Thursday Jul 09, 2026

Thursday Jul 09, 2026

Thursday, 27 February 2020 00:00 - - {{hitsCtrl.values.hits}}

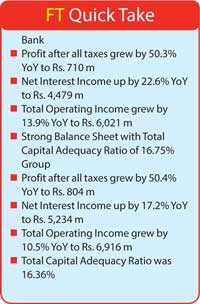

Union Bank said yesterday it demonstrated a healthy performance amidst the challenging macro-economic environment in the year 2019, recording a significant increase of 50% in profit after all taxes.

Amidst sector shocks that prevailed throughout, the Bank strived for revenue optimisation through

|

Chairman Atul Malik |

|

Indrajit Wickramasinghe-CEO |

portfolio re-alignment and prudent cost management. During the year, the Bank had paid 66% of its profits as taxes which was over Rs.1 billion the Union Bank said in a statement.

Core Banking growth and Profitability

Despite market challenges, the core banking operations of the Bank performed consistently on the back of focused strategic initiatives implemented across Corporate, SME and Retail Banking segments, supported by an impressive Treasury performance. As a result of well- managed core banking operations, The Net Interest Income (NII) of the Bank grew significantly to Rs. 4,479 Mn, which was a YoY growth of 22.6%.

Net Interest Margin (NIM) for the year was 3.6%. NIM for the current period would have been 3.8% if the return from investments in units was considered. Return from investments in units was Rs. 227 Mn and was recorded as capital gains under “net fair value gains/ (losses) from financial instruments at fair value through profit or loss”.

Despite policy rate revisions, the demand for credit to the private sector remained subdued, affecting the balance sheet growth. The Bank’s loans and advances stood at Rs. 77,358 Mn and recorded a growth of Rs. 3,609 Mn, which was a 4.9% increase in comparison to the previous year. The growth was mainly attributable to the contribution from loans in the retail segment including a significant increase in the credit cards portfolio and the expansion of the Corporate loans portfolio.

The deposits base of the Bank stood at Rs. 76,532 Mn as at year end. The Bank’s strategic focus was shifted towards acquisition of low-cost deposits which requisitioned a strategic re-alignment of the deposits base.

The growth momentum of CASA (Current and Savings Accounts) was continued throughout the year, with focused expansion of key products. As a result, the CASA base grew to Rs. 19,332 Mn by year end. The average CASA portfolio growth was 16% YoY while the CASA Mix of the Bank improved to 25%.

The Bank’s well executed strategic initiatives for fee income were continued throughout the year and produced a fee and commission income increase of Rs. 101 Mn which was a 10.5% growth YoY. This was mainly attributable to income generated from a significant increase in credit cards fees due to focused acquisition efforts, supported by an inflow of Bancassurance fees and guarantees’ income. Fee income was adversely affected by the drop in trade income due to the decline of imports and exports across the industry in 2019.

Net trading and other income was Rs. 686 Mn, and recorded a reduction of 14.2% over the previous year. The reduction was primarily due to the decrease in exchange gains.

The Bank’s Treasury recorded a notable performance with a significant increase of 89.4% in capital gains which was reported as Rs. 446 Mn. Income from investments in units remained flat at Rs. 227 Mn. Other operating income declined by 96.2% on the back of rupee depreciation and a significant increase in the number of funding swaps entered into, during the year under review.

The decline in trade volumes was attributable to adverse macro-economic conditions which also contributed to the overall decrease in trade income. The Bank has no trading equities and has not invested in any equity funds as at balance sheet date. The overall growth in core banking activities and the consistent financial performance which was mainly attributable to the increase of NII, led to a 13.9% growth in total operating income which was recorded as Rs. 6,021 Mn. Retail and SME segments increased their contribution to 51% of the total operating income during 2019.

Reflecting the macro-economic challenges, the Bank’s non-performing loans (NPL) ratio increased to 5.03% in 2019 in tandem with the increase of NPL ratios within the banking industry.

The SME banking segment showed the highest deterioration of NPL ratios during the year. Impairment charge for the year was Rs. 390 Mn - an increase of 14.0% YoY.

The operating expenses of the Bank was Rs. 3,830 Mn and was an increase of 2.7% YoY. Depreciation and amortisation and right-of-use asset coupled with other expenses increased by 2% YoY to Rs. 1,947 Mn. The Bank adopted SLFRS 16 “Leases” with effect from 1st January 2019. The comparative numbers have been calculated based on the previous Accounting standard LKAS 17. Accordingly, right-of-use asset have been recognised on the balance sheet and related amortisation have been considered under depreciation and amortisation instead of rent expenses charged under other expenses in 2018. Also, a portion has been recorded under interest expense as a finance cost of lease liability.

The Bank’s cost to income ratio improved to 64% from 71% in 2018 and marked a major milestone for the Bank in 2019.The operating margin increased to Rs. 2,191 Mn, and recorded a growth of 41% YoY. This represented widened jaws due to an increase of revenue at a faster pace of 13.9% as against the increase in costs by 2.7%; which asserts effective revenue and cost management, thus reflecting a significant improvement in the productivity and operational efficiencies of the Bank.

Share of profit of equity accounted investees for the year was Rs. 104 Mn and was a growth of Rs. 69.2 Mn YoY. The Bank’s subsidiary, UB Finance was the major contributor to this increase.

Profit for the year was Rs. 710 Mn compared to Rs. 473 Mn recorded in 2018 which was an impressive increase of 50.3% over the previous period. Other comprehensive Income for the year was Rs. 346 Mn which was a result of the impact on the valuation of investments in the government securities portfolio classified under financial investments at fair value through other comprehensive income. This was due to favourable market rate movements that prevailed during the year.

The Bank maintained a robust Capital Adequacy Ratio throughout the year reporting 16.75% core capital ratio as at year end.

The Group, consisting of the Bank and its two subsidiaries UB Finance Company Limited and National Asset Management Limited recorded Rs. 804 Mn in profit after all taxes which was a 50.4% growth YoY. Total assets of the group were reported as Rs. 129,840 Mn. The Bank accounts for 93.8% of the Balance Sheet of the Group and hence the Group performance is mainly propelled by the Bank.

Sustained business growth amidst challenges

The key business lines of the Bank continued to maintain growth in the year 2019 despite macro-economic challenges that continued to weigh down on the sector as a whole.

Corporate, SME and Retail Banking segments continued to propel the Bank’s portfolio expansion with selective acquisition strategies deployed on focused client segments that were identified as strategically significant. Despite challenges in the macro-economy, the Treasury performed well in 2019, contributing to the Bank’s revenue via significant capital gains and fee and commission income. Unfavourable market conditions had the greatest impact on the SME sector. Union Bank maintained its support to this sector with greater focus on their long-term funding requirements while managing the portfolio quality through sound risk management initiatives. In view of the challenges faced by Corporate and SME industries specially impacted by the Easter Sunday attacks, the Bank extended relief programmes and moratoriums towards the clients that were impacted to support and uphold their business operations during this difficult period. Corporate Banking recorded a very good performance through prudent management of portfolio yields, supported by new acquisitions and increased wallet share in identified segments. Union Bank BizDirect continued to be extended to the Bank’s Corporate and SME clients, facilitating best-in-class cash management convenience. In recognition of its great strides in providing Cash Management excellence, Union Bank was awarded ‘Best Cash Management Bank - Sri Lanka’ title at the Global Business Outlook Awards 2019.

Retail Banking continued to support the Bank’s credit growth through focused efforts on mortgaged backed loans and an aggressive drive on credit card acquisitions. Targeted initiatives conducted across the branches and within selected customer segments contributed to the Bank’s CASA and deposits growth objectives. Union Bank’s focus to increase customer convenience through technological enhancements was steadily furthered in 2019, with several initiatives implemented through alternate channels which includes the ATM network and digital banking platforms.

The Bank’s mobile banking application was further enhanced with added features and credit cards self-care services designed to provide an even better user experience. Union Bank unveiled a brand new corporate website in 2019 with a fresh outlook and improved features designed to support the Bank’s envisioned digital presence. The new and improved website of Union Bank won the Gold award under the Finance Category at dotCoMM Awards 2019 based in the USA.

Several customer engagement initiatives were carried out during the year to effectively manage key client relationships. Amongst them, the ‘CEO Breakfast Forum’ was a key highlight where key clients across Retail, SME and Corporate segments were provided an opportunity to gain insights on the economic landscape at the time along with a platform for networking and relationship building. The Bank conducted serveral other events for clients and the investor community during the year under review.

Re-affirming its commitment to support the well-being of society with a focus on children and education, several corporate social responsibility projects were initiated at selected branch localities with the objective to improve the standards of disadvantaged schools and provide better learning environments to children attending these schools.

Commenting on Union Bank 2019 performance Director/ CEO Indrajit Wickrmasinghe said, “I’m pleased to present Union Bank’s strong performance during a challenging year. Amidst many macro-economic challenges, the Bank had improved its core banking growth with focus on interest income, portfolio realignment and prudent cost management, reporting a resultant rise in profits. Union Bank marks its 25th anniversary in 2020 – a significant milestone that indicates our successful journey of growth over the years. During the year 2020 the Bank’s mid-term growth strategy will be furthered with a view to become a preferred banking partner to the target client segments served. We envision the business landscape to improve in the year 2020 and the Bank will continue to reinforce its Retail, Corporate, SME and Treasury businesses while capitalising on its clear competitive advantages to generate sustainable earnings. The focus on strategic growth segments, prudent portfolio expansion and inclusive banking approaches would pave the way for Union Bank’s progress in the year 2020.”