Wednesday Jul 15, 2026

Wednesday Jul 15, 2026

Wednesday, 13 June 2018 00:00 - - {{hitsCtrl.values.hits}}

By Piyush Pandey

The Hindu: We are seeing what is effectively India Inc.’s biggest ever fire sale. It’s even bigger than the Government’s planned divestment target.

The Reserve Bank of India’s (RBI) has decided to clean up the balance sheets of Indian banks, which are collectively saddled with Rs. 5 lakh crore of bad loans, by the end of this fiscal. So, the banks have started cracking the whip on Indian companies for repayment of loans. For most affected firms and groups, this will mean they will be forced to sell prized assets to repay their ballooning debts.

We are seeing ‘for sale’ tags on airports, roads, ports, steel plants, cement units, refineries, malls, corporate parks, land banks, coal mines, oil blocks, express highways, airwaves, Formula One teams, hotels, private jets, and even status symbol corporate HQs. Substantial stakes in firms, and in some cases entire companies, are on the block.

The Hindu reviewed leading corporate houses with billion-dollar loans riding on them, and the results are startling. The top 10 business house debtors alone owe Rs. 500,000 crore to the banks. They will be forced to sell assets worth over Rs. 200,000 crore.

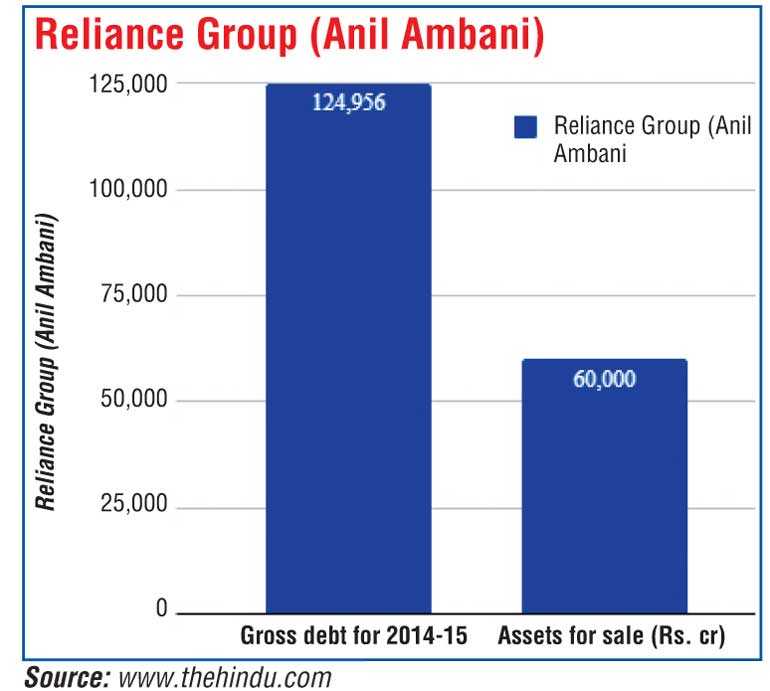

Reliance Group (Anil Ambani)

The Anil Ambani-led Reliance Group alone owes Rs. 121,000 crore of loans to the banks and had an annual interest liability of Rs. 8,299 crore against earnings before income tax of Rs. 9,848 crore. Some of the group’s firms, like Reliance Infrastructure and Reliance Defence, don’t earn enough to service the interest outgo.

The Anil Ambani-led Reliance Group alone owes Rs. 121,000 crore of loans to the banks and had an annual interest liability of Rs. 8,299 crore against earnings before income tax of Rs. 9,848 crore. Some of the group’s firms, like Reliance Infrastructure and Reliance Defence, don’t earn enough to service the interest outgo.

Assets put on sale by the Reliance Group include about 44,000 telecommunications towers (valued at Rs. 22,000 crore) and optic fibre and related infrastructure (Rs. 8,000 crore) from Reliance Communications (RCom), its flagship firm. Weighed down by about Rs. 40,000 crore of debt, RCom has posted a loss of Rs. 154 crore in FY14-15, and has continued to post losses in the first three quarters of FY 15-16, accumulating losses of over Rs. 2,000 crore until 31 December 2015; it is likely to end that fiscal with a net loss too. The company is valued at Rs. 13,440 crore, less than a third of its total debts. However, RCom plans to reduce its debts to Rs. 10,000 by selling Rs. 30,000 crore of telecom assets.

Reliance Infrastructure (R-Infra) is sitting on a pile of debt of Rs. 25,000 crore as of February. In November 2015, it agreed to sell a 49% stake in its electricity generation, transmission and distribution business in Mumbai and adjoining areas to Canadian pension fund Public Sector Pension Investment Board (PSP Investments). The transaction is expected to reduce debt of Rs. 7,000 crore attached to the distribution business. It agreed to sell its cement business to Birla Corporation for Rs. 4,800 crore in February, and is looking to sell its entire roads portfolio, valued at Rs. 9,000 crore, for which three international bidders have been short-listed. R-Infra’s EBIT stands at Rs. 1,686 crore, against interest liability of Rs. 1,974 crore. Its market capitalisation at Rs. 14,476 crore is Rs. 10,000 crore lower than its debt. By sale, of cement, road and the Mumbai power distribution businesses, the company expects to be debt free on standalone basis by the end of this fiscal.

Reliance Capital, with debt of Rs. 24,000 crore has sold stakes, in phases, in its mutual fund and life insurance businesses to Nippon Life Insurance for Rs. 3,461 crore to allow the latter to increase its stake to 49% in each of the businesses. It further plans to raise another Rs. 4,000 crore by the end of 2016-17 by selling non-core assets, including proprietary investment book and by inducting a partner in its general insurance business. Reliance Capital’s debt includes its lending portfolio – commercial lending and housing finance – of about Rs. 18,000 crore and claims to have a debt-equity ratio of 1.77, the lowest in the industry, as of 31 December 2015.

Ambani is also looking to exit the media and entertainment businesses, under Reliance Broadcast Network Ltd. (RBNL), for Rs. 1,500-Rs. 2,000 crore.

His foray into defence — the recently-acquired Pipavav Defence & Offshore Engineering, rechristened Reliance Defence — is sitting on debt of Rs. 6,800 crore against its current market capitalisation of Rs. 4,895 crore. The loss-making company with negative EBIT of Rs. 306 crore has an interest liability of Rs. 347 crore a year.

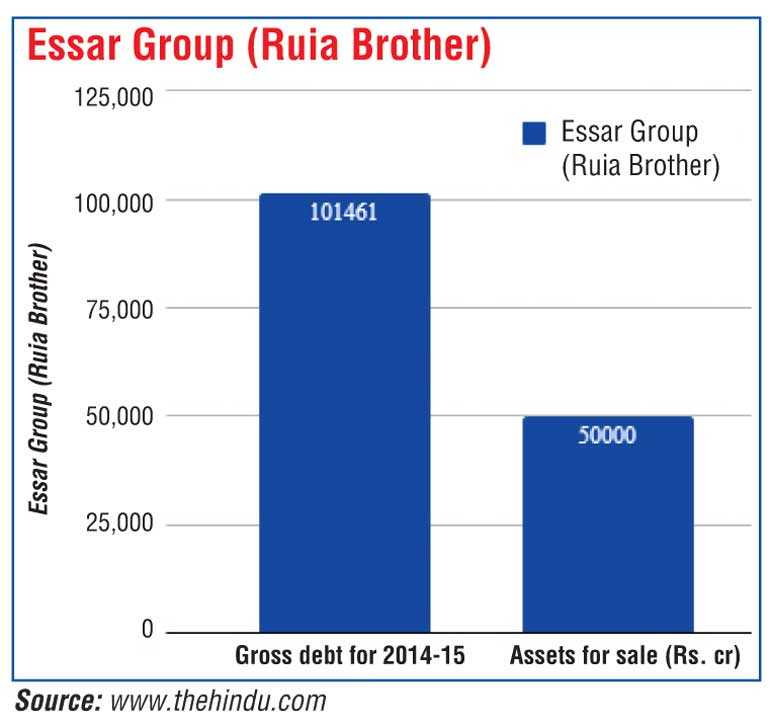

Ruia’s Essar group

(Shashi and Ravi Ruia)

Shashi and Ravi Ruia’s Essar group has gross debt of Rs. 101,461 crore. The group is looking to sell about 50% stake of its family silver, i.e., Essar Oil’s 20mtpa (million tonnes per annum) Vadinar refinery, for Rs. 25,000 crore. It also plans to bring in a financial partner for its 10mtpa steel business that currently has a debt of Rs. 40,000 crore; a 49% stake in the steel facility will be valued at about Rs. 25,000 crore. The debt-laden group is also looking to sell stake in its ports business. Essar Steel and Essar Oil each account for one-third of the group debt, and Essar Power, one-fifth.

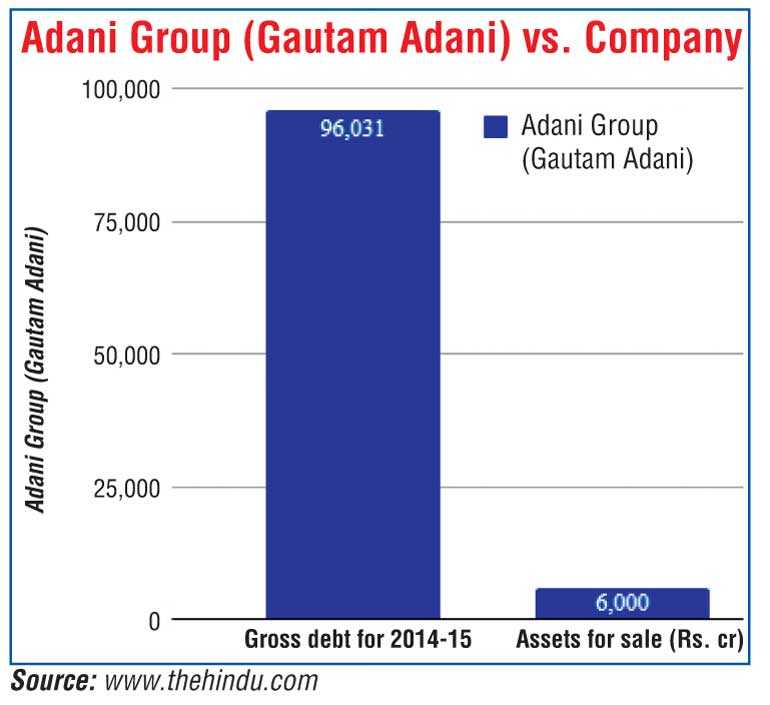

Adani group (Gautam Adani)

The billionaire Gautam Adani’s Adani group, with Rs. 96,031 crore debt, is under pressure to sell its stake in the Abbott Point coal mines, port and rail project. The Adani Group’s debt stands at Rs. 72,000 crore. Last year, Standard Chartered bank had recalled loans amounting to $2 .5 billion as part of its global policy of reducing exposure in emerging markets. Global lenders have backed out from funding the $10-billion coal mine development project. State Bank of India has also declined to offer a loan despite signing a MoU to fund the group with $1 billion. An Adani spokesperson declined to offer any comments on the issue.

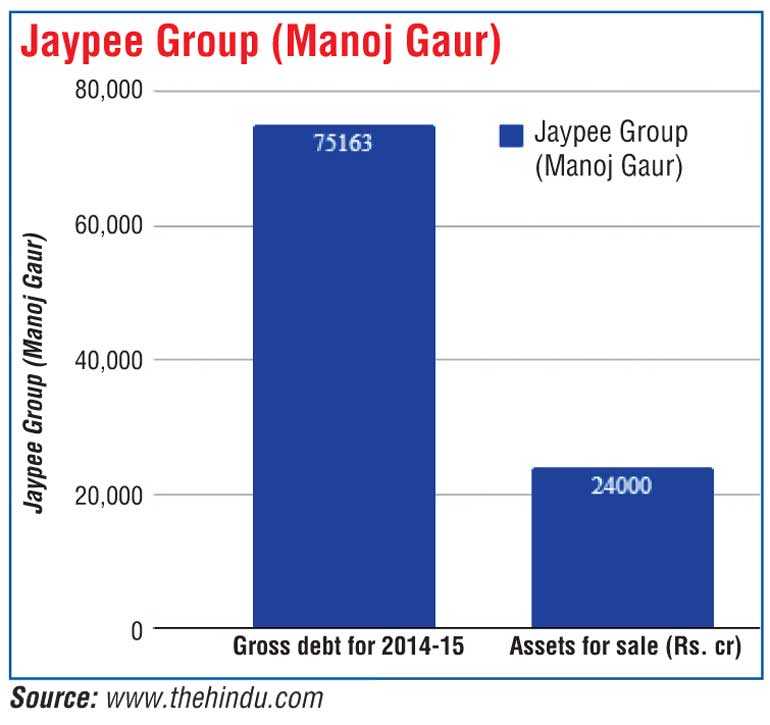

Jaypee group (Manoj Gaur)

Manoj Gaur’s Jaypee group’s debt is over Rs. 75,000 crore. The group has agreed to sell its 20mtpa of cement assets to Kumar Birla-led Ultratech for Rs. 15,900 crore. This will leave its listed entities with about 6mtpa of cement capacity, three thermal power plants, one hydropower plant, an expressway project and land parcels. It is looking to sell most of these assets at the right price, but buyers are not easy to come by.

Manoj Gaur’s Jaypee group’s debt is over Rs. 75,000 crore. The group has agreed to sell its 20mtpa of cement assets to Kumar Birla-led Ultratech for Rs. 15,900 crore. This will leave its listed entities with about 6mtpa of cement capacity, three thermal power plants, one hydropower plant, an expressway project and land parcels. It is looking to sell most of these assets at the right price, but buyers are not easy to come by.

Aside from selling stake in its land parcels and the Yamuna Express Highway, the group is looking to sell its remaining cement plants for Rs. 4,000 crore and its Bina thermal power plant for Rs. 3,500 crore. In the last year, the group has defaulted on payment obligations worth $350 million. Analysts say its capacity to service its debt has not improved.

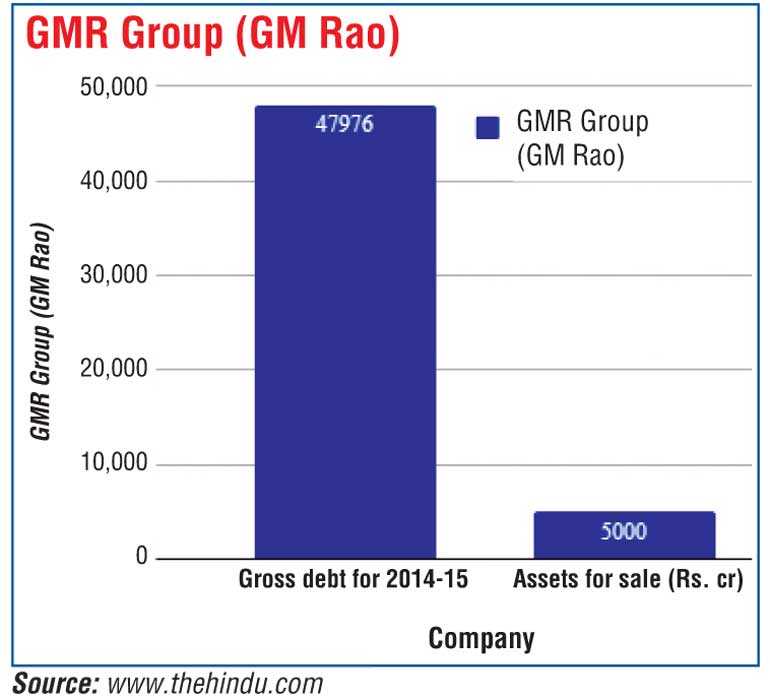

GMR group (GM Rao)

G.M. Rao’s GMR group was one of the first debt-ridden companies to sell off assets; it has already offloaded stake worth Rs. 11,000 crore in its roads, power and coal assets in the last two years. Despite this, its total debt has actually gone up: from Rs. 42,349 crore at the end of FY13 to Rs. 47,738 as of March 2015. The group is planning to raise about Rs. 5,000 crore this year by selling land parcels, energy assets and stake in airport subsidiary. Last month, it announced it was selling part of a road project in Karnataka, to help reduce debt by more than Rs. 1,000 crore. It also plans to sell 30% of its stake in its airport arm, which is valued about Rs. 10,000 crore.

Lanco group

(L Madhusudhan Rao)

The Lanco group has debts of Rs. 47,102 crore. It completed the sale of its Udupi plant in FY16 for Rs. 6,300 crore (15% of FY15 debt). Debt levels have continued to rise, up 6% in FY15. The group plans to sell power assets worth Rs. 25,000 crore to de-leverage its balance sheet and retire debts of about Rs. 18,000 crore. It is also planning to sell a one-third stake in the Australian coal mine it acquired in 2011 for $ 750 million.

Videocon group

(Venugopal Dhoot)

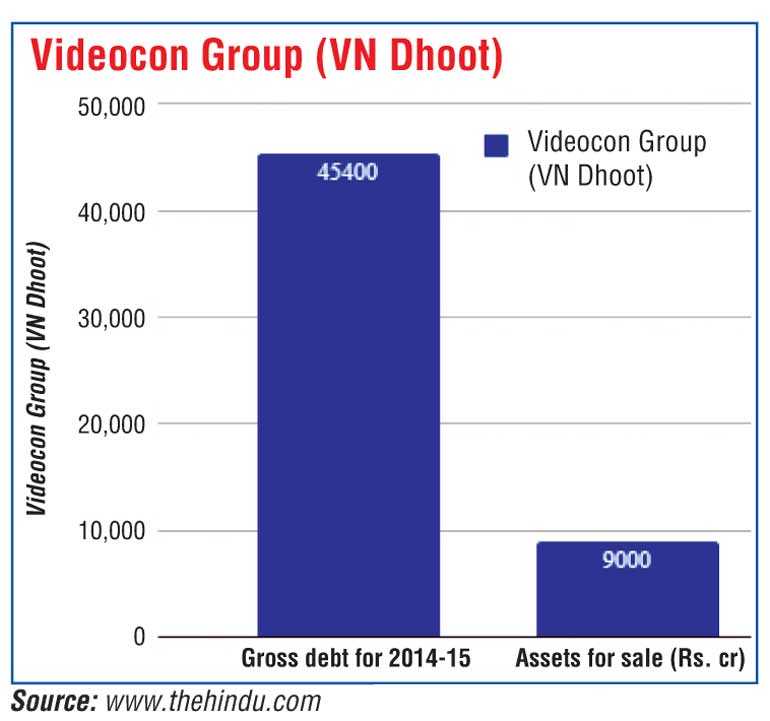

Despite the Videocon group selling its stake in its Mozambique gas fields for Rs. 15,000 crore, gross debt has continued to rise: it is up 10% year-on-year to Rs. 45,405 crore, while net debt has remained largely flat at Rs. 39,600 crore. Last month, it sold its spectrum to Bharti Airtel for Rs. 4,600 crore.

Despite the Videocon group selling its stake in its Mozambique gas fields for Rs. 15,000 crore, gross debt has continued to rise: it is up 10% year-on-year to Rs. 45,405 crore, while net debt has remained largely flat at Rs. 39,600 crore. Last month, it sold its spectrum to Bharti Airtel for Rs. 4,600 crore.

“If you minus last month’s spectrum sale amount of Rs. 4,600 crore which will be paid directly to the banks, then debt comes to Rs. 34,000 crore. To decrease debt further, we will be liquidating assets worth Rs. 5,000 crore this year so the net debt of the group will be around Rs. 29,000 crore,” Videocon Industries chairman Venugopal Dhoot told The Hindu adding that out of this net debt, Rs. 21,000 crore has been taken for oil and gas ventures in Brazil, Indonesia and across the globe, where the group and its partners have discovered oil and gas reserves. So, domestic debt of around Rs. 8,000 crore will be serviced.

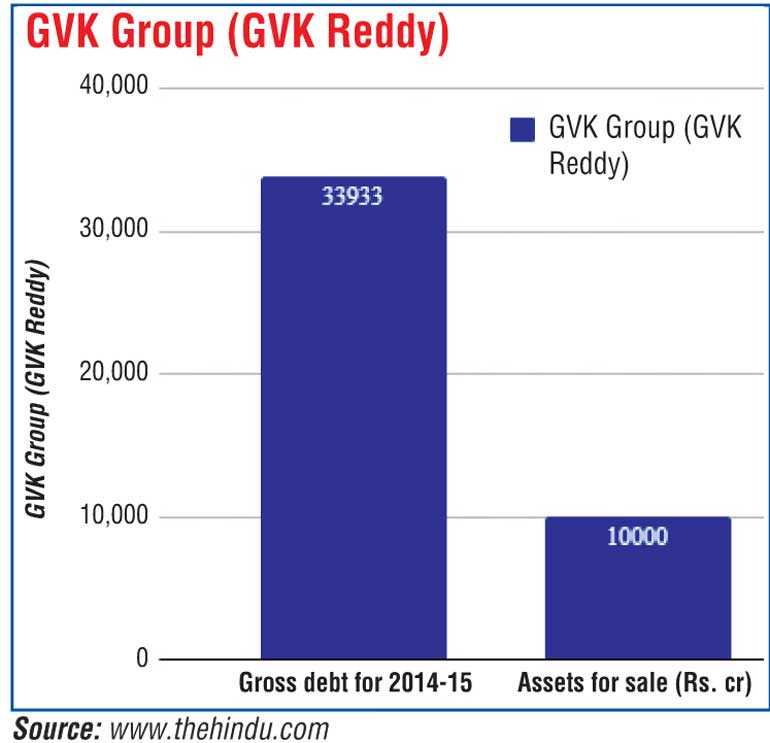

GVK group (G.V. Krishna Reddy)

To repay some of its debt of Rs. 34,000 crore, the GVK group is in talks to sell 49% of its airport subsidiary, which has an enterprise value of Rs. 10,000 crore. Last month, it agreed to divest its 33% stake in BIAL to Fairfax India Holdings Corp for an aggregate investment of Rs. 2,149 crore.

The company is also exploring the possibility of bringing in equity investors into Hancock Infrastructure Ltd., its holding company for its rail and port projects in Australia. A GVK spokesperson in reply to an e-mail query by The Hindu said, “As part of our corporate policy, we do not comment on any speculation in the media. While it’s public knowledge that we are considering various options for reducing our debt, we regret we cannot respond to any of your queries.”

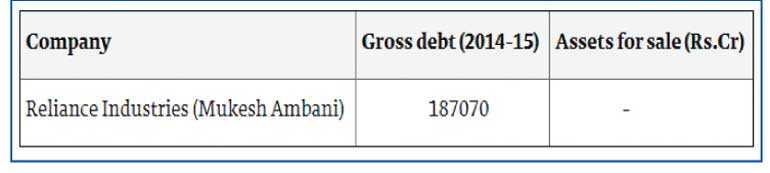

Reliance Industries

(Mukesh Ambani)

India’s largest debtor, Mukesh Ambani’s Reliance Industries (RIL), has a total debt of Rs. 187,079 crore (up from Rs. 62,500 crore as on 31 March 2010, mainly because of the Rs. 150,000 crore roll-out of Reliance Jio), the biggest among all corporate houses, and the largest ever in Indian corporate history. But it’s also one of the best-rated firms in servicing its interest, so banks are happy to offer RIL loans at competitive rates. Analysts believe that huge debt may weigh down the profitability due to interest outgo and depreciation after the commercial roll-out of Reliance Jio, if it is not able to scale up quickly.

India’s largest debtor, Mukesh Ambani’s Reliance Industries (RIL), has a total debt of Rs. 187,079 crore (up from Rs. 62,500 crore as on 31 March 2010, mainly because of the Rs. 150,000 crore roll-out of Reliance Jio), the biggest among all corporate houses, and the largest ever in Indian corporate history. But it’s also one of the best-rated firms in servicing its interest, so banks are happy to offer RIL loans at competitive rates. Analysts believe that huge debt may weigh down the profitability due to interest outgo and depreciation after the commercial roll-out of Reliance Jio, if it is not able to scale up quickly.

Tata Group

The Tata Group, India’s largest corporate group, with over 100 companies, wants to sell its UK steel business, which came as part of the $12.9 billion acquisition by Tata Steel of Corus in 2007.

Tata Steel had invested over $ 2 billion as capital expenditure in its UK steel business and it has now written down the value of its investment of $2.9 billion, meaning the value of its UK steel business is almost zero. The company’s consolidated debt was $10.7 billion on September 30, 2015, with the total long-term debt of its Europe business at about $4.3 billion.

The others Among

other corporates,

Naveen Jindal-led Jindal Steel and Power Ltd. has agreed to sell a 1,000 MW power plant to his elder brother Sajjan Jindal at an enterprise value of Rs. 6,500 crore and is looking to sell other assets to reduce debts of Rs. 46,000 crore.

DLF Ltd., India’s most valuable property developer, has sought expressions of interest from several top global investors to sell a 40% stake in its rental assets arm as it seeks to pare debt.

The rental assets arm holds about 20 million sq.ft of leased-out office space and is valued at about $2 billion.

India’s largest sugar producer Shree Renuka Sugars Ltd. has declared its Brazilian unit bankrupt and has filed for protection in the country. The company plans to fully exit from the National Commodity & Derivatives Exchange (NCDEX), as part of a strategy to sell all its non-core assets to reduce debt.

The Sahara group’s sale list is long: 86 real estate assets, a 42% stake in Formula 1 team Force India, four airplanes, and its hotels: the Sahara Hotel in Mumbai, Grosvenor House, London, the New York Plaza Hotel, and The Dream New York Hotel.

Almost all of Vijay Mallya’s assets are on sale by the banks.

Quenching the fire

Despite all the desperate deleveraging, the financial stress at these groups has intensified: all of them saw further increases in debt in FY15. These debts have grown seven-fold over the past eight years and account for 12% of system loans, according to Credit Suisse

As groups like Jaypee and GMR cut back on capex and sold assets, their debt and EBITDA have deteriorated further, mainly because they sold their best assets, which were contributing to as much as 70% of their EBITDA. For Jaypee, Lanco, Essar, and GMR, about half their debt has already been downgraded to Default by rating agencies.

For GMR and Videocon, absolute debt has continued to rise despite asset sales. Lanco’s Udipi plant sales reduced debt levels by 15%, but that project contributed to 69% of its FY15 EBITDA. Videocon too hasn’t seen any reduction in debt levels.

Investment advisor SP Tulsian said that when you have gangrene in your body, you need to chop off that part to survive; “Similarly, Indian firms need to sell off assets to deleverage their balance sheets or they will die sooner or later. For, banks will take control of their assets and sell them to recover dues.”

However, Morgan Stanley, the global financial services firm believes that the worst of India’s corporate debt crisis seems to be over as companies are reporting positive Free Cash Flow (FCF) for only the second time in two decades.

In its Asia Insight Report titled ‘India – Macro meets Micro,’ Morgan Stanley said that the distress in corporate India’s balance sheet is unchanged for the past four years and lists out the following problems of corporate sector:

It’s a balance sheet recession

Corporate debt to equity is at all-time high

The debt service ratio is at a new low. The BSE 500 index companies have about four times their operating income to pay interest expenses compared to around 10 times in the boom years

Interest to sales is approaching an all-time high, hurting net margins and impeding debt serviceability.

Excess return on capital (ROCE minus the prime lending rate) is at all-time lows and in negative territory. This means that companies are earning less on their investment than the cost of their debt.

Tulsi Tanti’s Suzlon became the first casualty of the banks’ recovery drive. In 2015, it was forced to sell its largest international subsidiary, Senvion, bought for €1.4 billion euro in 2007, for around €1.1 billion. The sale helped Suzlon cut down its debt of Rs. 16,500 crore to Rs. 10,500 crore, and reduce its interest liability from Rs. 1,600 crore to Rs. 800 crore a year.

More companies from indebted sectors — power, infra, steel, realty for example — will be forced to emulate Suzlon and go for rapid asset sale in the hope of staying afloat until better times.

(Source: http://www.thehindu.com/business/Industry/the-biggest-ever-fire-sale-of-indian-corporate-assets-has-begun-to-tide-over-bad-loans-crisis/article14310208.ece)