penetration of the long term insurance business in 2016 stood at 0.54% (2015: 0.49%) and the penetration of the general insurance business was 0.67% (2015:0.63%), both classes recording slight increases compared to the penetration ratios recorded in 2015.

Insurance density reflects the insurance premium income per person of the population and has increased to Rs. 6,743 million in 2016 compared to Rs. 5,865 million recorded in 2015, growing by 14.97% mainly due to increased premium income against lower increase in population.

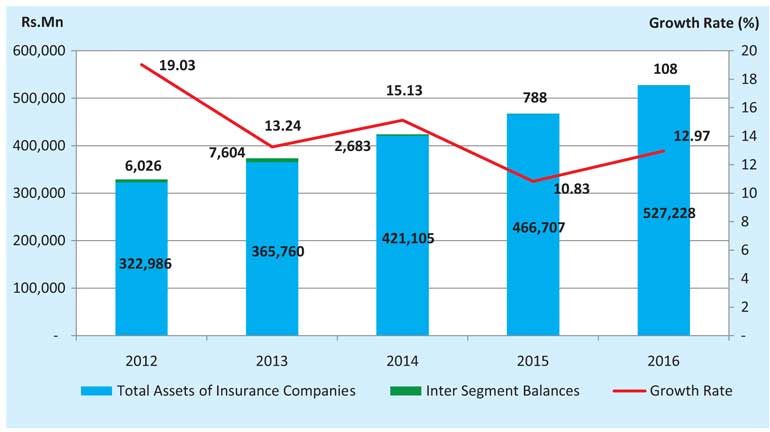

Total assets

Total assets of the insurance industry (after eliminating inter segment transactions) which comprise of theassets belonging to long term and general insurers and the national reinsurer, NITF have amounted to Rs.527,228 million as at 31December 2016. This was an increase of 12.97% compared to the assetsamounted to Rs. 466,707 million recorded as at 31December 2015.

Long term insurers held the majority of total industry assets which amounted to Rs. 345,675 million as at31December 2016 (2015: Rs. 312,713 million). Assets of long term insurance business recorded agrowth of 10.54% in 2016 compared to 2015. Assets of general insurance business amounted to Rs.175,745 million as at 31 December 2016 (2015: Rs. 151,177 million) and recorded a growth of 16.25%.

NITF held assets amounting to Rs. 5,915 million as at 31December 2016, belonging to reinsurance business recording a significant growth of 64.12% compared to assets recorded as at 31December 2015, which amounted to Rs. 3,604 million. The above mentioned increases in assets were mainly attributable tothe growth in the premium income of long term and general insurance and reinsurance businesses whichhave resulted in the expansion of the asset base of insurers and NITF.

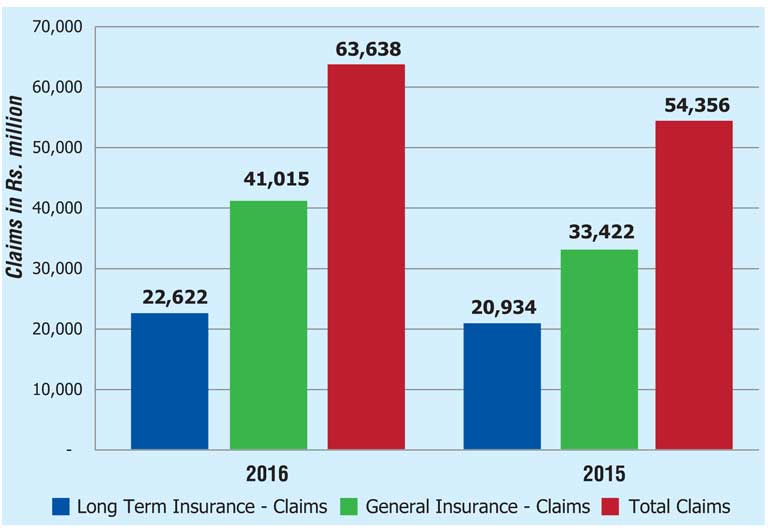

Claims incurred by insurance companies

The claims incurred by insurance companies in both Long Term Insurance Business andGeneral Insurance Business was Rs. 63,638 million (2015: Rs. 54,356 million) showing an increase in total claims amount by 17.08% year-on-year. The Long Term Insurance claims, including maturity and death benefits, amounted to Rs. 22,622 million (2015: Rs. 20,934 million). The claims incurred in General Insurance Business, including Motor, Fire, Marine and other categories, amounted to Rs. 41,015 million (2015: Rs. 33,422 million). Hence, during 2016, there is an increase in claims incurred by 8.07% and 22.72% for Long Term Insurance and General Insurance Businesses respectively, when compared to 2015.

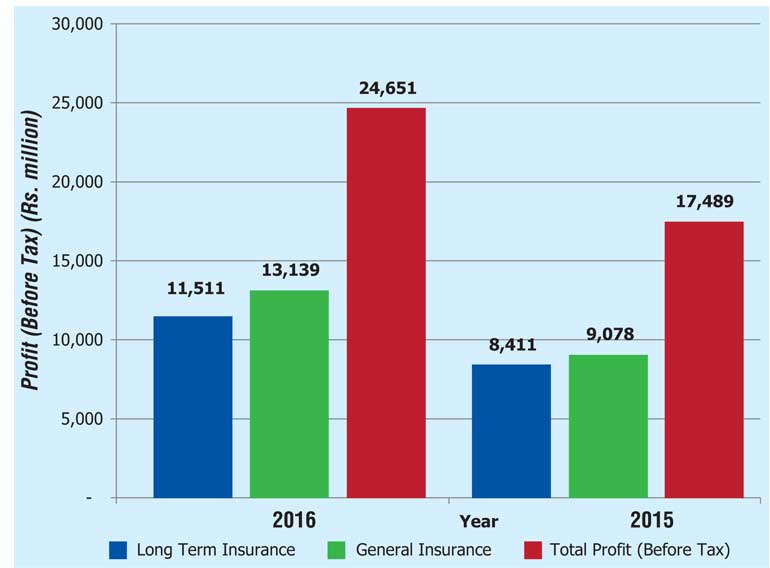

Profit (before tax) of insurance companies

The profit (before tax) of insurance companies in both Long Term Insurance Business andGeneral Insurance Business has increased to Rs. 24,651 million (2015: Rs. 17,489 million) showing a remarkable growth in profits by 40.95%. The profit (before tax) of Long Term Insurance Business amounted to Rs. 11,511 million (2015: Rs. 8,411 million) while the profit (before tax) of General Insurance Business amounted to Rs. 13,139 million (2015: Rs. 9,078 million) during the year. Thus, profit (before tax) of Long Term Insurance Business and General Insurance Business witnessed a growth of 23.72% and 44.74% respectively, when compared to 2015.

Dispute resolution and Investigations

IBSL, under its overall objective of safeguarding the interests of policyholders, inquires into policyholders’ grievances in connection with insurance claims pertaining to life and general insurance policies. IBSL also investigates into any other complaint referred to it against any insurer, broker or agent. During 2016, 353 new matters were referred to the Board. A total of 345 matters were settled/closed during the period. Aggregate value of the claims settled during the period, due to the intervention of the Board, is around Rs. 21.5 million.

Insurers

Out of 28insurance companies (insurers) operating as at 31 December 2016, 12 companies carry on only Long Term Insurance Business,13 companies carry on General Insurance Business and three are composite companies (dealing in both General and Long Term Insurance Businesses).

Insurance brokers

Fifty-eight insurance brokering companies, registered with the Board as at 31 December 2016, mainly concentrate in General Insurance Business.

The premium income generated through General Insurance Business indicates the importance of brokers as an intermediary in the General Insurance market. However, insurance brokers’ contribution towards Long Term Insurance Business was insignificant in 2016 as witnessed in previous years. The premium income generated through Insurance Brokering Companies with respect to General Insurance Business amounted to Rs. 17,519 million (2015: Rs. 16,124 million) while the premium income generated with respect to Long Term Insurance Business amounted to Rs. 263 million (2015: Rs. 206 million).

The total premium income from both General Insurance Business and Long Term Insurance Business amounted to Rs. 17,782 million during 2016, compared to Rs. 16,330 million during the previous year. Thus, the total premium income generated through insurance brokering business witnessed a growth of 8.89% year-on-year. However, the brokering companies’ contribution as a percentage of the total GWP has dropped to 12.44% from 13.28% recorded in 2015. (Source: Insurance Board of Sri Lanka)

Footnotes

2016–Provisional Figures.

Assets –Intersegment transactions (i.e. transactions between Long Term and General Insurance segments) have been eliminated.

The assets belonging to life shareholders of SLIC and Sanasa have been reported under general insurance.

Income and assets of Crop & Loan Protection scheme of NITF have been eliminated from the computation of industry statistics.