Friday Jul 03, 2026

Friday Jul 03, 2026

Monday, 26 September 2016 00:01 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

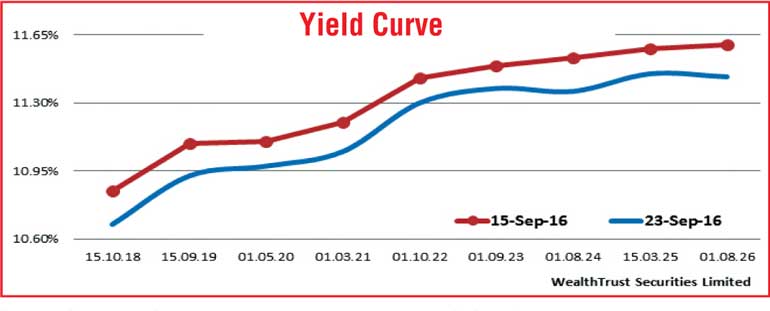

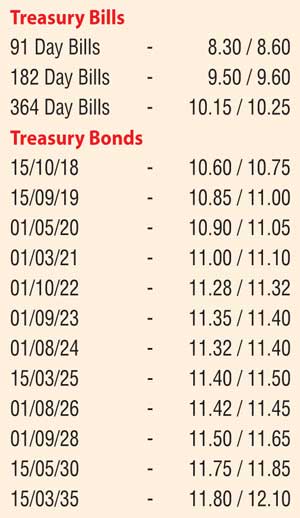

Activity in secondary bond markets increased considerably towards the latter part of the week, mainly on Friday as yields decreased due to substantial buying interest returning back to the market, reversing an upward trend that was witnessed during the beginning of the week. Trades were mainly seen on the liquid maturities of 15.10.18, 01.03.21, 01.10.22, 01.09.23, 01.08.24, 15.03.25, 01.08.26, 01.09.28 and 15.05.30 from weekly highs of 10.98%, 11.30%, 11.57%, 11.60%, 11.64%, 11.65%, 11.70%, 11.80% and 12.00% respectively to lows of 10.70%, 11.00%, 11.32%, 11.40%, 11.35%, 11.45%, 11.40%, 11.60% and 11.85% reflecting a parallel shift downwards of the overall yield curve on a week on week basis.

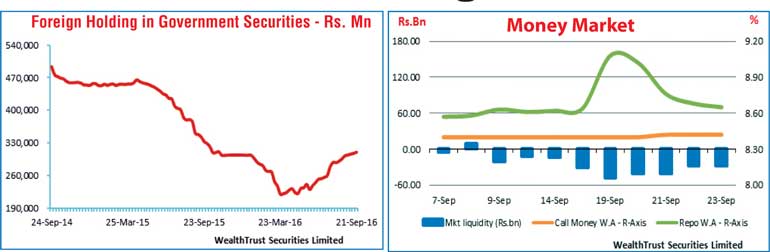

Furthermore, buying pressure on secondary bills was evident during the week as durations centring the 364 day maturity was seen trading at lows of 10.25%. This was fuelled by the outcome of the weekly Treasury bill auction, at where weighted averages decreased once again with the total accepted amount just falling short of the total the total offered amount of Rs. 16 billion. Meanwhile foreign buying of Rupee bonds which has been prevalent over the past six weeks, continued with an inflow of Rs. 2.6 billion for the week ending 21 September.

In money markets, overnight call money and Repo rates increased during the week to average 8.41% and 8.84% respectively as the net liquidity shortfall in the system increased to Rs. 37.33 billion in average against its previous weeks net shortfall average of Rs. 19.03 billion. The Open Market Operations (OMO) Department of Central Bank continuously infused liquidity by way of overnight Reverse repo auctions at weighted averages ranging from 8.48% and 8.49%.

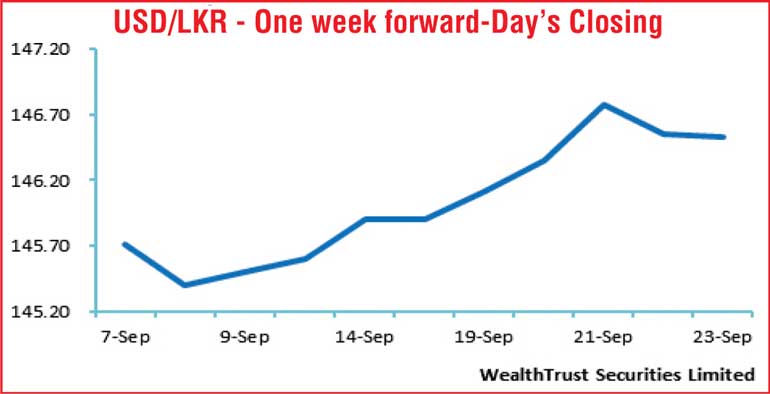

Rupee depreciates further during the week

The rupee on spot next contracts depreciated further during the week to close at Rs. 146.35/40 against its previous weeks closing level of Rs. 145.65/80 on the back of continued importer demand and foreign equity outflows outweighing foreign Rupee bond inflows and export conversions. Activity on Spot contracts reduced during the week.

The daily USD/LKR average traded volume for the first four days of the week stood at $ 40.43 million. Some of the forward dollar rates that prevailed in the market were one month – 147.10/25; three months – 148.80/00 and six months – 151.10/40.