Saturday Jul 04, 2026

Saturday Jul 04, 2026

Tuesday, 28 June 2016 00:05 - - {{hitsCtrl.values.hits}}

By Wealth Trust Securities

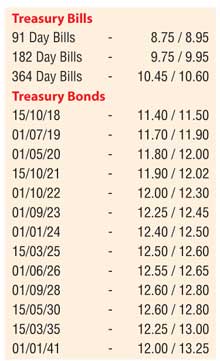

The four Treasury bond auctions conducted yesterday recorded impressive weighted averages well below market expectations with a total amount of Rs.23.9 billion been accepted against a total offered amount of Rs.30 billion.

The amount accepted on the 4.05 year maturity of 15.12.2020 and the 8.08 year maturity of 15.03.2025 was Rs.12.14 billion and 7.42 billion respectively against its offered amounts of Rs.10 billion and 6 billion while the remaining two maturities recorded accepted volumes below its offered amounts.

In secondary bond markets, yields decreased yesterday with the liquid maturities of 01.01.24 and 01.06.26 hitting intraday lows of 12.45% and 12.60% respectively against its previous day’s closing levels of 12.75/78 and 12.75/85. In addition on the short end of the yield curve, the 2019 maturities were seen changing hands within the range of 11.90% to 11.92% as well.

In money markets yesterday, overnight call money and repo rates remained steady to average 8.18% and 8.04% respectively as the Open Market Operations (OMO) department of Central Bank was seen injecting an amount of Rs.22.00 billion on an overnight basis by way of a reverse repo auction at a weighted average of 7.97%. The net liquidity shortage in the system stood at Rs.18.53 billion  with a further amount of Rs.15.52 billion been accessed from CBSL’s Standing Lending Facility Rate of 8.00% against a deposit amount of Rs.18.49 billion at its Standing Deposit Facility Rate of 6.50%.

with a further amount of Rs.15.52 billion been accessed from CBSL’s Standing Lending Facility Rate of 8.00% against a deposit amount of Rs.18.49 billion at its Standing Deposit Facility Rate of 6.50%.

Rupee depreciates further

The USD/LKR rate on the active one week forward contract was seen depreciating further yesterday to close the day at Rs.148.30/50 against its previous weeks closing of Rs.147.80/00 on the back of renewed importer demand. The total USD/LKR traded volume for the 24nd June 2016 was $ 59.65 million. Some of the forward USD/LKR rates that prevailed in the market were 1 Month - 148.85/05; 3 Months - 150.30/60 and 6 Months - 152.50/75.