Tuesday Jul 14, 2026

Tuesday Jul 14, 2026

Monday, 26 October 2015 00:00 - - {{hitsCtrl.values.hits}}

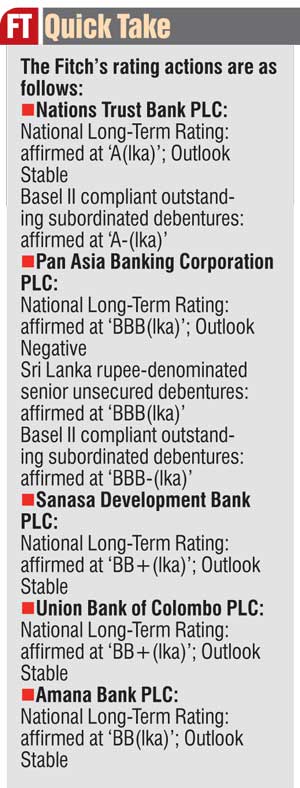

Fitch Ratings has affirmed the National Long Term Ratings on five small and mid-sized Sri Lankan banks. Nations Trust Bank PLC (NTB) has been affirmed at ‘A(lka)’, Pan Asia Banking Corporation PLC (PABC) at ‘BBB(lka)’, Sanasa Development Bank PLC (Sanasa) at ‘BB+(lka)’, Union Bank of Colombo PLC’s (UB) at ‘BB+(lka)’ and Amana Bank PLC (Amana) at ‘BB(lka)’. A full list of rating actions is at the end of this commentary.

Fitch Ratings has affirmed the National Long Term Ratings on five small and mid-sized Sri Lankan banks. Nations Trust Bank PLC (NTB) has been affirmed at ‘A(lka)’, Pan Asia Banking Corporation PLC (PABC) at ‘BBB(lka)’, Sanasa Development Bank PLC (Sanasa) at ‘BB+(lka)’, Union Bank of Colombo PLC’s (UB) at ‘BB+(lka)’ and Amana Bank PLC (Amana) at ‘BB(lka)’. A full list of rating actions is at the end of this commentary.

The ratings are all based on the banks’ intrinsic strengths. The main development affecting their business profiles is the banks’ initiatives to expand their small franchises. The banks’ unique business models have led to growth in different areas. While UB has shifted to larger corporates, the other banks are more focused on the SME and retail segments. All of their loans grew faster than that of the overall banking sector, resulting in continued decline in their capital ratios. The capitalisations of NTB, UB and Sanasa have remained satisfactory, but Amana and PABC have yet to maintain capital of at least Rs. 10 billion, which would be required by 1 January 2018.

The NPL ratios of the banks have been decreasing. This has been largely a function of the strong growth in loans, which could lead to asset-quality pressure as the loan book seasons. The banks’ deposit franchises are weak in relation to more established banks and all except Amana have a small share of current and savings accounts (CASA) in the deposit mix.

Key rating driversNational ratings and senior debt

NTB’s ratings reflect its expanding franchise, improved efficiency and its high and increasing exposure to products and customer segments that are more susceptible to economic cycles.

The bank’s SME and retail exposure increased to 25% of gross loans at end-June 2015 from 12% at end-2010. Consumer lending continued to account for a large portion of NTB’s loan portfolio, with leases accounting for 27% of gross loans while credit cards and personal loans together accounted for a further 22% of gross loans at end-June 2015.

Fitch believes that these exposures could put pressure on NTB’s asset quality. Its reported gross NPL ratio was 4.02% at end-June 2015 and 4.14% at end-2014 (end-2013: 3.51%), with leasing NPLs accounting for an increasing share. The ratio of the bank’s reserves for impaired loans to gross loans was 2.26% at end-June 2015, which remained lower than that of its peers.

CASA accounted for 32% of overall deposits, which Fitch expects to remain lower than that of higher rated peers, although this has increased from the 26% at end-2013, driven by the recent branch expansion.

PABC’s rating reflects improving but still-weak asset quality relative to higher-rated peers, its moderate franchise and improving profitability. The Negative Outlook on PABC’s rating reflects continued deterioration in its capitalisation amid rapid loan growth. Fitch believes that PABC’s aggressive growth could put pressure on asset quality over the medium term, even though the bank’s NPLs have declined. ROA improved to 1.1% at end-June 2015 from 0.6% at end-2014 due to expansion in net interest margin (NIM) and improved cost-to-income ratio.

PABC’s senior debentures are rated in line with its National Long-Term Rating of ‘BBB(lka)’, as they rank equally with the claims of the bank’s other senior unsecured creditors.

Sanasa’s rating captures the bank’s high exposure to the retail and lower-end SME segments and its weak asset quality, which are counterbalanced by above-average NIM stemming from its high-yielding loan book. Fitch believes that Sanasa will need a capital injection as internal capital generation will likely remain insufficient to support strong loan growth. The slight improvement in its reported gross NPL ratio to 3.2% at end-June 2015 from 3.8% at end-2014 stems from rapid loan growth and Fitch expects asset quality to deteriorate as the loans season.

UB’s rating reflects ongoing structural improvements, a still-small franchise and higher capitalisation compared with that of its peers. Fitch expects capitalisation to gradually decline over the next 12-18 months to levels more comparable to that of its peers, but believes that it could sustain stronger capitalisation in the medium term than in the past. Its Fitch Core Capital ratio decreased to 29.1% at end-June 2015 after being boosted to 35.8% at end-2014 following an LKR11.4bn capital injection from an affiliate of Texas Pacific Group (TPG). UB’s profitability is low with an ROA of 0.3% at end-June 2015 and Fitch believes that the low internal capital generation may not keep pace with rapid loan growth.

Fitch believes UB’s risk profile has improved following a shift towards loans to larger corporates from SMEs, which are more vulnerable in economic downturns, and better risk management. This could support better asset quality than in the past. There has been a sharp decline in UB’s reported gross NPL ratio to 4.87% at end-June 2015 from 8.25% at end-2014. This figure excludes NPLs at its subsidiary UB Finance, which remained significant and accounted for 33.5% of the groups’ total NPLs at end-June 2015.

The rating on Amana, which is a Sharia-compliant bank, reflects its still-small and developing franchise and short operating history. The rating also captures the bank’s relatively high risk appetite, which is evident in the rapid growth in retail and SME segments, which could result in pressure on asset quality as the loan book seasons. Liquid assets are mostly placements overseas as the bank cannot invest in domestic government securities, which are not Sharia-compliant. The deterioration of its capitalisation weighs on its rating. Amana’s profitability metrics have improved with ROA reaching 0.4% in 1H15 from -0.27% in 2014.

Subordinated debt

NTB’s and PABC’s subordinated debentures are rated one notch below their National Long-Term Ratings to reflect the subordination to senior unsecured creditors.

Rating sensitivitiesNational ratings and senior debt

NTB’s rating may be upgraded if it demonstrates progress in building a strong commercial banking franchise with enhanced funding stability, improved capitalisation and asset quality levels that are in line with higher-rated banks. An increase in risk appetite and rapid expansion in segments that are susceptible to economic cycles could result in a rating downgrade. This may be evident through aggressive loan growth or loan pricing that may lead to weaker asset quality or capital levels.

PABC’s rating would remain at the current level if it is able to significantly and sustainably improve its capitalisation, mostly likely through a timely capital infusion and slower growth in its loan book. Failure to materially improve its capital ratios or indications of a higher risk appetite would result in a downgrade. The rating of PABC’s senior debt will move in tandem with PABC’s National Long-Term Rating.

Aggressive loan growth that could increase Sanasa’s capital impairment risks, either through greater unprovided NPLs or a continued deterioration in capitalisation, could lead to a downgrade. An upgrade would be contingent upon fundamental improvements in its asset quality and moderation of its risk appetite alongside asset growth.

The upgrade of UB’s rating could stem from a sustained improvement in its asset quality, sustainable and improved earnings, moderation in its risk appetite and a stronger franchise. Capital impairment risks stemming from sustained rapid loan expansion or deterioration in asset quality could pressure UB’s rating.

Fitch would downgrade Amana’s rating if the bank fails to maintain adequate capital levels relative to risk-weighted assets that are commensurate with its above-average loan growth and lower provisioning for NPLs. A rating upgrade is contingent upon the expansion of Amana’s franchise and improved and sustained performance to levels similar to higher-rated peers.

Subordinated debt

NTB’s and PABC’s subordinated debt ratings will move in tandem with the banks’ National Long-Term Ratings.